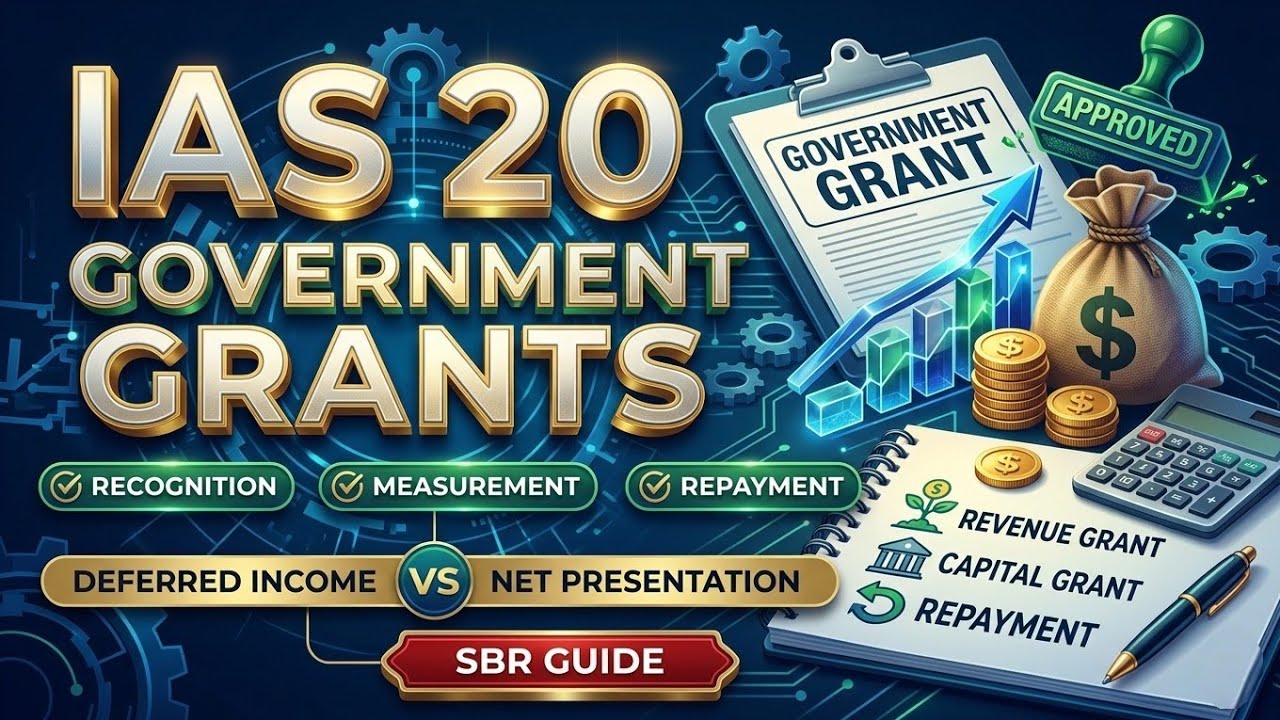

IAS 20 Government Grants fully explained Recognition, Measurement & Repayment (IFRS)

Автор: Finance Zaby

Загружено: 2026-03-09

Просмотров: 12

Описание:

Master IAS 20 Government Grants in this clear, exam-focused video. Learn definitions, recognition rules, measurement choices (deferred income vs net presentation), repayment accounting with journal entries, and required disclosures — perfect for ACCA//IFRS students.

What you’ll learn

✅ What a government grant is (simple definition + example)

✅ Difference between revenue and capital grants

✅ Recognition criteria and when to treat assistance as non-monetary (training)

✅ Two measurement/presentation methods: Deferred-income (liability) vs Net presentation (deduct from asset)

✅ How to account for partial and full repayments under both methods (journal entries + P&L effects)

✅ Practical example worked through (asset cost, grant amount, useful life)

✅ Disclosures required under IAS 20 and exam answering tips

Worked Example (short)

Asset cost = $50,000; Grant = $10,000; Life = 5 years

Deferred-income method: record asset at full cost, liability = $10,000; recognize $2,000 grant income each year.

Repayment: if full repayment after 3 years, remaining deferred income $4,000 → immediate derecognition; remaining $6,000 already recognized → loss = $6,000.

#IAS20 #GovernmentGrants #IFRS #Accounting #ACCA #ExamPrep #SBR #FR

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: