Court Holds FBAR Error on Schedule B (Foreign Accounts) Can Still be Non-Willful - Golding & Golding

Автор: Golding & Golding. Offshore Tax. Board-Certified

Загружено: 2024-07-27

Просмотров: 133

Описание:

https://www.goldinglawyers.com/court-...

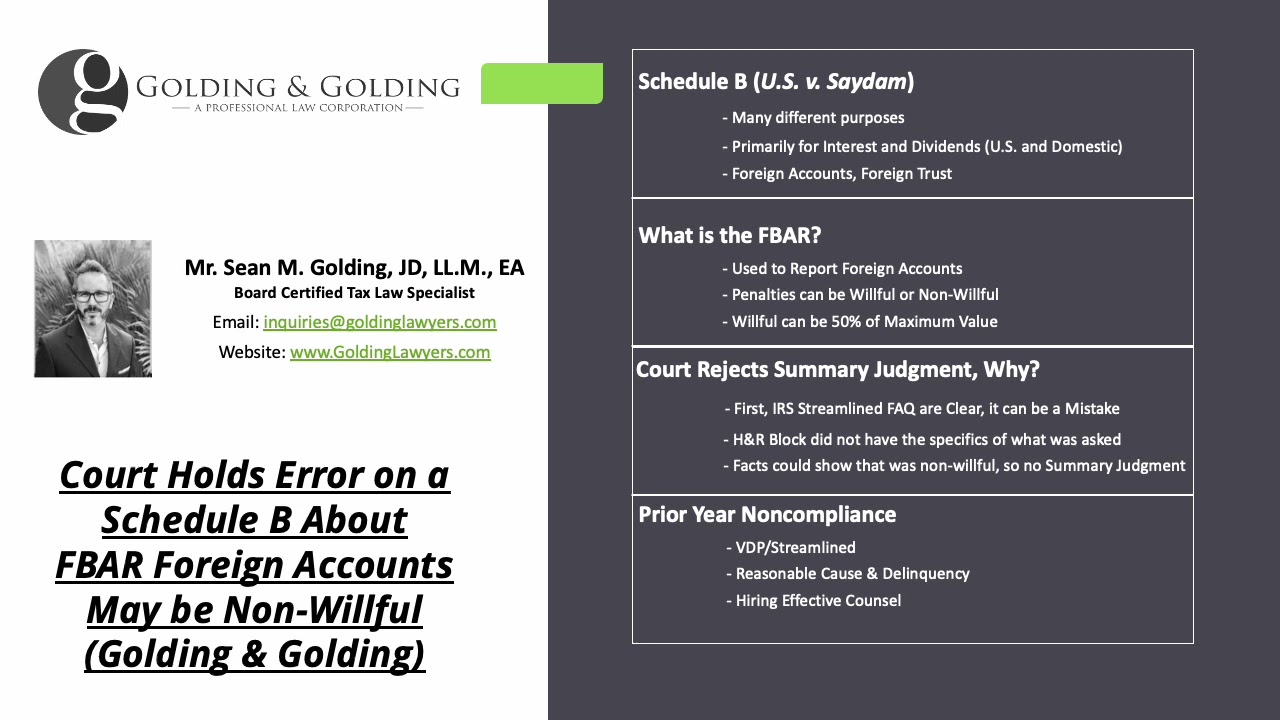

Court Rejects Government's Schedule B FBAR Summary Judgment

U.S. Taxpayers who have ownership or signature authority over foreign accounts are required to file a form Schedule B each year to report their ownership or signature authority as part of their IRS Form 1040. This is the case, even if the U.S. Taxpayer is ultimately not required to file the FBAR. Schedule B is used to report several different items – with a primary focus on reporting dividends and/or interest income (domestic or foreign). It is only on the bottom third portion of Schedule B where a taxpayer must identify that they have ownership or signature authority over a foreign account -- even if they are not required to file the FBAR. Thus, it is not uncommon for taxpayers to be blissfully unaware that they must file Schedule B, especially in situations in which they have no dividends or interest. Likewise, Taxpayers may file Schedule B but have not reviewed the form in its entirety before filing, because they do not have any dividends or interest, and trust that their preparer completed the form correctly. In the recent 2024 case of Saydam, the Taxpayer was required to file an FBAR (but did not do so) and also did not identify in his Schedule B that he had foreign accounts. The government used this fact as primary support for its motion for summary judgment, but the court disagreed and rejected the motion.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: