Finance Theory — 12.2: Risk-Neutral Option Pricing

Автор: Ludium

Загружено: 2026-02-17

Просмотров: 30

Описание:

Two traders disagree on whether a stock will go up or down — yet they arrive at the exact same option price. This video builds a one-period binomial model from scratch to show why real-world probabilities cancel out of option pricing entirely, and how replication and no-arbitrage arguments replace forecasting with financial engineering.

Key concepts covered:

• Binomial option pricing model with a concrete numerical example (S₀ = $20, strike = $15)

• Replicating portfolios: matching option payoffs with stock and bonds

• Why the real-world probability p never enters the pricing formula

• Risk-neutral probabilities (θ) as a mathematical pricing tool, not a market belief

• The equilibrium condition d ‹ r ‹ u and why both assets must coexist

• Arbitrage enforcement: how mispricing creates riskless profit opportunities

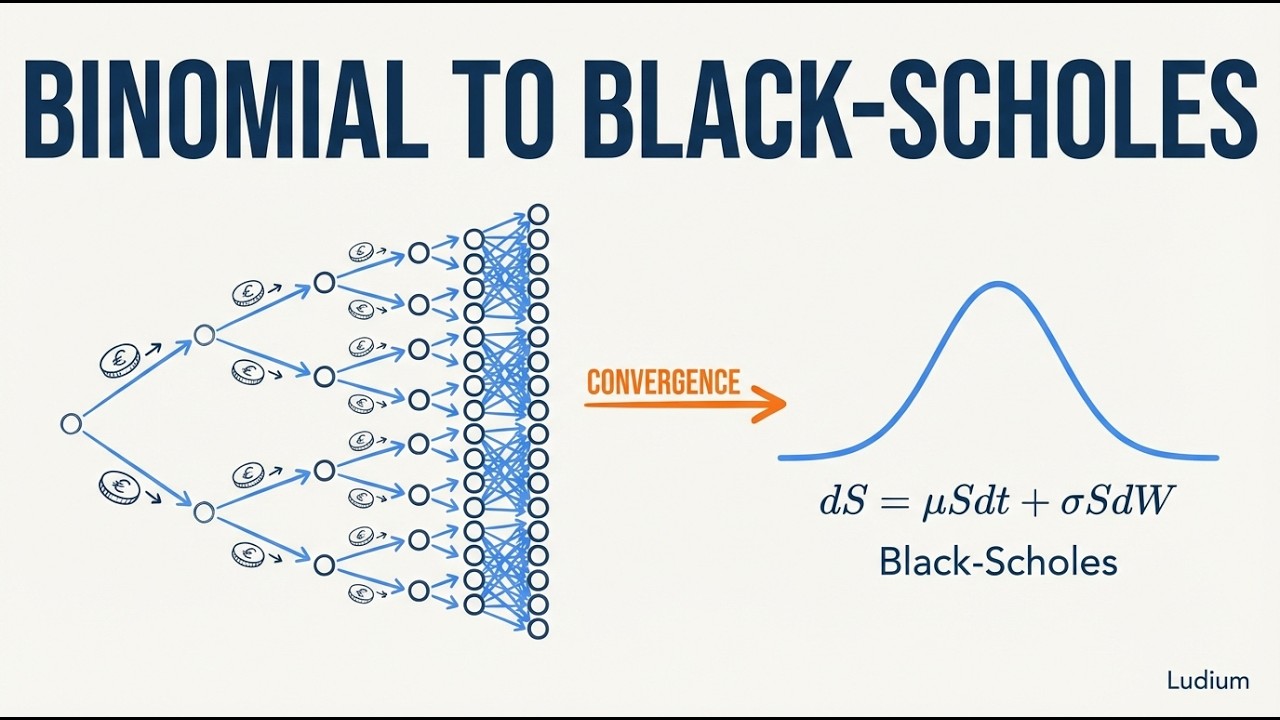

• The conceptual bridge from binomial trees to Black-Scholes

ORIGINAL SOURCE

This video is based on content from the following source:

• Ses 12: Options III & Risk and Return I

All credit for the original educational content belongs to the original creator.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: