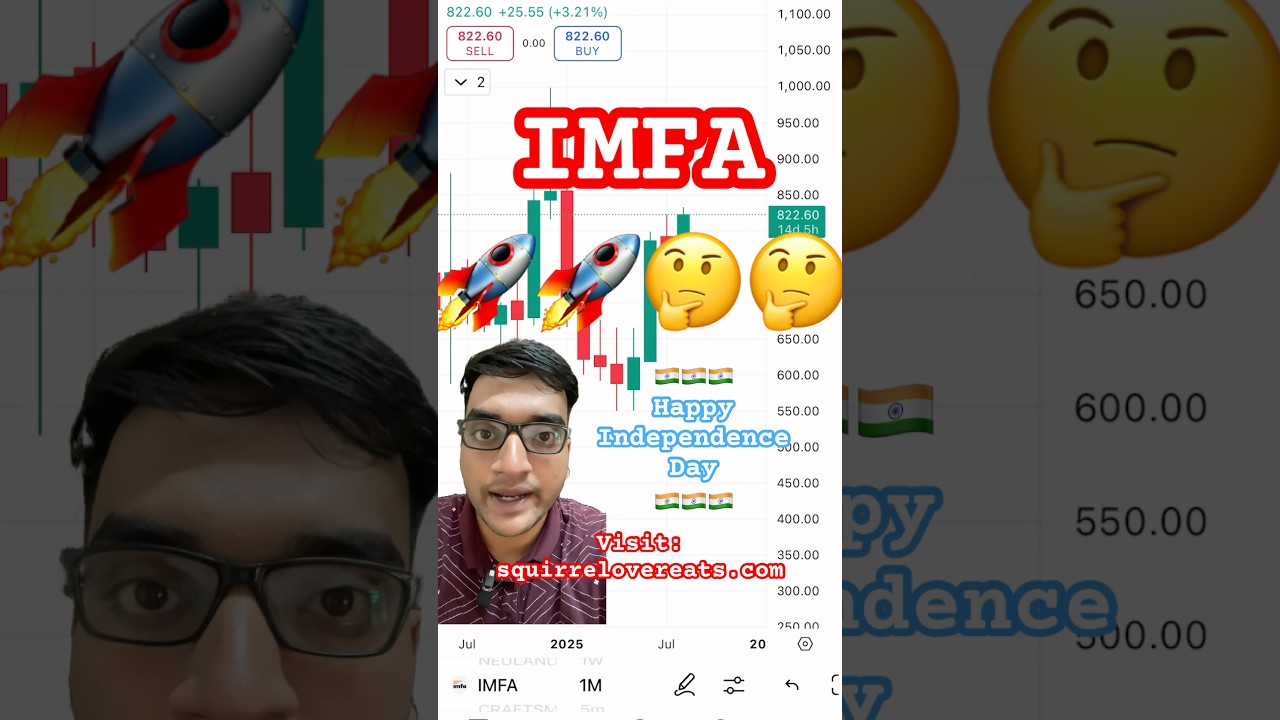

IMFA to fly high from September 2025??

Автор: Squirrel Overeats

Загружено: 2025-08-14

Просмотров: 312

Описание:

Indian Metals & Ferro Alloys Ltd – Integrated Ferrochrome Producer with Operational Resilience and Growth Capex

Business Overview

IMFA is one of India’s largest fully integrated producers of ferrochrome, supplying around 20% of domestic output and about 25% of exports to markets like China, Japan, and Taiwan. The company operates across chrome ore mining, ferro-alloys smelting, and captive power generation, with manufacturing units in Therubali and Choudwar, backed by captive mines and renewable power installations.

⸻

Q4 FY25 Performance

• Revenue dropped ~19% YoY to ₹567 crore, while EBITDA declined to ₹71 crore (margin around 12%). Net profit stood at ₹47 crore, up 34% YoY. Normalized EPS was ₹8.77.

• Despite subdued demand and pricing pressures, IMFA maintained profitability through cost optimization and efficient operations.

FY25 Annual Metrics

• Full-year revenue was ₹2,565 crore, down from ₹2,780 crore in FY24. EBITDA came in at ₹531 crore, and PAT stood at ₹378 crore (slight YoY improvement). Exports were ₹2,322 crore.

Q1 FY26 Quarter Highlights

• Revenue rebounded to ₹642 crore, EBITDA jumped to ₹125 crore (margin ~19.6%), and PAT improved to ₹91 crore. Ferrochrome production was ~65,929 tonnes, sales were ~66,580 tonnes. Export value was strong at ₹556 crore.

• The company remains debt-free, ensuring financial flexibility.

⸻

Expansion & Long-Term Strategy

• IMFA is progressing its greenfield ferrochrome expansion project in Kalinganagar, targeting commissioning by mid-FY26.

• A 110 MW hybrid renewable energy plant is in development under partnerships with JSW Green Energy and Ampin Energy Utilities.

• The merger of Utkal Coal Ltd into IMFA has been approved, enhancing resource integration.

⸻

Financial Health & Valuation

• ROCE stands at ~21%, ROE at ~17%, with a dividend yield of ~2.4%. P/E ratio is around 12–13× and book value is ₹435. The company’s sales growth has been modest (~9–10% over 5 years), but returns remain healthy.

• Balance sheet is robust, with increasing equity (~₹2,322 crore), minimal long-term debt, and strong working capital management. Cash flows are also solid.

⸻

Investment Summary

Highlights

• Fully integrated structure delivers resilience amid market cycles.

• Excellent margin control and debt-free status underpin financial strength.

• Strategic growth roadmap via capacity expansion and renewable energy ventures.

Risks

• Q4 cyclicality reflects sensitivity to ferrochrome demand and pricing.

• Expansion execution risk—timely commissioning is essential to sustain growth.

• Modest long-term sales growth underscores cyclical dependency.

⸻

Key Metrics to Monitor

• Q2-Q3 FY26 performance as Kalinganagar capacity ramps up.

• Ferrochrome realization and margin trends amid global demand recovery.

• Progress on renewable energy projects and integration of merged entities.

For more, visit:

squirrelovereats.com

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: