Finance Theory — 11.3: Implied Volatility and the VIX

Автор: Ludium

Загружено: 2026-02-17

Просмотров: 55

Описание:

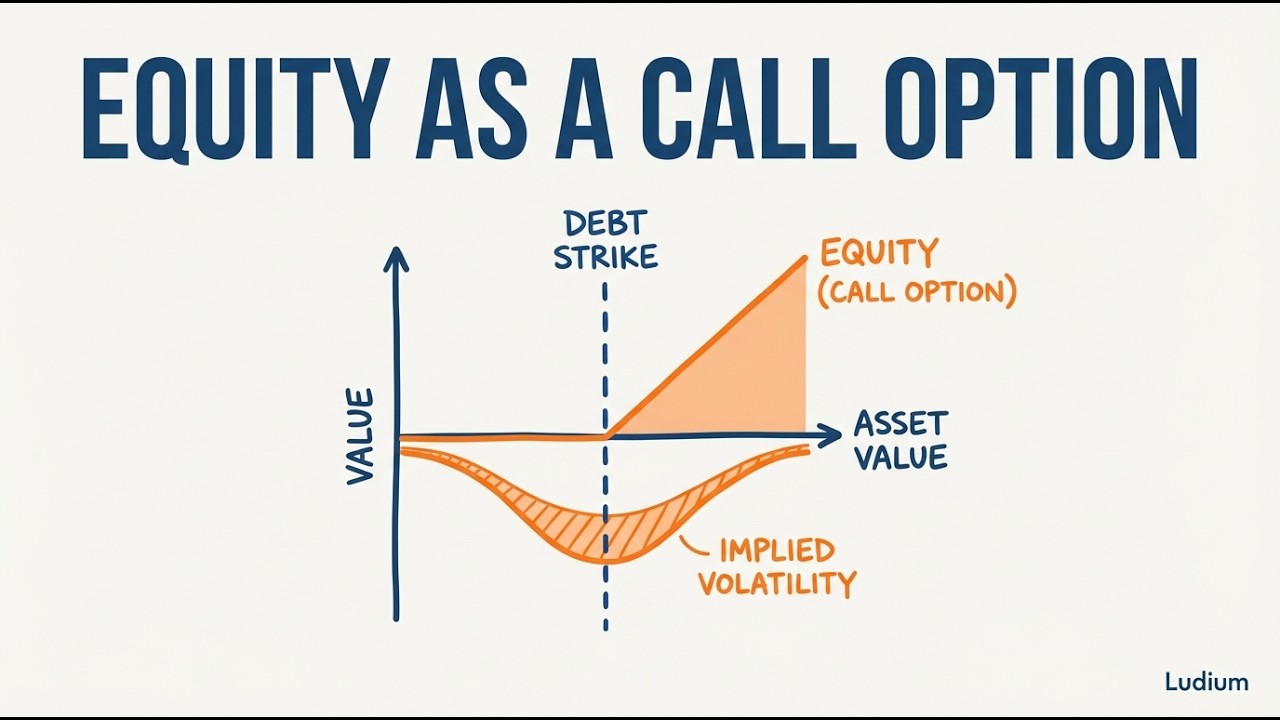

When the VIX spiked to 82.69 in March 2020, that number wasn't calculated from historical data — it was extracted from option prices using a powerful inversion of the Black-Scholes formula. This video explains how implied volatility works, how the VIX captures forward-looking fear, and then pushes the framework further: showing that a company's equity is mathematically identical to a call option on its assets, with the face value of debt as the strike price.

Key concepts covered:

• Implied volatility as the reverse-engineering of Black-Scholes

• Forward-looking vs. historical volatility

• How the CBOE constructs the VIX from S&P 500 options

• The term structure of implied volatility (temporary shocks vs. prolonged uncertainty)

• The Merton model: equity as a call option on firm assets

• Debt as a risk-free bond minus a put option

• The identity V = D + E and capital structure arbitrage

• Why asymmetric payoffs make volatility beneficial for option holders

• Options thinking applied to education, hiring, and venture capital

─────────────────────────────

ORIGINAL SOURCE

─────────────────────────────

This video distills concepts from the following source:

• Ses 11: Options II

All credit for the original content belongs to the original creator.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: