TILA RESPA Integrated Disclosure Rule (TRID) (Free Tutorial)

Автор: National Mortgage Exam

Загружено: 2022-04-20

Просмотров: 3401

Описание:

Welcome to the fourth episode of the National Mortgage Exam Tutorials & Practice Tests videos. The series will be following the sequence of topics as presented in the NMLS test content outline at https://bit.ly/NMLSoutline. Near the end of each video there is a link for downloading practice questions.

You can purchase The SAFE Mortgage Loan Originator National Exam Study Guide at https://amazon.com/author/patriciaoco.... There are hundreds of questions and two practice exams.

Please take a moment to subscribe at https://bit.ly/mortgage-exam. First, go to Settings/Privacy in your profile and make subscriptions public. You have to do this before you subscribe if you want quizzes starting at video #8,

****************************************************************************

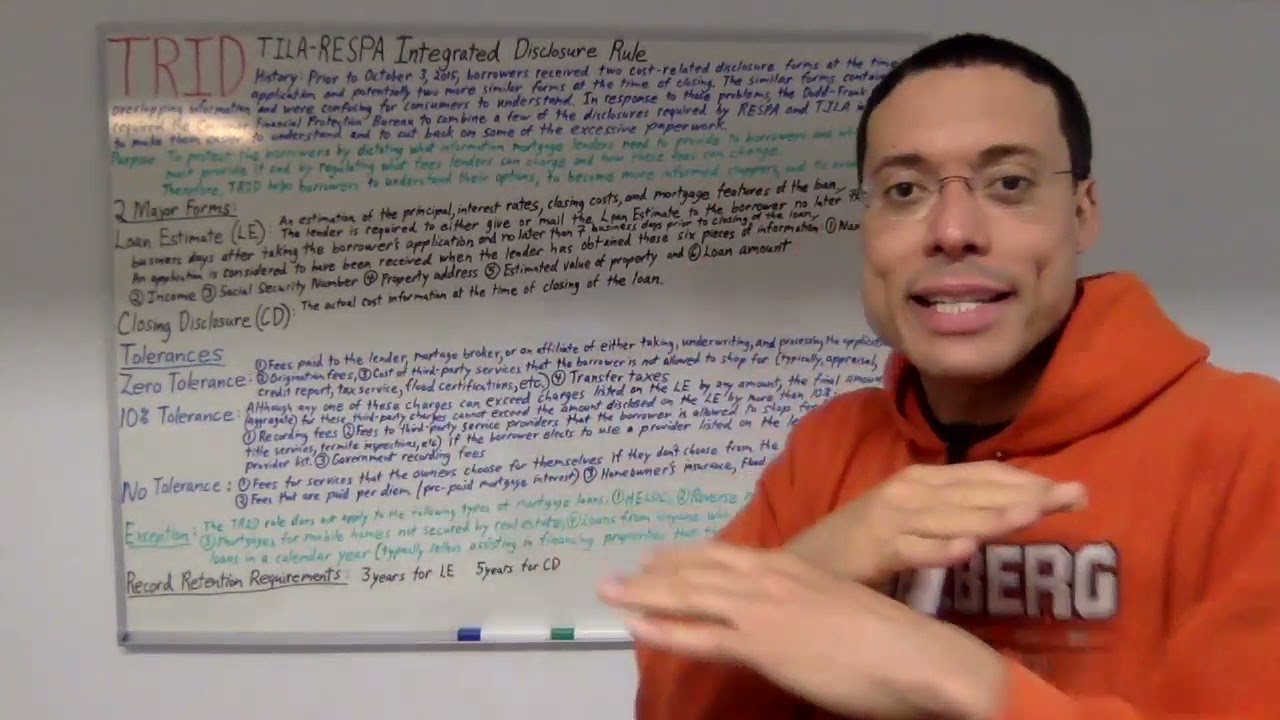

The TILA RESPA Integrated Disclosure (TRID) went into effect in 2015. Prior to 2015, all residential loans required a signed TILA APR disclosures and a Good Faith Estimate (GFE) at or shortly after an application, and a HUD-1Settlement statement with another TILA disclosure. The new corresponding disclosures are called the Loan Estimate and Closing Disclosure and the TILA APR disclosure is incorporated into each document. TRID applies to most closed-end residential loans (1-4 units) including purchase, refinancing, construction-only loans, and vacant land or 25 or more acres of land. It does NOT apply to reverse mortgages and Home Equity Lines of Credit (HELOC).

Loan Estimate Triggers

• Name

• Income

• SSN

• Property Address

• Estimate of Value

• Requested loan amount

Loan Estimate (LE) Facts

• Expiration date for interest rate lock

• Credit report fee is the only money that can be collected before the loan estimate is delivered and borrower requests to proceed.

• Borrower can’t be required to submit any documents before LE is received.

• LE must be mailed or delivered within 3 business days after loan application.

• LE must be delivered or mailed no later than 7 days before loan consumption (the day the state recognizes as the date when the borrower is legally contracted to the creditor. Possibilities include the day the contracts were signed or the day of funding.)

Loan Estimate (LE) Revisions

Creditors may not revise an estimate because of technical issues, incorrect calculations or low estimates. They can revise if changing circumstances:

• Increase the closing costs

• Affect the value of a property

• Negatively affects a borrower’s ability to qualify for the loan

• Consumer waits more than 10 business days to indicate an Intent to Proceed.

• Settlement is delayed more than 60 calendar days for a new construction loan if the original LE includes the statement that the estimate can be revised for this reason.

Lenders must operate within the following timeframes when reissuing an estimate:

• Delivered or mailed within 3 business days after becoming aware of the new information that required the reissuance.

• Delivery/mailing must precede the date the Closing Disclosure was delivered/mailed.

• Revised estimate is received at least 4 business days prior to loan consummation (mailed at least 7 business days prior). If the closing is scheduled before then, the changes may be reflected in the closing statement without reissuing the estimate.

Special Information Booklet

• Explains Settlement Costs

• Must be mailed or delivered within 3 business days after application

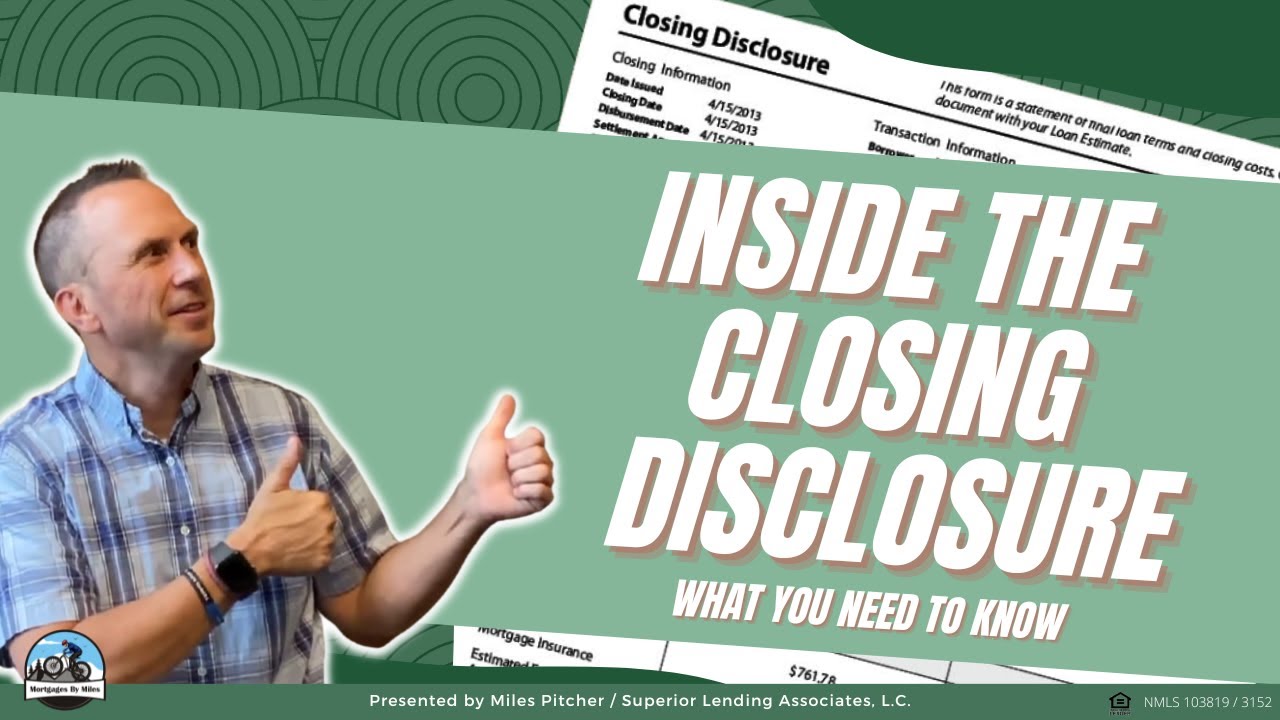

Closing Disclosure (CD)

• Borrower must receive the Closing Disclosure at least 3 business days before consummation. If the following items change, a new Closing Disclosure must be provided to the borrower and settlement is delayed for an additional 3 business days:

• APR.

• Loan product.

• Addition of a prepayment penalty.

• If there are changes other than these three items, borrower has the right to view the revised CD 1 business day before consummation.

• Seller hardship may be an exception to the 3-day rule

• Seller has the right to view the CD 1 day before consumption

Acceptable Percent of Variance between the Loan Estimate and Closing Disclosure numbers are:

• 0% for items outside of borrower’s control: real estate taxes, lender fees (loan origination and interest rate), credit report, and appraisal

• 10% for items lender chooses or recommends: government recording fees and title insurance (if recommended)

• Unlimited % for items that borrower chooses or that are paid per-diem (depends on closing date): Hazard insurance, title insurance (if not recommended by lender), and pre-paid mortgage interest (per-diem calculation). Lenders have 60 days to refund any excessive variance between the two documents.

Right of Recession

• A 3-day cooling-off period for refinances, home improvement or second mortgage loan on a primary residence.

• Loan not funded until period is over.

• Borrowers receive a Notice of Right to Rescind when applying.

• They can cancel in writing up until midnight of the third business day (including Saturday) after signing the contract.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: