Stress-Testing JEPI & JEPQ for Retirement

Автор: The Average Joe Investor

Загружено: 2026-02-20

Просмотров: 1913

Описание:

Which High-Yield Income ETF's do not have significant NAV Erosion AND deliver consistent income? Testing JEPI and JEPQ in this video.

-------------------------------------------------------------------------

This communication/content is for informational purposes only and is not intended as personalized investment advice, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon for purposes of transacting in securities or other investment vehicles. Trading options carries a high degree of risk and may not be appropriate for all investors. Options can lose value rapidly and a position may expire worthless. Some strategies can result in losses greater than your original investment. Past performance is not indicative of future results. This video is for educational purposes only and should not be construed as financial, investment, tax, or legal advice. Consult your personal financial advisor or other qualified professional before making any investment decisions. Do not trade with capital you cannot afford to lose.

------------------------------------------------------------------------

➡️Join Income Academy Today! ⬅️

https://www.skool.com/incomeacademy

------------------------------------------------------------------------

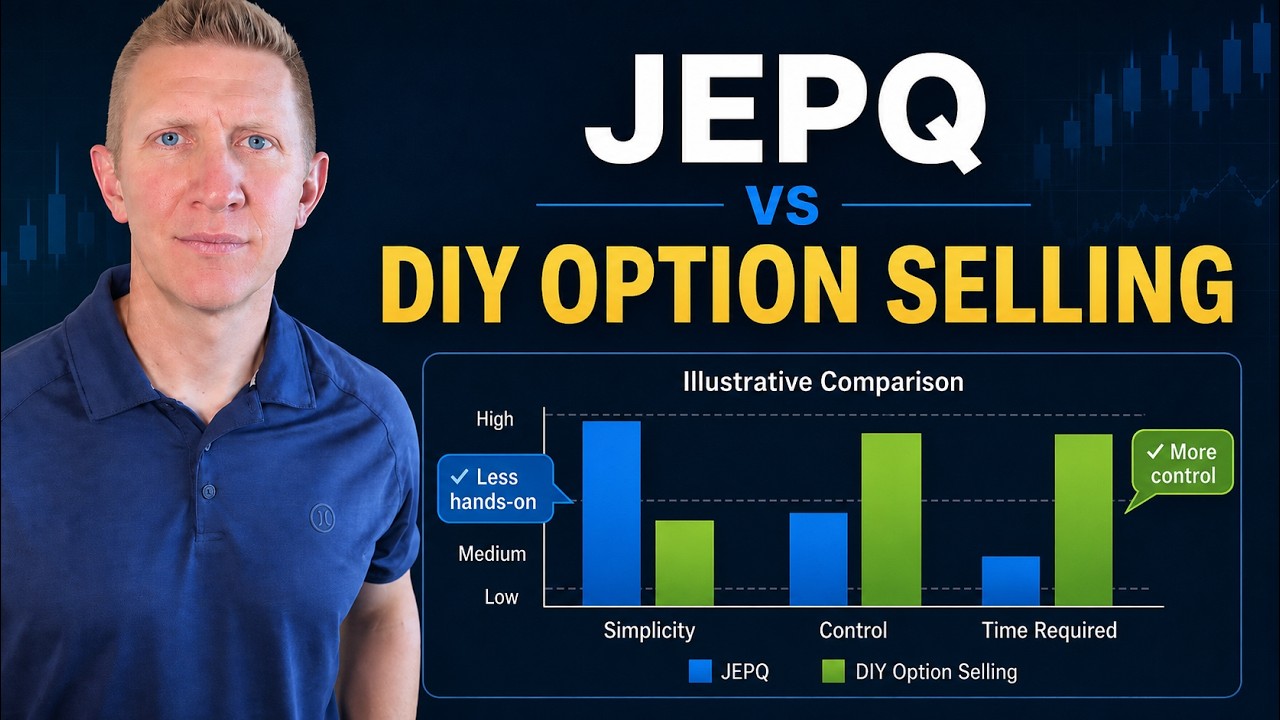

NAV erosion in high-yield option-income ETFs is the gradual loss of share price over time as the fund distributes a large portion of option premium and sometimes capital, while structurally capping its ability to fully recover in strong up markets.

What NAV erosion is (in this context)

In covered-call and 0DTE/derivatives-based income ETFs, NAV erosion typically comes from:

Systematically selling upside: Writing calls on most or all of the notional means the fund participates fully in drawdowns but only partially in sharp recoveries, so long-term price compounding lags the underlying index.

Paying out “too much” cash: If distributions materially exceed the underlying’s organic total return (price appreciation + dividends), the fund must effectively return capital, gradually walking NAV down.

Whipsaw/volatility effects: Fast down-then-up markets (e.g., crash and V-shaped recovery) are especially damaging because the strategy sells calls into volatility, captures downside, then repeatedly caps the upside needed to get back to prior highs.

Total return (NAV change + distributions reinvested) can still be competitive even if the price chart alone looks like a slow bleed; the “erosion” discussion is mostly about price level stability vs income level.

QYLD: textbook NAV erosion risk

QYLD (Global X Nasdaq 100 Covered Call ETF) sells at-the-money calls on 100% of the Nasdaq-100 exposure and distributes most of the premium as monthly income.

Structure: Fully covered, index-level, typically ATM calls on the Nasdaq-100, so upside is heavily capped every month.

Outcome: It tends to track drawdowns closely but underparticipate in subsequent rallies, which has led to long-run NAV decline even while paying double‑digit yields.

Evidence: One analysis estimates QYLD’s NAV declined at about −3–4% annually over a multi‑year period, despite attractive headline yield, because the strategy misses many of the strong up days that drive long-term equity returns.

In other words, QYLD is a classic example where investors see a stable or declining price plus large distributions: strong cash flow, but meaningful NAV erosion risk and lower long-run total return relative to simply holding QQQ.

QQQI: high income with limited NAV decay (so far)

QQQI (NEOS Nasdaq-100 High Income ETF) is also an income-focused options fund on the Nasdaq-100, but it is designed more around tax-efficient, actively managed call exposure rather than a simple “always 100% ATM covered call” rule.

Active overlay: NEOS adjusts call strikes and notional rather than mechanically overwriting 100% ATM, aiming to keep more upside for NAV while still generating high income.

1256 contracts & tax management: QQQI uses index options taxed under section 1256 (60/40 treatment) and incorporates tax-loss harvesting on options and equity holdings, targeting more tax-efficient income for taxable investors.

Distribution target: The fund explicitly targets a high annualized distribution rate (recent marketing has referenced a high‑teens to low‑20% range, after fees) from a mix of option premium and equity income.

QDTE: extreme yield, higher NAV-erosion risk

QDTE (Roundhill Innovation‑100 0DTE Covered Call Strategy ETF) runs a very different play: a synthetic covered call/overlay on an “Innovation‑100” tech/growth basket using 0‑days‑to‑expiry (0DTE) options, targeting enormous headline yield.

Structure: Uses short‑term (0DTE) index options to generate frequent premium while holding exposure to an innovation-focused equity index.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![ARMIA PUTINA DRUGĄ ARMIĄ ŚWIATA? PRAWDZIWA SIŁA ROSJI [WOLSKI I BOJKE]](https://imager.clipsaver.ru/-0hLR4R3gvk/max.jpg)