The Earning Gap | Asset Liability Management

Автор: Edspira

Загружено: 2021-07-27

Просмотров: 16526

Описание:

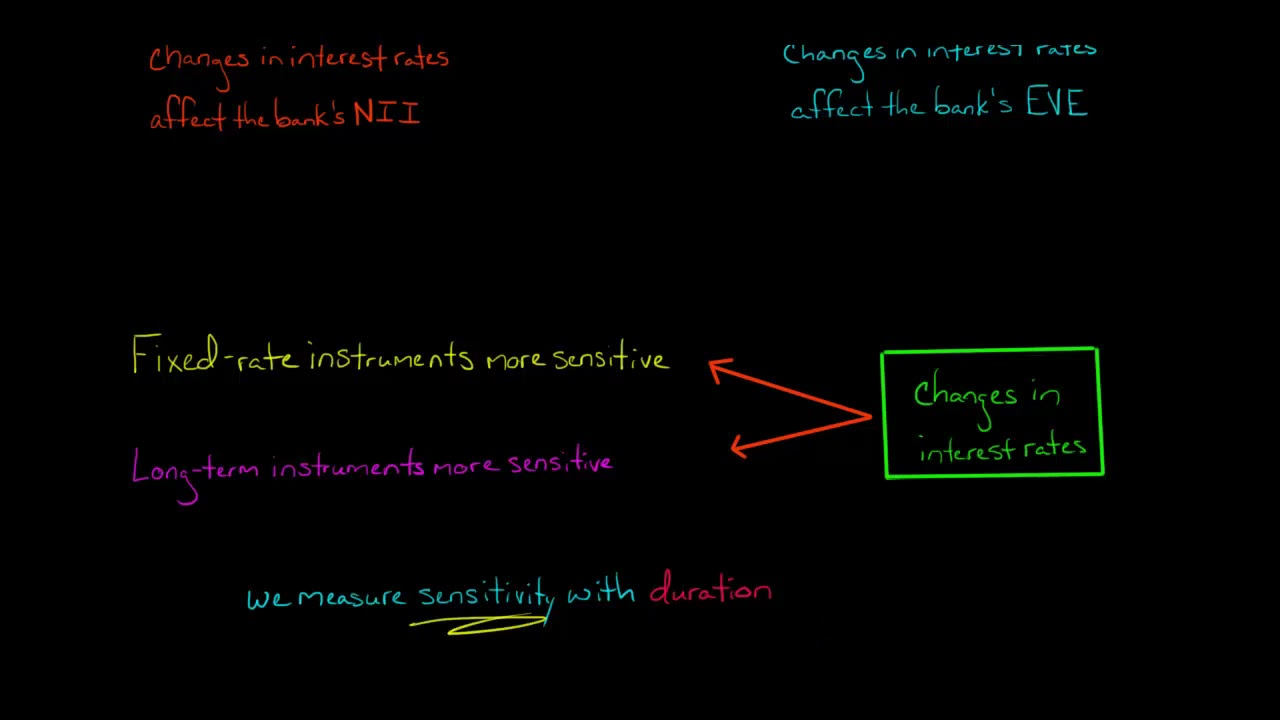

Mismatches between a bank’s source of funds (liabilities) and use of funds (assets) can affect the bank’s profit. This is best explained with an example.

Imagine a bank with one asset and one liability:

• The asset is a fixed-rate loan with an interest rate of 5%

• The liability is a floating-rate note with an interest rate of 2%

Thus, the bank has a net interest margin of 3%.

But what if the interest rate on the floating-rate note increases to 2.2%? The bank’s net interest margin will shrink to 2.8%. This occurred because we had a mismatch: a fixed-rate asset and a floating-rate liability.

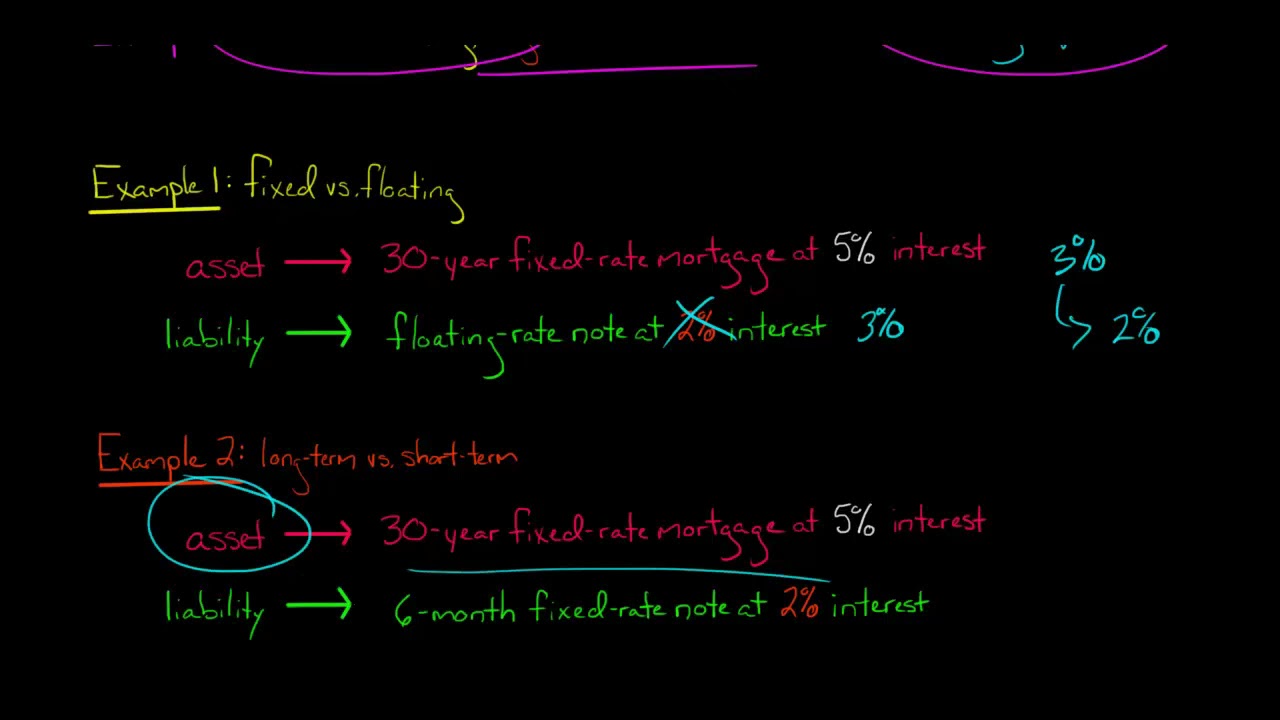

Here’s an example of a different kind of mismatch.

Imagine a bank with one asset and one liability:

• The asset is a fixed-rate loan with an interest rate of 5%

• The liability is a fixed-rate note with an interest rate of 2%

The bank again has a net interest margin of 3%.

But what if the fixed-rate loan has a term of 30 years, while the fixed-rate note has a term of 6 months? If interest rates rise, the bank’s net interest margin will decrease when it repays the note at the end of 6 months and obtains new financing at the higher rate. If the bank obtained new financing at a rate of 2.4%, then it’s net interest margin would be 2.6%. Again, the bank suffered from a mismatch problem. This time, the mismatch occurred because the bank funded a long-term asset with a short-term liability.

It’s difficult to solve the mismatch problem.

A local bank that focuses on conventional mortgages might have assets that are primarily fixed-rate mortgages and liabilities that are primarily floating-rate savings accounts. A bank could reduce this risk by entering into an interest rate swap.

Alternatively, a bank might have fixed-rate assets that reset monthly and floating-rate liabilities that reset quarterly. If interest rates are declining, the interest rate earned on assets will reset faster and reduce the net interest margin.

To estimate the effect of interest rate changes, banks compare the principals of assets and liabilities that are repriced during a period.

Banks then try to reduce this earning gap, which is the difference between rate-sensitive and rate-sensitive liabilities.

—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

http://eepurl.com/dIaa5z

—

SUPPORT EDSPIRA ON PATREON

* / prof_mclaughlin

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

https://edspira.thinkific.com

—

LISTEN TO THE SCHEME PODCAST

Apple Podcasts: https://podcasts.apple.com/us/podcast...

Spotify: https://open.spotify.com/show/4WaNTqV...

Website: https://www.edspira.com/podcast-2/

—

GET TAX TIPS ON TIKTOK

/ prof_mclaughlin

—

ACCESS INDEX OF VIDEOS

https://www.edspira.com/index

—

CONNECT WITH EDSPIRA

Facebook: / edspira

Instagram: / edspiradotcom

LinkedIn: / edspira

—

CONNECT WITH MICHAEL

Twitter: / prof_mclaughlin

LinkedIn: / prof-michael-mclaughlin

—

ABOUT EDSPIRA AND ITS CREATOR

https://www.edspira.com/about/

https://michaelmclaughlin.com

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: