Willful vs Non Willful: IRS Updated Willfulness vs Non Willfulness for OVDP & Streamlined Offshore.

Автор: Golding & Golding. Offshore Tax. Board-Certified

Загружено: 2020-03-30

Просмотров: 761

Описание:

https://www.goldinglawyers.com

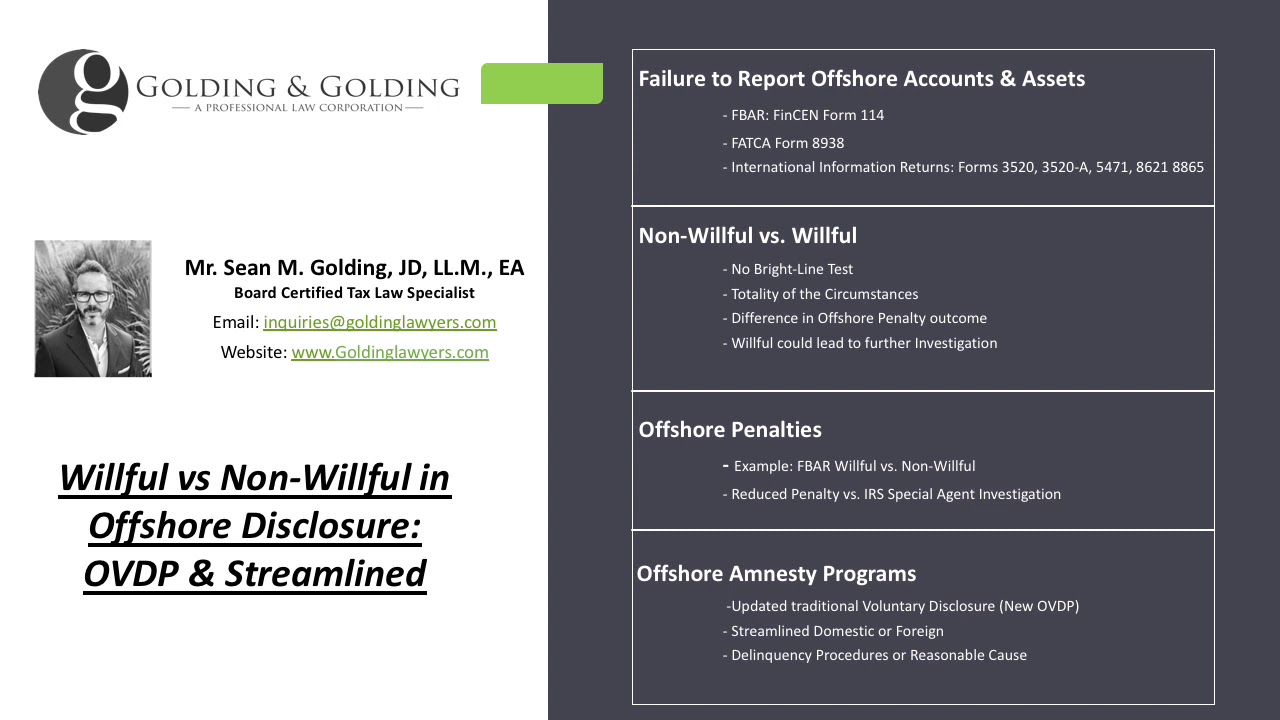

Willful vs. Non-Willful FBAR Penalty & the IRS

Willful vs. Non-Willful: Analyzing willful vs. non-willful is a complex undertaking. The IRS has not issued a bright-line test to determine if a person qualifies as non-willful with respect to offshore disclosure. The analysis of determining whether a person qualifies as willful or non-willful, is a very detailed evaluation. When determining whether a taxpayer is willful vs. non-willful, and should submit to either the streamlined procedures or OVDP (New 2020 version), it is important that the taxpayer speaks with highly-experienced counsel. This is especially true, since the Internal Revenue Service is taking an aggressive position on matters involving foreign accounts compliance and unreported offshore income.

The failure to get into compliance timely, may result in significant offshore fines and penalties.

What is Willful vs. Non-willful?

When a Taxpayer learns that they are out of compliance for not properly reporting offshore accounts, assets, investments, and income – they get understandably nervous. The Internet is peppered with inexperienced tax attorneys who use fear mongering and scaremongering to try to goad taxpayers into hurried representation.

Oftentimes, these attorneys will simply mislead the taxpayer and submit them into the streamline program even when they are willful, and a streamlined submission is not warranted. This makes an otherwise complicated situation infinitely more complex.

*Here is a case study example of the perils of going this route with less experienced counsel.

Common Misconceptions about Willfulness & Non-Willfulness

There are many misconceptions about willful vs. non-willful.

Since there is no bright line test to determine willful versus non-willful, one method for helping taxpayers understand the analysis is to debunk some of the misconceptions out there involving offshore disclosure and foreign bank account/asset amnesty.

A. "No" On 1040 Schedule B is Automatic Willfulness

Just because a person checked “No” for Schedule B does not presume willfulness. There can be many reasons why a person checked “No.” In fact, some tax programs include “No,” as the automatic default. Therefore, marking "no" on 1040 Schedule B is not automatic willfulness.

B. Non-Transfer of Overseas Money to the U.S. is automatic Non-Willfulness

Many times a client will come to us and presume they are non-willful -- solely because the money was never transferred to the U.S.

This fact does not presume non-willfulness. For example, if a taxpayer intentionally hides money outside of the U.S., the mere fact that they have not accessed the (if they knew about the reporting requirements) does not presume they were non-willful.

C. Willfulness Requires Intent

Willfulness does not require intent. There are lower-levels of willfulness such as reckless disregard (which does not require intent) or willful blindness (which does not require actual knowledge). If a person is found to meet one of the lower levels of willfulness, they are still subject to the full FBAR willfulness penalty.

D. Minimal Unreported Income is Always Non-Willful

The amount of unreported income has no (direct) bearing on whether a person acted willful or non-willful. In other words, a person could have minimal unreported income, but had the actual knowledge that they were supposed to report the foreign accounts and income – this would presumably be considered willful.

E. OVDP was Terminated, with no “Willful” alternative

OVDP was terminated, but the traditional voluntary disclosure program was expanded to include new updated procedures for submitting to voluntary disclosure (VDP) in lieu of OVDP.

The above-referenced facts are just some of the common misconceptions involving willful vs. non-willful.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: