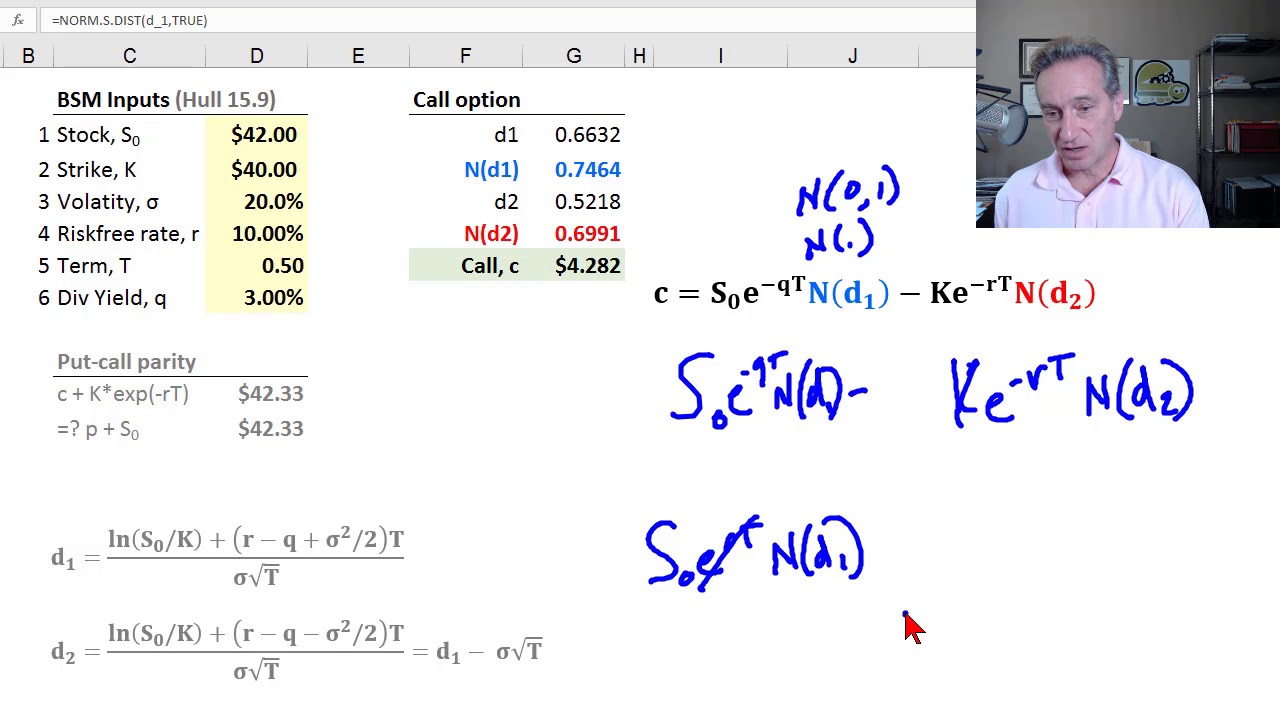

Black-Scholes Option Pricing in Excel

Автор: QuantPy

Загружено: 2020-05-23

Просмотров: 32211

Описание:

Implementation of the Black-Scholes Option Pricing model in Excel.

I apologise for missing to multiply the second term of the numerator in d1 by time T (don’t forget like I did).

★ A data driven path to getting a job in Quant Finance

https://www.quantpykit.com/

★ QuantPy GitHub

Collection of resources used on QuantPy YouTube channel. https://github.com/thequantpy

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: