(Stata13): VAR and Impulse Response Functions (2)

Автор: CrunchEconometrix

Загружено: 2018-06-20

Просмотров: 46205

Описание:

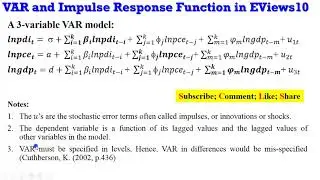

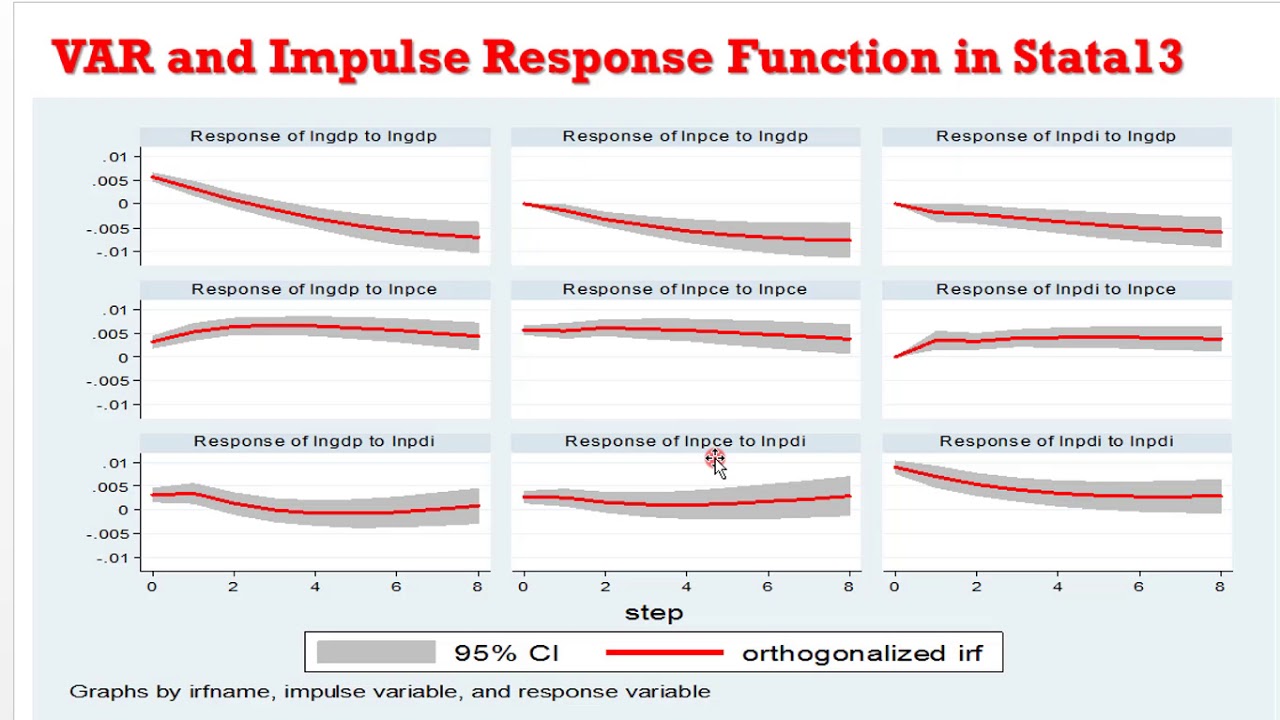

What do you understand by impulse response function? It explains the reaction of an endogenous variable to one of the innovations; describes the evolution of the variable of interest along a specified time horizon after a shock in a given moment; it is an essential tool in empirical causal analysis and policy effectiveness analysis; tracks the impact of a variable on other variables in the system; traces the effects on present and future values of the endogenous variable of one standard deviation shock to one of the innovations; in signal processing, the impulse response of a dynamic system is its output when presented with a brief input signal, called an impulse; used in explaining the concepts of “pass through” which measures degree at which the changes in a variable are passed to other variables at different stages either directly or indirectly; used to further assess the tendencies of significant Granger causality results. Also, because individual coefficients in the estimated VAR models are often difficult to interpret, hence practitioners often estimate the impulse response function (IRF). The IRF traces out the response of the dependent variable in the VAR system to shocks in the error terms, such as 〖 u〗_1, 〖 u〗_2 and 〖 u〗_3 used in this tutorial. Suppose 〖 u〗_1 in the lnpdi equation increases by a value of one standard deviation. Such a shock or change will change lnpdi in the current as well as future periods. But since lnpdi appears in the lnpce and lngdp regressions, the change in 〖 u〗_1 will also have an impact on lnpce and lngdp. Similarly, a change of one standard deviation in 〖 u〗_2 of the lnpce equation will have an impact on lnpdi and lngdp…and same for a change of one standard deviation in 〖 u〗_3 of the lngdp equation. The IRF traces out the impact of such shocks for several periods in the future. Although the utility of such IRF analysis has been questioned by researchers, it is the centre-piece of VAR analysis. Using Stata13, this video shows you how to perform impulse response function within a VAR framework and interpret the results.

Here is the link to the ex21-1.wf1 dataset (EViews file) used for this tutorial (endeavour to have a Google account for easy accessibility): https://drive.google.com/drive/u/1/fo...

Follow up with soft-notes and updates from CrunchEconometrix:

Website: http://cruncheconometrix.com.ng

Blog: https://cruncheconometrix.blogspot.co...

Forum: http://cruncheconometrix.com.ng/blog/...

Facebook: / cruncheconometrix

YouTube Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and Interpret Two-way A...

EViews Videos Playlist: • (EViews10):Interpret VECM, Forecast Error ...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: