Fama French Three Factor Model

Автор: Edspira

Загружено: 2018-10-21

Просмотров: 117098

Описание:

This video discusses the Fama-French three-factor asset pricing model.

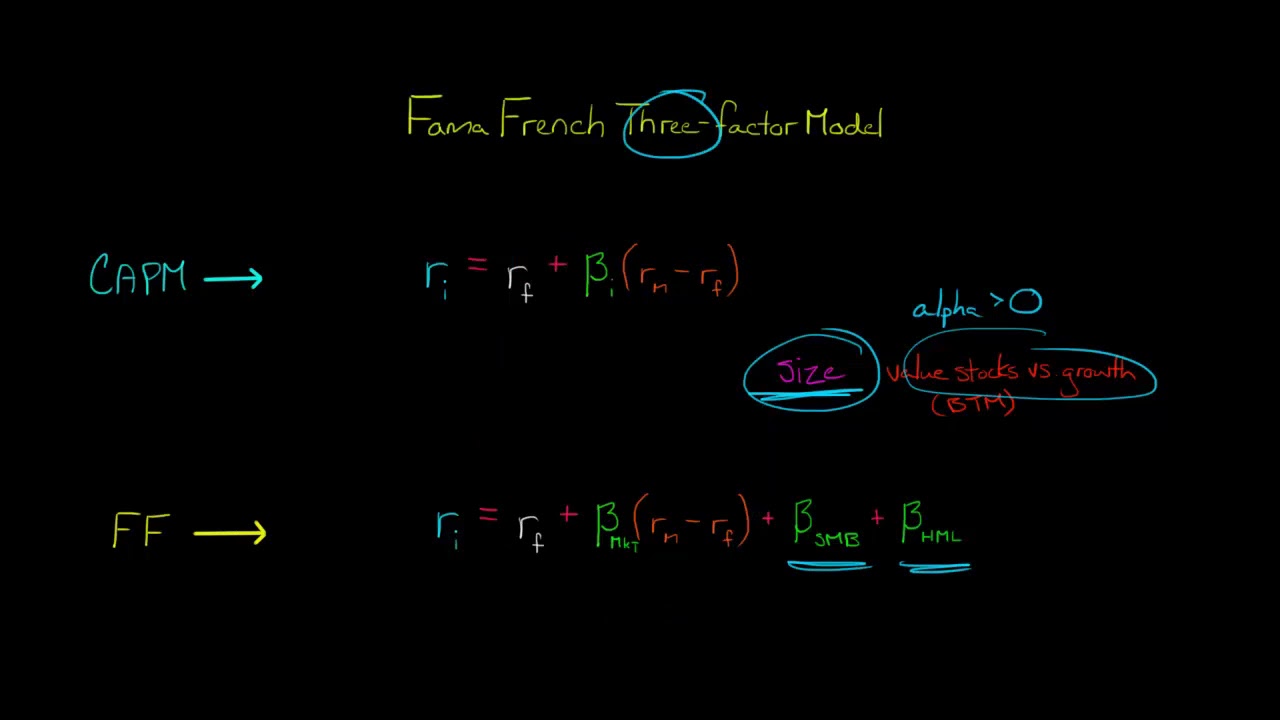

The Fama-French Model is a three-factor model that shows how market risk, firm size, and book-to-market ratio affect the expected retursn of a security. The Capital Asset Pricing Model shows the expected return of a security as function of the security's systematic risk (measured by beta), but Gene Fama and Kenneth French noticed that small-cap stocks (companies with smaller market capitalizations) tended to outperform large-cap stocks and that companies with a higher book-to-market ratio (value stocks) tended to outperform companies with a lower book-to-market ratio (growth stocks). Fama and French incorporated these factors into a new asset pricing model, which shows the expected return of a security as a function not just of market risk but of firm size and the book-to-market ratio.

The additional factors added by Fama and French are typically written as SMB and HML, with SMB meaning "small minus big" and HML meaning "high minus low." SMB represents the return from going long on stocks that have lower market capitalizations and selling short stocks that have higher market capitalizations. HML represents the return from going long on firms that have higher book-to-market ratios and selling short firms that have lower book-to-market ratios.—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

http://eepurl.com/dIaa5z

—

SUPPORT EDSPIRA ON PATREON

* / prof_mclaughlin

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

https://edspira.thinkific.com

—

LISTEN TO THE SCHEME PODCAST

Apple Podcasts: https://podcasts.apple.com/us/podcast...

Spotify: https://open.spotify.com/show/4WaNTqV...

Website: https://www.edspira.com/podcast-2/

—

GET TAX TIPS ON TIKTOK

/ prof_mclaughlin

—

ACCESS INDEX OF VIDEOS

https://www.edspira.com/index

—

CONNECT WITH EDSPIRA

Facebook: / edspira

Instagram: / edspiradotcom

LinkedIn: / edspira

—

CONNECT WITH MICHAEL

Twitter: / prof_mclaughlin

LinkedIn: / prof-michael-mclaughlin

—

ABOUT EDSPIRA AND ITS CREATOR

https://www.edspira.com/about/

https://michaelmclaughlin.com

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: