Finance Theory — 16.3: Systematic vs. Idiosyncratic Risk

Автор: Ludium

Загружено: 2026-02-19

Просмотров: 4

Описание:

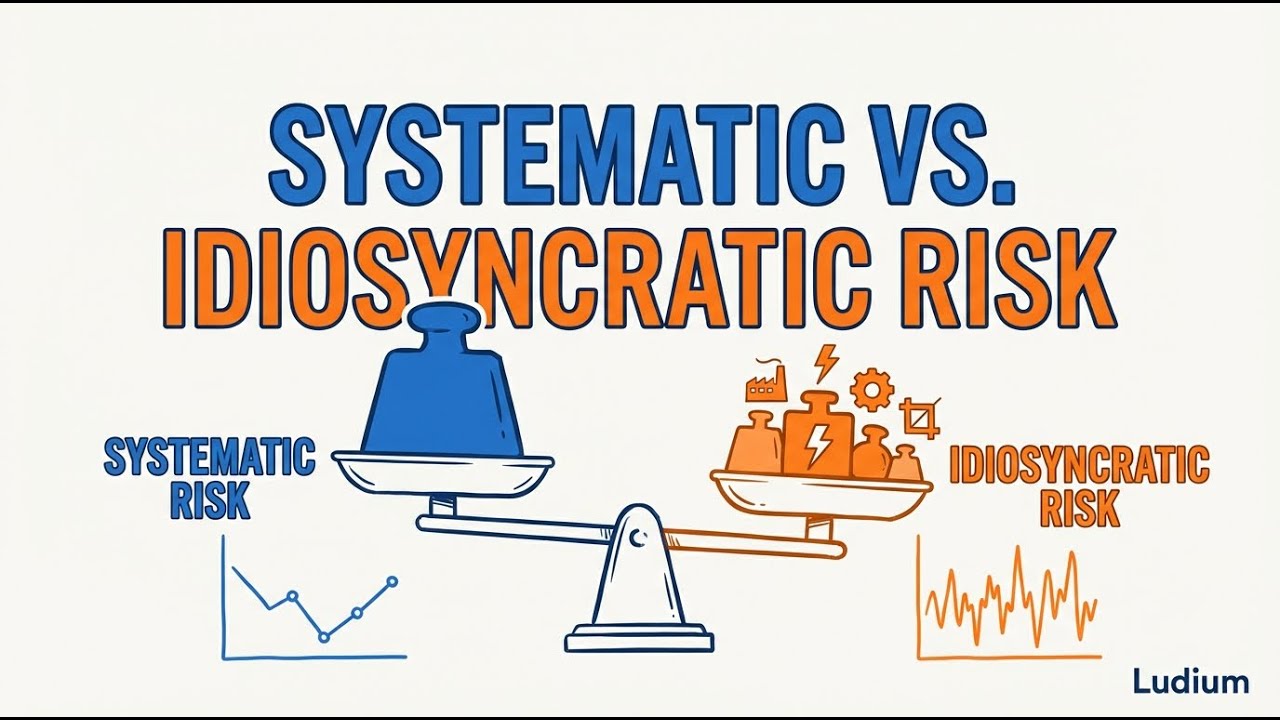

Why does the market reward some risks but not others? This video breaks down the two components of every stock's risk — systematic and idiosyncratic — and explains why diversification eliminates firm-specific risk for free, leaving only beta as the driver of expected returns. Using a memorable window washer analogy, real Apple vs. S&P 500 data, and the Capital Asset Pricing Model, you'll see exactly why concentrated portfolios are uncompensated gambles.

Key concepts covered:

• Systematic risk (market-wide: recessions, rate changes, geopolitical shocks) vs. idiosyncratic risk (firm-specific: CEO scandals, factory fires, failed drug trials)

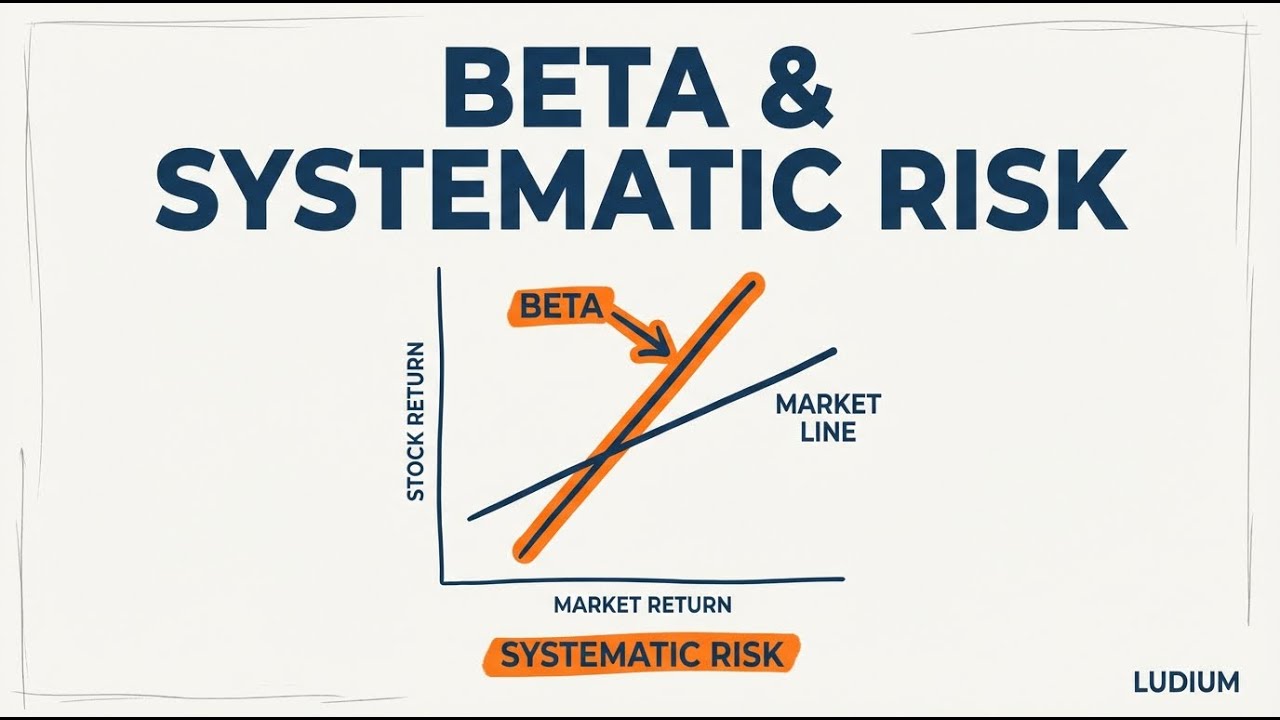

• Risk decomposition: Rᵢ = Rᶠ + βᵢ(Rₘ − Rᶠ) + εᵢ

• Beta as a measure of systematic exposure (β = 1 moves with market, β greater than 1 amplifies, β less than 1 dampens)

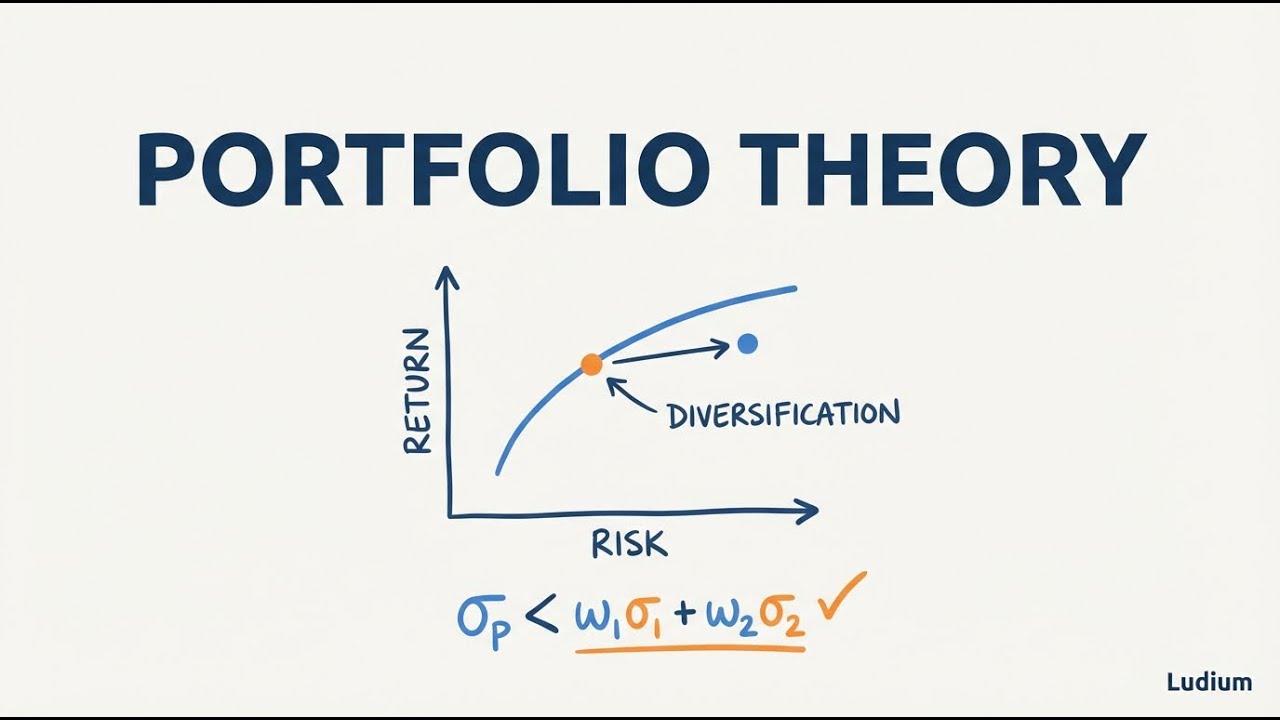

• The diversification curve: how portfolio volatility drops from ~45% (1 stock) to ~16% (50 stocks) as idiosyncratic risk vanishes

• Law of large numbers: why uncorrelated firm-specific risks cancel out as N increases — Var(εₚ) = (1/N) × σ̄²ε

• The CAPM equation: E(Rᵢ) = Rᶠ + βᵢ × [E(Rₘ) − Rᶠ] — no term for idiosyncratic risk

• Why equilibrium pricing means no rational investor pays a premium for diversifiable risk

• The employee stock concentration trap: salary, benefits, and portfolio all tied to one firm

• Human capital risk: why your portfolio should offset your career sector, not double down on it

• Common misconceptions — more risk does not always mean more return, and ~50 stocks across sectors is sufficient to diversify

• Four practical takeaways: hold 50+ stocks or an index fund, sell employer stock after holding periods, diversify away from your career sector, and always ask whether a risk is compensated

━━━━━━━━━━━━━━━━━━━━━━━━

SOURCE MATERIALS

The source materials for this video are from • Ses 16: The CAPM and APT II

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: