Navigating Market Breadth: Signals and Risks in Equity Strategies

Автор: 中環十一少 Mr.11

Загружено: 2024-12-23

Просмотров: 30

Описание:

One of the key technical factors analysts has been using over time to gauge the health of equity markets is the breadth of participation by the underlying stocks. Recently, we have fielded many questions from clients about breadth, as many have noted that December has exhibited some of the worst breadth in history while stock indices have remained near all-time highs. This anomaly is unusual, but some have concluded that breadth may not matter as much as in the past as a signal for price. In my experience, ignoring breadth is usually a bad idea, and this past week suggests that breadth has anticipated what we learned on Wednesday – i.e., the Fed may not be able to deliver as much accommodation as markets were expecting. Interestingly, the deterioration in breadth that started at the beginning of December coincided with a steady climb in 10-year UST yields, ultimately rising above our key 4.5% threshold where we’ve seen rates become a headwind for stocks. Indeed, the correlation with equity multiples flipped to negative when this occurred.

Another consideration is the growing propensity of investors to use price momentum as a key factor in their investment strategy. Rebalancing has also been de-emphasized as many investors have let their winners run, given the lack of mean reversion in the past several years. This all helps to explain the extreme concentration we’re seeing in many equity markets, not just in the United States. As I noted in my Sunday Start last month, quality is a very crowded factor, and it’s a global phenomenon. In fact, quality is more expensive outside the US, given the lower proportion of quality companies in ROW indices. This is a major reason why the S&P 500 trades at a substantial premium to foreign indices and lower-quality cohorts like small- and mid-caps. Nevertheless, this focus on price momentum and the resulting concentration may explain the disconnect between breadth and price and why many were willing to ignore its warning until this week.

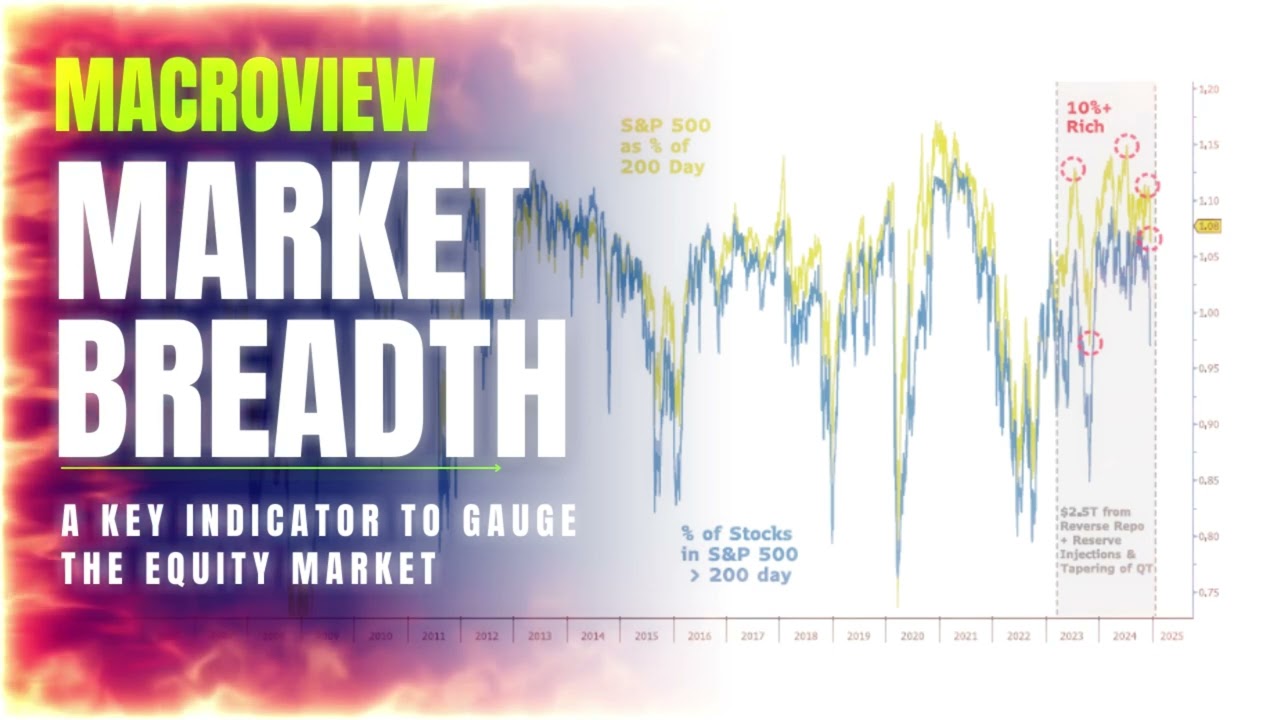

To add to this last point, the appeal of large-cap quality and momentum strategies, combined with the advent of low-cost passive investment products, has led to a persistently wider premium/spread in a relationship I watch closely – the S&P 500 index as a percentage of its 200-day moving average versus the percentage of S&P 500 stocks trading above their 200-day moving average.

For most of the past 25 years, these ratios have traded in lock step, with divergences normalizing quickly. However, over two extended periods, the divergences remained wide for longer than normal – i.e., the S&P 500 index traded “rich” relative to this measure of breadth. Those periods were 1999 and April 2023 to today. Beyond the drivers mentioned above, some of which were absent in the late 1990s, these two periods share an important similarity – the generous liquidity provided by the Fed and/or the Treasury. In 1999, the Fed arguably maintained an excessively loose policy as a precaution against Y2K transition risk at year-end. Once the new year arrived without complications, liquidity was tightened and the spread in these ratios promptly narrowed.

Today, the persistently wider spread in the ratios shown below began when the US$2.5 trillion reverse repo facility (RRP) peaked in April 2023. This divergence also coincided with the US$500 billion injection of reserves to stem the flight of bank deposits post the regional bank failures that spring. The question now is, will draining the RRP to zero and the Fed cutting less than expected set the stage for a tightening of liquidity early next year that closes this spread? Or can liquidity remain robust, with the Fed surprising on the upside with more cuts than expected and/or ending QT? It’s hard to know, but the anomaly between breadth and price that so many are highlighting could normalize if/when the abundance of liquidity subsides. Furthermore, breadth may not matter as much as it has in the past for high-quality indices with the greatest price momentum. More specifically, we think this is another strong argument to stay up the quality curve for now. Based on the reset in stock prices this past week, expensive/unprofitable growth stocks and low-quality cyclicals appear to be the most vulnerable to potentially higher-for-longer interest rates and less liquidity as the RRP facility is wound down.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: