Скачать

Quantlab - Turn of Year effect in Currency Interest Rate Swap Pricing

Автор: Quantlab

Загружено: 2018-03-22

Просмотров: 241

Описание:

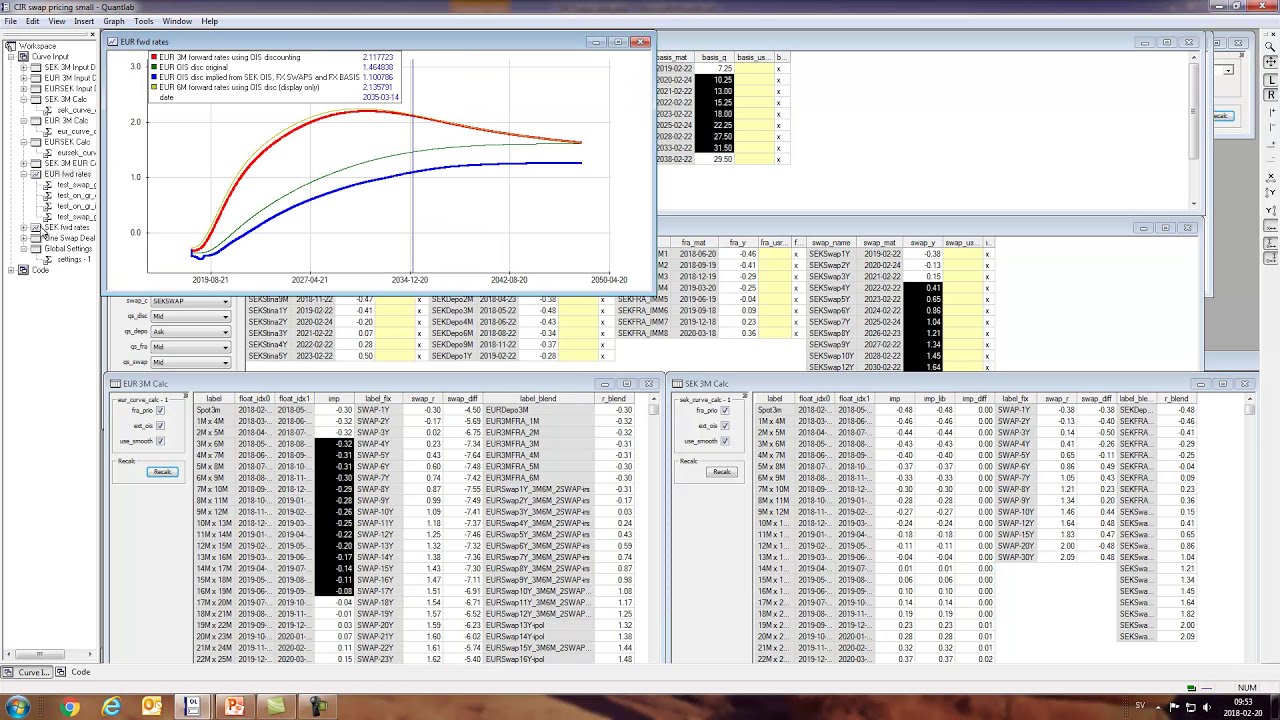

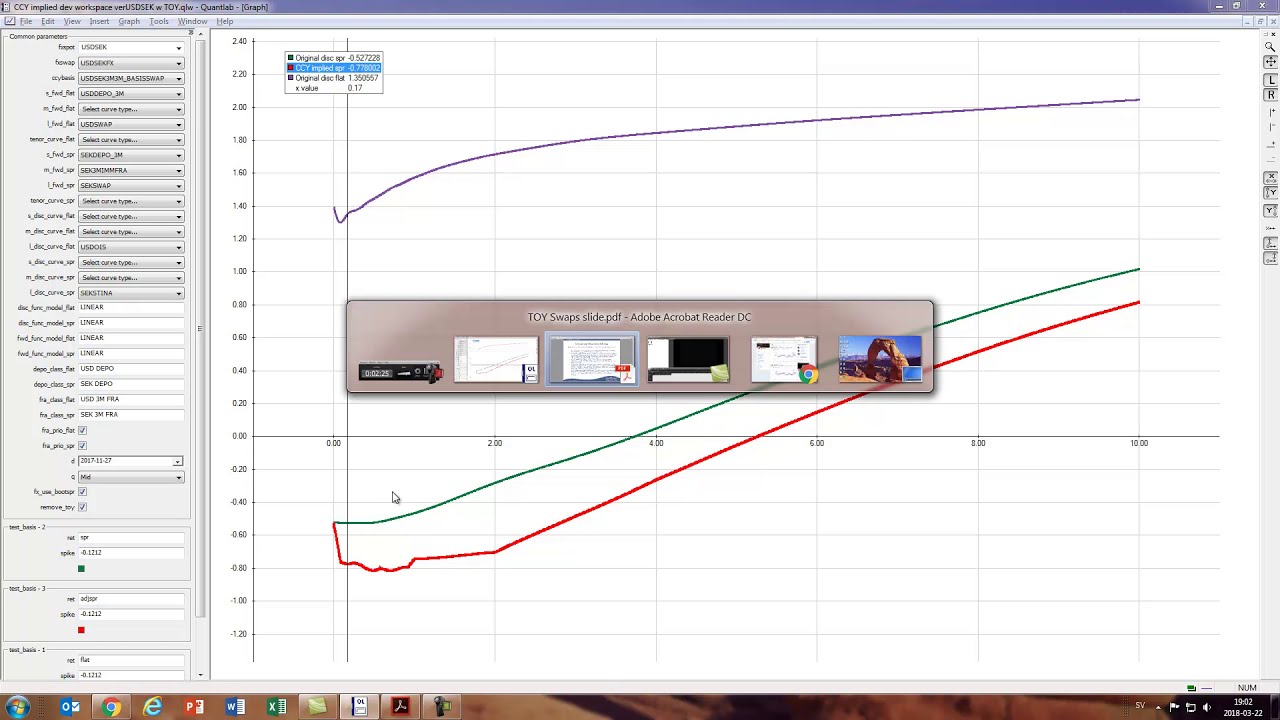

A continuation on things to take notice of when creating discount curves for pricing and risk measurement of currency related products such as the currency interest rate swap and fx swaps.

Here we focus our attention on the so called Turn-of-Year liquidity effect and how it effects the curve. We show how it is removed and discuss some implication of such a cleaning.

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: