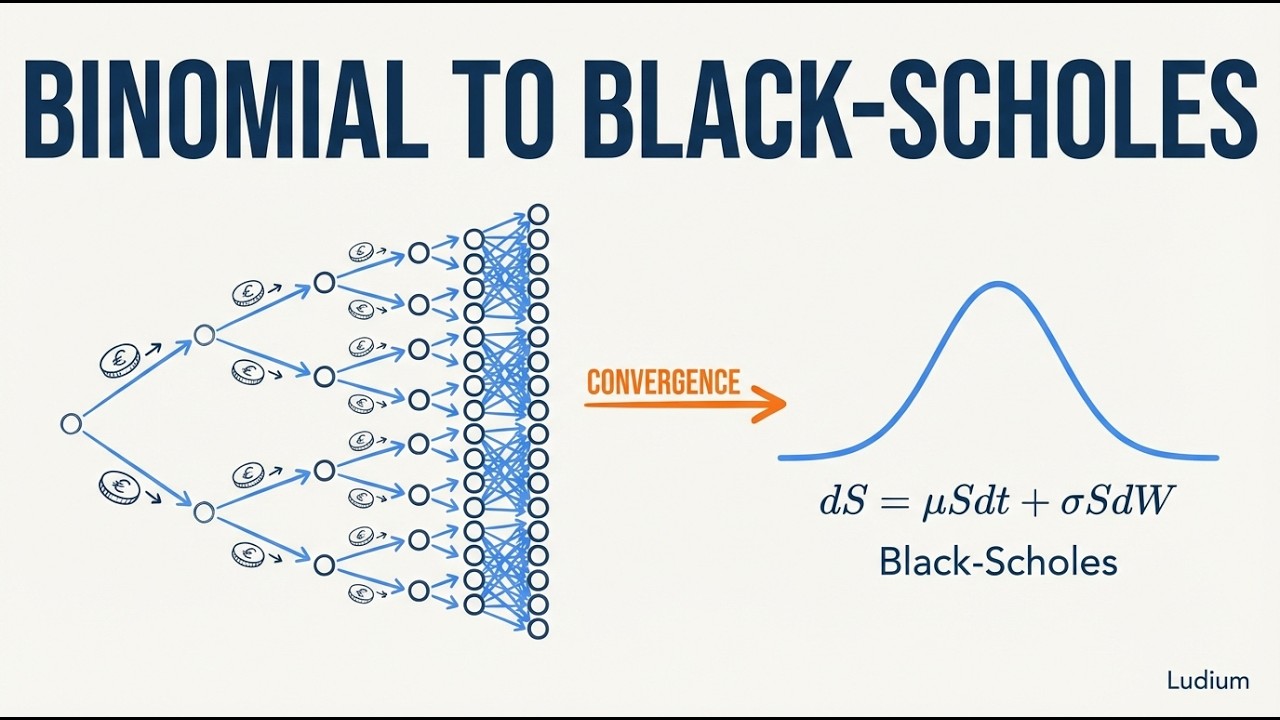

Finance Theory — 12.3: Binomial Trees to Black-Scholes

Автор: Ludium

Загружено: 2026-02-17

Просмотров: 134

Описание:

How does a simple coin flip — heads the stock goes up, tails it goes down — become the most famous formula in finance? This video traces the precise mathematical path from single-period binomial models through multi-period trees to the continuous-time Black-Scholes formula. Along the way, you'll see why the Central Limit Theorem turns discrete Bernoulli trials into the lognormal distribution, and why Wall Street practitioners still prefer trees over elegant closed-form solutions.

Key concepts covered:

• One-period binomial model as a Bernoulli trial with risk-neutral pricing

• Recombining trees and combinatorial explosion of terminal outcomes

• Period length flexibility — how shrinking step size shrinks disagreements about price dynamics

• Convergence of binomial terminal distributions to the lognormal via the Central Limit Theorem

• The Black-Scholes formula as the continuous limit of binomial option pricing

• Numerical example: pricing a call option (S₀=$100, K=$105, σ=20%, r=5%, T=1yr → C=$8.02)

• Why trees beat PDEs for American options, barrier options, and mortgage-backed securities

• Decision logic at tree nodes replacing differential equations for complex instruments

—

ORIGINAL SOURCE

This video distills concepts from the following lecture:

• Ses 12: Options III & Risk and Return I

All credit for the original educational content belongs to the original author(s).

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: