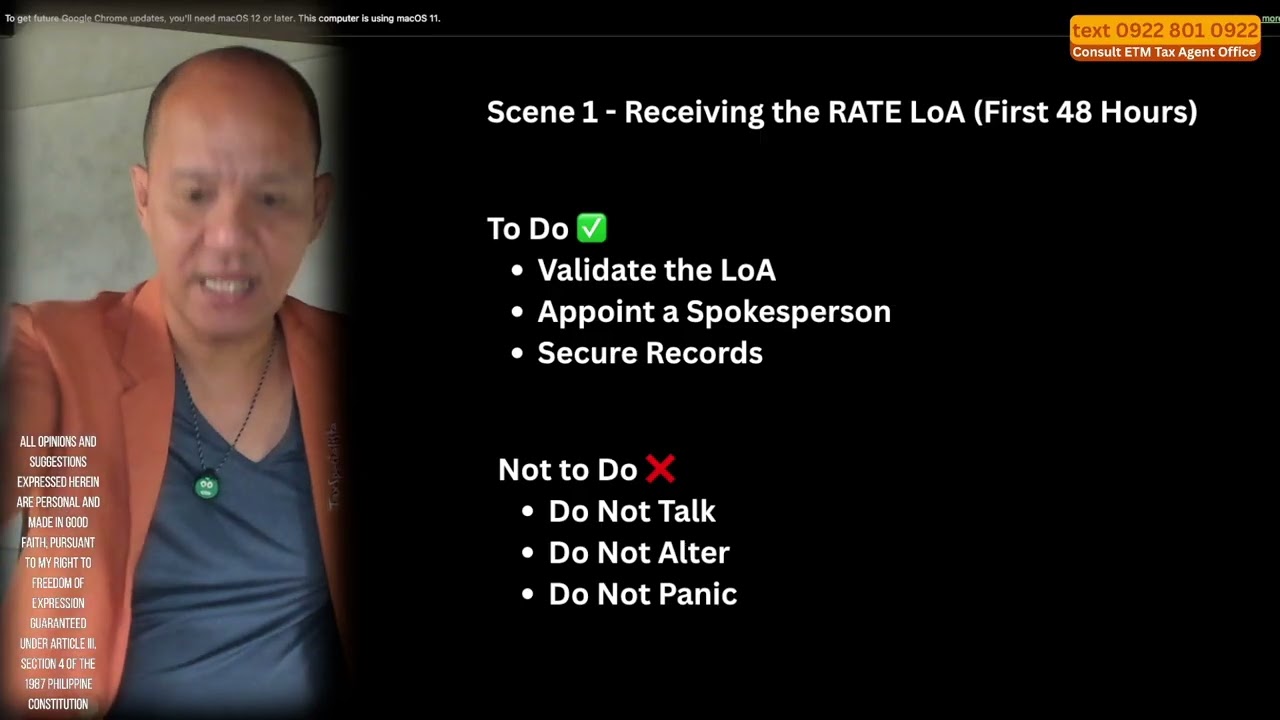

2 Things to Do When 2nd Request was Served to You: The Acclimation

Автор: TaxSpecialista

Загружено: 2018-08-01

Просмотров: 243

Описание:

It is the responsibility of the taxpayers to comply with the

requests of the BIR to produce their books of accounts

and/or other records and documents in the course of a tax

investigation and/or access to records requests. Those

who will refuse to produce the requested documents and

records will be dealt with in accordance with these

guidelines.

After ten (10) calendar days from receipt of a Letter of

Authority (LA) and checklist of the requirements for the

audit or access to records request, a First Notice will be

issued to the taxpayer by the revenue officer signed by

himself and/or his group supervisor. If the taxpayer

ignores and continues to disregard the demand for the

submission of the required documents, a Second and

Final Notice signed by the Head of the Office concerned

shall be sent to the taxpayer after ten (10) calendar days

from receipt of the First Notice.

If the First and Second Notice fails to convince the

taxpayer to comply with the requirements the Head of the

Office shall request the issuance of a Subpoena Duces

Tecum (SDT) from the Legal Service of the BIR National

Office, Legal Division of the Regional Office, or any

other authorized office after ten (10) calendar days from

receipt of the Second and Final Notice. The authorized

office shall act on the request for the issuance of SDT

within five (5) calendar days from receipt of such request.

The SDT must be served immediately and the revenue

officer shall return a served copy to the office who issued

the same within five (5) calendar days from issuance

thereof.

Any taxpayer who refuses to comply with the subpoena

duces tecum may be charged of a criminal case against

the taxpayer for violation of Section 5 in relation to

Sections 14 and 266 of the National Internal Revenue

Code and/or may be charged for contempt under Section

3(f), Rule 71 of the Revised Rules of Court.

When there is a request for the dismissal of the cases

filed in court, the BIR shall concur upon payment of ten

thousand pesos (PHP 10,000.00) as penalty for the

delayed compliance and violations of pertinent revenue

regulations and upon submission of the requested

information.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: