Risk Capital Attribution and Risk-Adjusted Performance Measurement (FRM Part 2 – Book 3 – Ch 12)

Автор: AnalystPrep

Загружено: 2020-07-22

Просмотров: 8527

Описание:

Master Risk Capital Attribution and Risk-Adjusted Performance Measurement (RAROC) for FRM Part 2 (Book 3, Ch. 12). We clarify risk capital vs. economic/regulatory capital, show how to compute RAROC with a full banking example, link it to hurdle rates and CAPM, and discuss VaR scaling (square-root-of-time), capital allocation, diversification benefits, and best practices.

You’ll learn to:

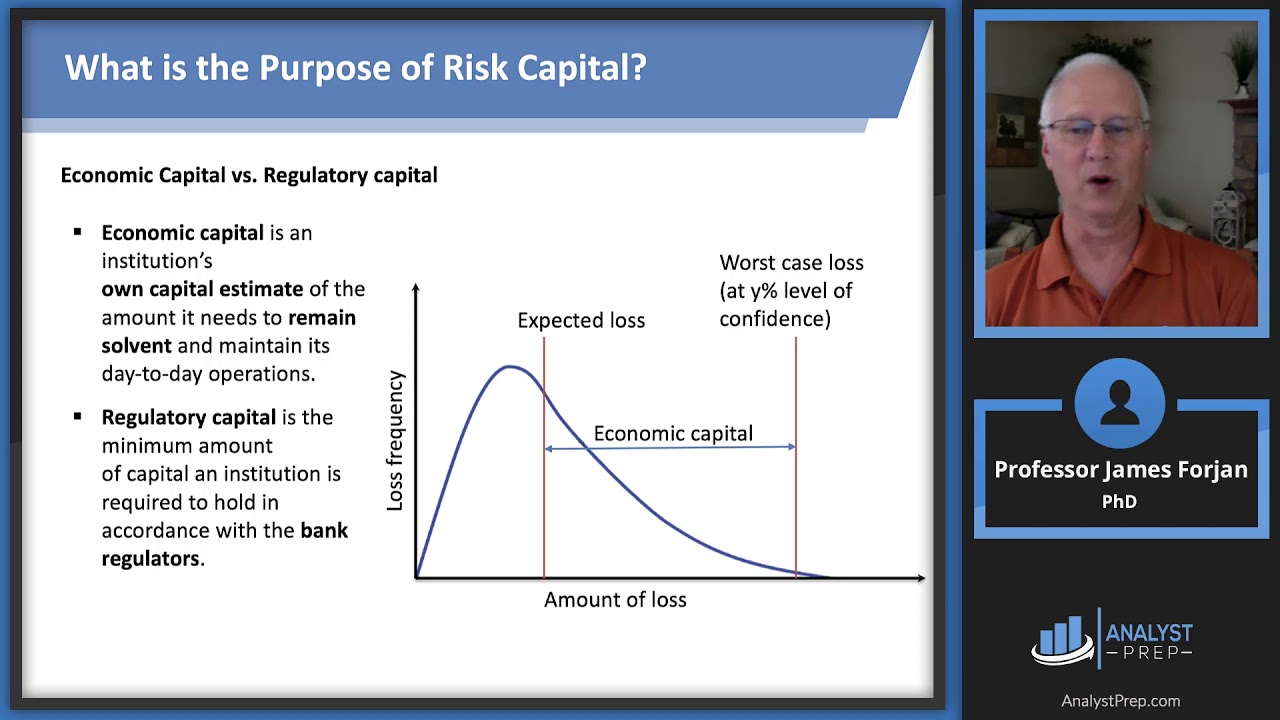

Define risk, economic, and regulatory capital and their purposes.

Compute and interpret RAROC and adjusted RAROC.

Set and test a hurdle rate (cost of equity via CAPM, preferred equity).

Treat risk capital as VaR and annualize via the square-root-of-time rule.

Allocate capital across business lines and handle diversification effects.

For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: https://analystprep.com/shop/unlimite...

AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams

After completing this reading, you should be able to:

Define, compare and contrast risk capital, economic capital and regulatory capital, and explain methods and motivations for using economic capital approaches to allocate risk capital.

Describe the RAROC (risk-adjusted return on capital) methodology and its use in capital budgeting.

Compute and interpret the RAROC for a project, loan, or loan portfolio and use RAROC to compare business unit performance.

Explain challenges that arise when using RAROC for performance measurement, including choosing a time horizon, measuring default probability and choosing a confidence level.

Calculate the hurdle rate and apply this rate in making business decisions using RAROC.

Compute the adjusted RAROC for a project to determine its viability.

Explain challenges in modeling diversification benefits, including aggregating a firm’s risk capital and allocating economic capital to different business lines.

Explain best practices in implementing an approach that uses RAROC to allocate economic capital

#FRM #FRMPart2 #RiskCapital #RAROC #OperationalRisk #CreditRisk #MarketRisk #ValueAtRisk #GARP #AnalystPrep

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: