Regulation S-X of the SEC Reporting Requirements. CPA Exam BAR

Автор: Farhat Lectures. The # 1 CPA & Accounting Courses

Загружено: 2023-11-19

Просмотров: 1222

Описание:

In this video, I explanation regulation S-X of the SEC reporting requirement as it is covered on the CPA exam BAR section.

✅https://farhatlectures.com/

0:00 Introduction

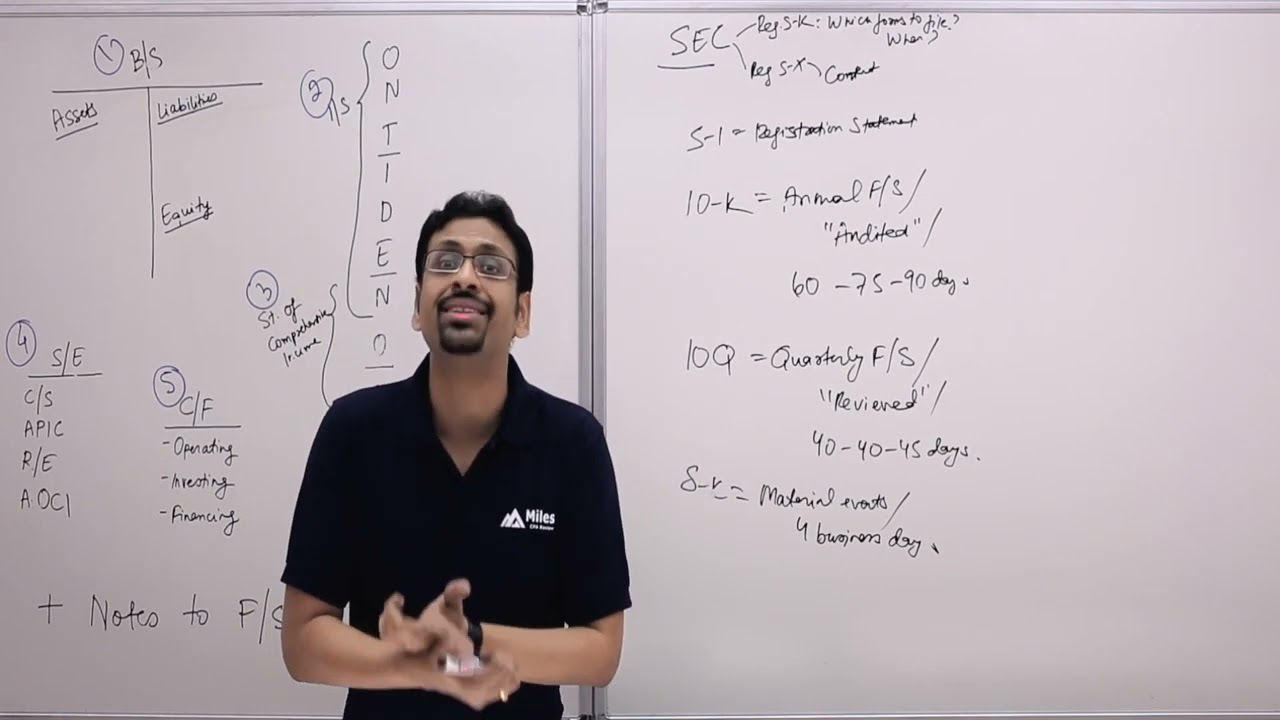

This video explains Regulation S-X, which dictates the form and content of financial reports for publicly traded companies, such as the quarterly 10-Q and annual 10-K reports (0:08, 0:17). Its purpose is to ensure uniformity in financial reporting.

Key points covered:

Regulation S-X vs. Regulation S-K: S-X deals with financial numbers, while S-K deals with qualitative descriptions (0:53).

Interim Financial Statements (e.g., 10-Q): These are for periods less than a full year and are subject to review, not a full audit (2:11, 2:23). They typically include the most recent fiscal quarter and the year-to-date period for income statements and cash flows, and the most recent quarter's balance sheet (2:38, 3:27). They can be condensed but must disclose any necessary adjustments (5:08).

Annual Reports (10-K): These must be audited (7:20, 7:23). The 10-K requires two years of audited balance sheets and three years of audited income statements, cash flow statements, and statements of changes in owner's equity (7:30, 7:36, 7:42, 7:52). They require extensive disclosures (7:58).

The video uses Amazon's financial statements as an example to illustrate how quarterly reports are presented (3:53).

CPA candidate or student? Start your free trial for more.

Regulation S-X, overseen by the Securities and Exchange Commission (SEC), establishes guidelines for how registrants must disclose financial statements in various filings. Its applicability extends to a wide range of documents, including registration statements for initial public offerings (IPOs) and shelf offerings, periodic reports, going-private statements, tender offers, proxy statements, and more. The regulation is divided into several key areas:

Qualifications and Reports of Accountants: Ensuring that auditors are qualified and independent, and setting requirements for accountants' reports.

General Instructions for Financial Statements: Mandating the filing of consolidated balance sheets, statements of comprehensive income and cash flows, and providing specific instructions for these statements. It also includes requirements for financial statements of acquired businesses, unconsolidated subsidiaries, and consolidated financial statements of the registrant and its subsidiaries.

Rules of General Application: Covering form, terminology, captions, omissions of unnecessary or identical information, and general notes to financial statements.

Specific Provisions for Certain Registrants: Catering to the unique requirements of insurance companies, smaller reporting companies, and similar entities.

Pro Forma Financial Information: Outlining requirements for pro forma financial information in registration statements following significant acquisitions

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: