Statistics and Risk Modeling

Создание сводки PDF-файла с помощью Python и отображение ее с помощью FastAPI

Normal Inverse Gaussian Process in Python

Variance Gamma Process in Python

Merton Jump-Diffusion Process in Python

Mean Reversion Trading Strategy in Python

Tracking Ornstein-Uhlenbeck Process in Python

Bond Pricing by Vasicek Model in Python

Моделирование процесса Орнштейна-Уленбека на Python

Building Trinomial Tree for CIR Model in Python

Variance Reduction in Hull-White Using Moment Matching

Kirk Formula and Modified Kirk Formula for Spread Option Pricing in Python

Building Trinomial Tree for Black Karasinski Model in Python

Option Pricing with Heston Model in Python

Hull White Term Structure Simulations in Python

Building XGBoost Model in Python

Bitcoin Price Prediction using Machine Learning in Python

Main Concepts and Implementation of gRPC

Credit Risk Modeling in Python (Part 2) (Modeling)

Credit Risk Modeling in Python (Part 1) (Data Analysis)

Heston Model Simulation in Python

Build a Simple ZeroMQ in CSharp

Pick Right Trading Strategy with the Hurst Exponent

Predict Interest Rate with Calibrated CIR Model

Object Detection with Tensorflow in Python

PCA & Monte Carlo Simulation for Vasicek Model in Python

Black Karasinski Model & Calibration in Python

Choose the Optimal Learning Rate with Python

Comparison between Bachelier and Black Scholes Models

Сравнение сигмоиды и функции активации Softmax с Python

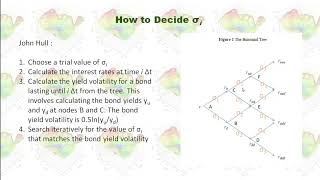

Постройте дерево биномиальной процентной ставки с помощью игрушечной модели Black Derman