Portfolio Theory: How Diversification Reduces Risk Through Math

Автор: Ludium

Загружено: 2026-02-13

Просмотров: 14

Описание:

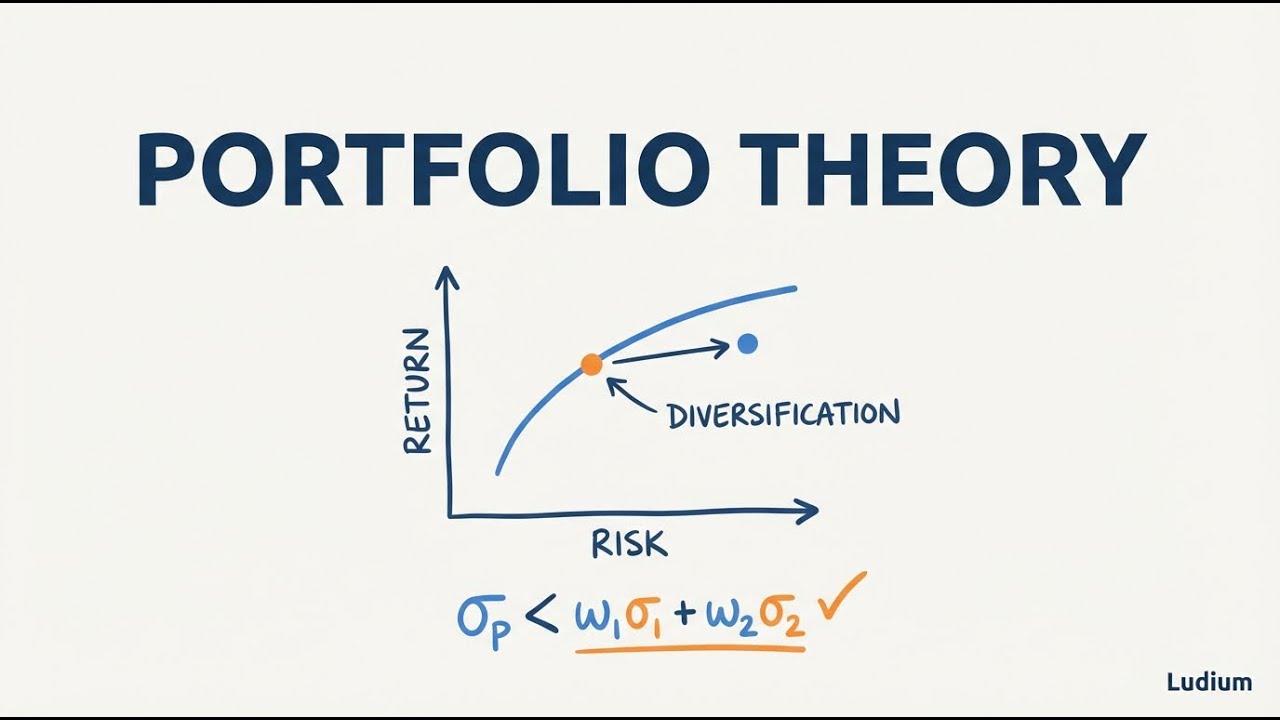

Why does combining assets into a portfolio produce better risk-adjusted returns than any single stock? This video walks through the mean-variance framework — the foundational tool of modern portfolio management — and shows exactly why diversification works, not as a vague principle, but as a mathematical certainty driven by correlation.

Using real historical data from assets like Motorola, Merck, McDonald's, GM, and the S&P 500, we build the risk-return map, define dominance versus tradeoff, and reveal how the efficient frontier curves northwest into territory no individual asset can reach alone.

Key concepts covered:

• The mean-variance framework: evaluating investments on expected return and standard deviation

• The risk-return scatter plot: mapping real assets on two dimensions

• Dominance vs. tradeoff: when one asset clearly beats another vs. when risk tolerance decides

• The efficient frontier: why portfolios curve northwest beyond individual assets

• Correlation as the engine of diversification — not the number of holdings

• Idiosyncratic risk vs. systematic risk in sector-focused portfolios

• Why portfolio contribution matters more than standalone merit

• Historical data limitations: process over prediction

---

ORIGINAL SOURCE

This video distills concepts from a longer lecture.

Source video: • Ses 13: Risk and Return II & Portfolio The...

Full credit to the original author and lecture series.

---

About Ludium

Learn. Play. Discover.

Ludium distills long lectures into focused concept videos, making complex ideas accessible without sacrificing rigor.

GitHub: https://github.com/Augustinus12835/au...

#PortfolioTheory #MeanVariance #Diversification #EfficientFrontier #RiskReturn #ModernPortfolioTheory #InvestingEducation #FinancialLiteracy

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: