053 - Martyn Tinsley - 2 of 2 - Walk Forward Correlation: A New Tool for Robust Strategy Design!

Загружено: 2026-05-25

Просмотров: 6509

Описание:

Big discount on Martyn's tool for subscribers: https://www.algoadvantage.io/toolbox/

Watch Part 1 first! • 052 - Martyn Tinsley - 1 of 2 - Building R...

My detailed write up on Walk Forward Correlation Analysis: https://www.algoadvantage.io/podcast/...

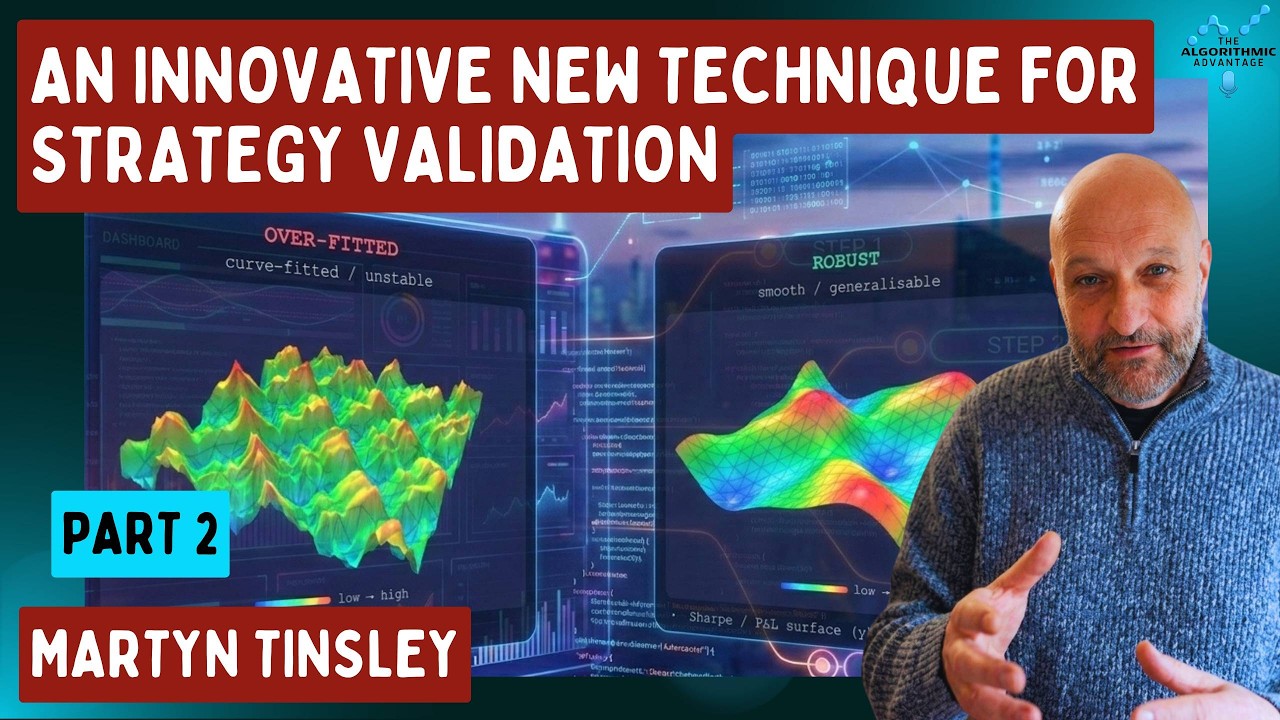

Martyn introduces Walk Forward Correlation (WFC) as a diagnostic for two problems that sit at the heart of systematic trading: over-fitting and structural edge. Traditional walk-forward analysis typically optimizes a strategy on an in-sample window, picks the “best” parameter set, then tests that one choice out-of-sample. Used the wrong way, there’s a potential flaw here: one parameter set can look good out-of-sample purely by accident. That tells you very little about whether the underlying model is genuinely robust.

Tinsley’s move is simple, but useful. Instead of judging one selected point, he looks at all parameter combinations in the optimisation grid and asks a harder question: does strong in-sample performance tend to map to strong out-of-sample performance across the whole space? If yes, you may have something real. If no, you’re probably flattering noise.

Contents:

0:00 Walk Forward Correlation Explained

4:22 Best Metrics for Strategy Selection

9:27 Building a Combined Performance Metric

13:05 Objective Functions and Walk Forward Tests

17:30 In-Sample vs Out-of-Sample Validation

22:28 Pre-Live Optimization for Live Trading

25:14 Why Traditional Walk Forward Falls Short

28:59 Walk Forward Correlation Method

32:28 Measuring Predictive Power in Trading

39:25 Reading Correlation Chart Scenarios

41:48 Trade Counts and Statistical Significance

45:52 Go/No-Go Gates for Robust Strategies

51:03 Optimize Strategy Software Overview

56:43 Final Thoughts for Systematic Traders

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: