Скачать

Quantlab - Valuation of Cross Currency Interest Rate Swap

Автор: Quantlab

Загружено: 2018-02-20

Просмотров: 9167

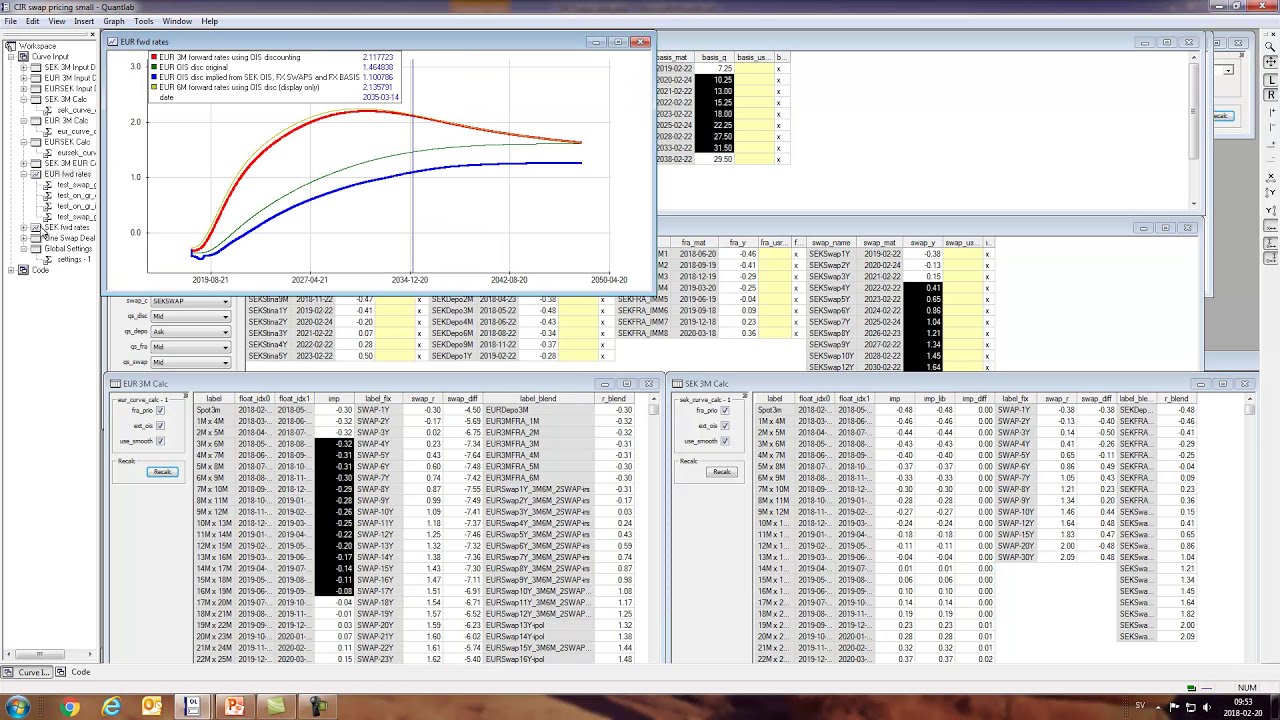

Описание: A short tutorial on valuation of the cross currency interest rate swap. Here exemplified using a EUR/SEK fixed/float 10Y swap. We extract 3M forward curves using dual bootstrap and OIS discounting, as well as extract the implied EUR discounting curve from the FX-swaps and FX-basis swap rates.

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: