Finance Theory — 15.5: The Market Portfolio

Автор: Ludium

Загружено: 2026-02-18

Просмотров: 3

Описание:

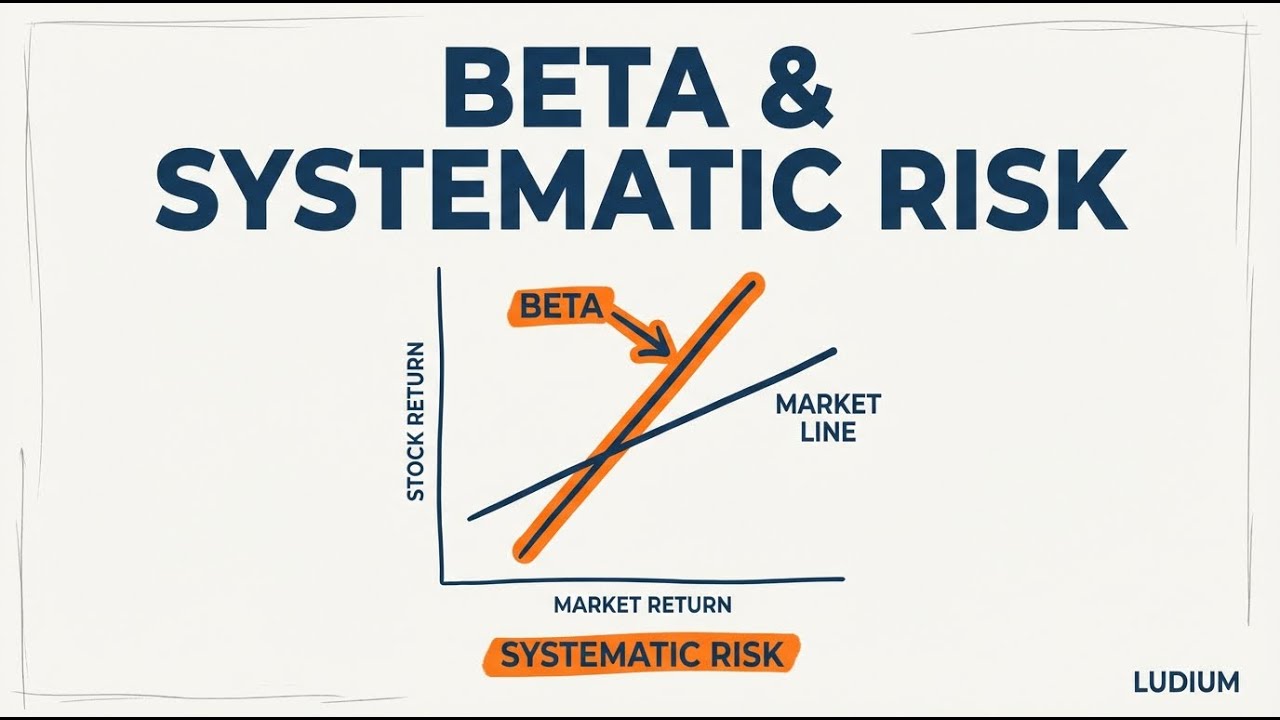

Why should a hedge fund manager borrowing millions and a retiree holding mostly Treasury bills own the exact same risky portfolio? Nobel Prize-winning theory shows that the optimal risky portfolio isn't a secret formula — it's the entire market, cap-weighted, available to anyone through a low-cost index fund. This video walks through the logic from Markowitz's efficient frontier to Sharpe's Capital Market Line to arrive at this powerful result.

Key concepts covered:

• The efficient frontier: the set of portfolios offering the highest expected return for each level of risk

• The Capital Market Line (CML): combining a risk-free asset with the tangency portfolio M to dominate the entire frontier

• The Sharpe ratio and why portfolio M maximizes return per unit of risk

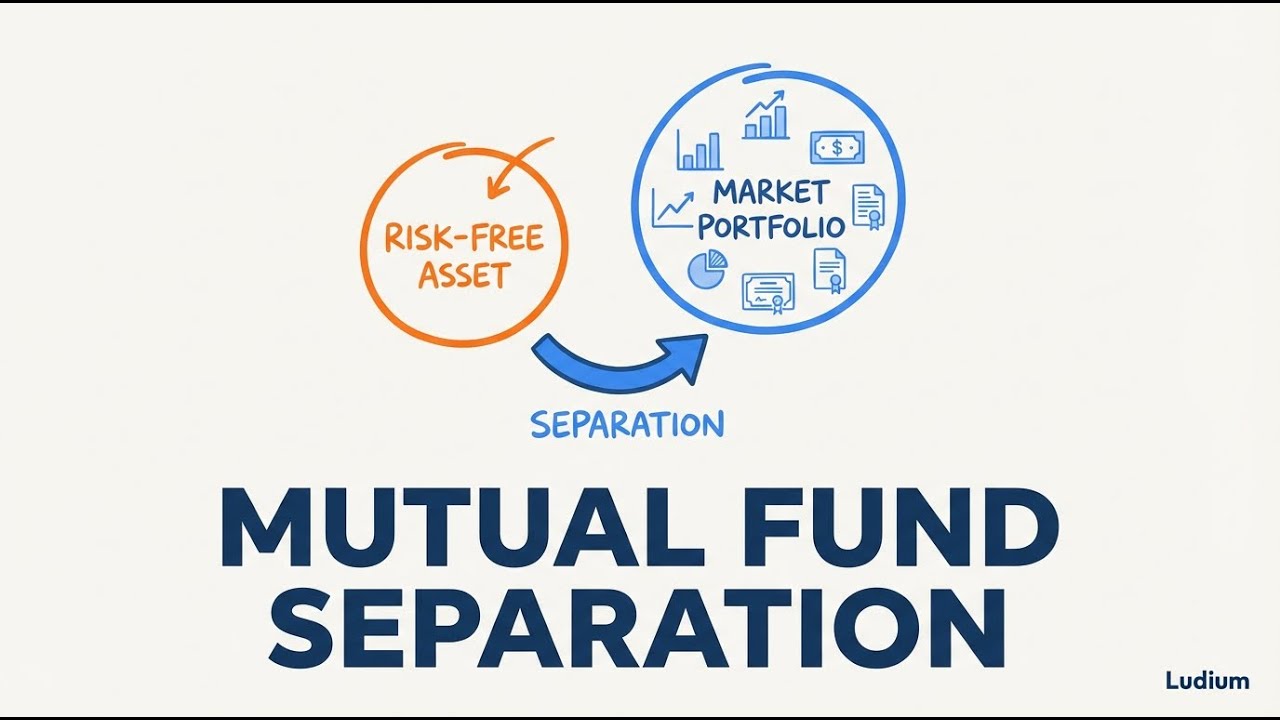

• Two-fund separation: all investors hold the same M, adjusting risk tolerance only by mixing M with T-bills (or leveraging)

• Market clearing argument: aggregating all investors' holdings proves M must be the cap-weighted market portfolio

• Why every stock with positive market cap earns its place — the role of the full covariance matrix and correlation benefits

• The market portfolio is naturally long-only with all positive weights

• Practical approximations: S&P 500, Russell 2000, and total market index funds

• 20-year comparison of S&P 500 vs. Russell 2000 showing similar trajectories with meaningful divergences

• Why index investing is mathematically optimal, not just settling for average

• Preview of the Capital Asset Pricing Model (CAPM) and individual stock pricing

━━━━━━━━━━━━━━━━━━━━━━━━

SOURCE MATERIALS

The source materials for this video are from • Ses 15: Portfolio Theory III & The CAPM an...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: