Financial Correlation Modeling – Bottom-Up Approaches (FRM Part 2 2025 – Book 1 – Chapter 9)

Автор: AnalystPrep

Загружено: 2020-04-08

Просмотров: 17656

Описание:

Master Financial Correlation Modeling for FRM Part 2 – Book 1 (Market Risk Measurement & Management). This lesson demystifies the bottom-up approach using the Gaussian copula, from mapping unknown marginal distributions to the standard normal, to estimating joint default probabilities and scaling to multi-asset portfolios with a correlation matrix. Clear analogies + a worked bond-default example.

You’ll learn to:

Explain copulas and why correlation alone can mislead

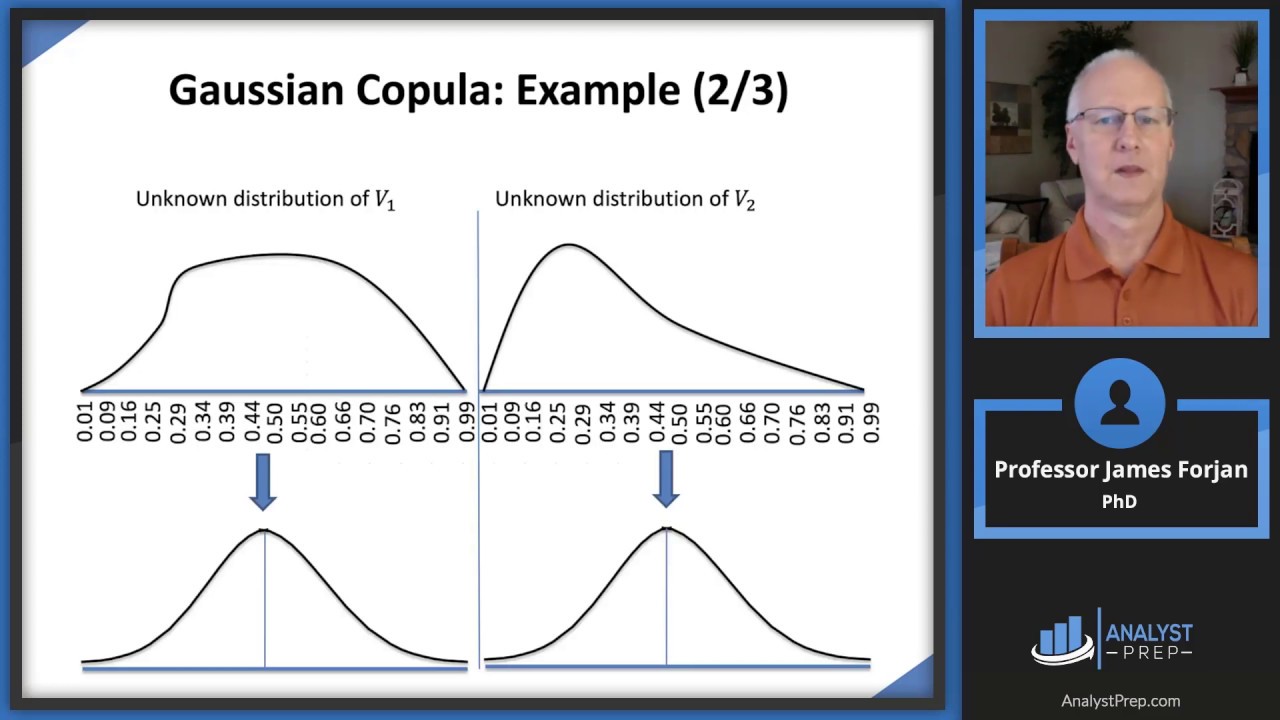

Map unknown distributions → standard normal (Sklar’s theorem idea)

Estimate joint default probability for two bonds

Extend to n assets, CDS/CDO applications, and Monte Carlo intuition

For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: https://analystprep.com/shop/unlimite...

AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams

After completing this reading you should be able to:

Explain the purpose of copula functions and the translation of the copula equation.

Describe the Gaussian copula and explain how to use it to derive the joint probability of default of two assets.

Summarize the process of finding the default time of an asset correlated to all other assets in a portfolio using the Gaussian copula.

#FRM #FinancialRiskManagement #GaussianCopula #CreditRisk #QuantFinance #MarketRisk #Copula #JointDefault #Correlation #AnalystPrep

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: