Скачать

FRM: Intuition behind the Black-Scholes-Merton

Автор: Bionic Turtle

Загружено: 2008-05-29

Просмотров: 85334

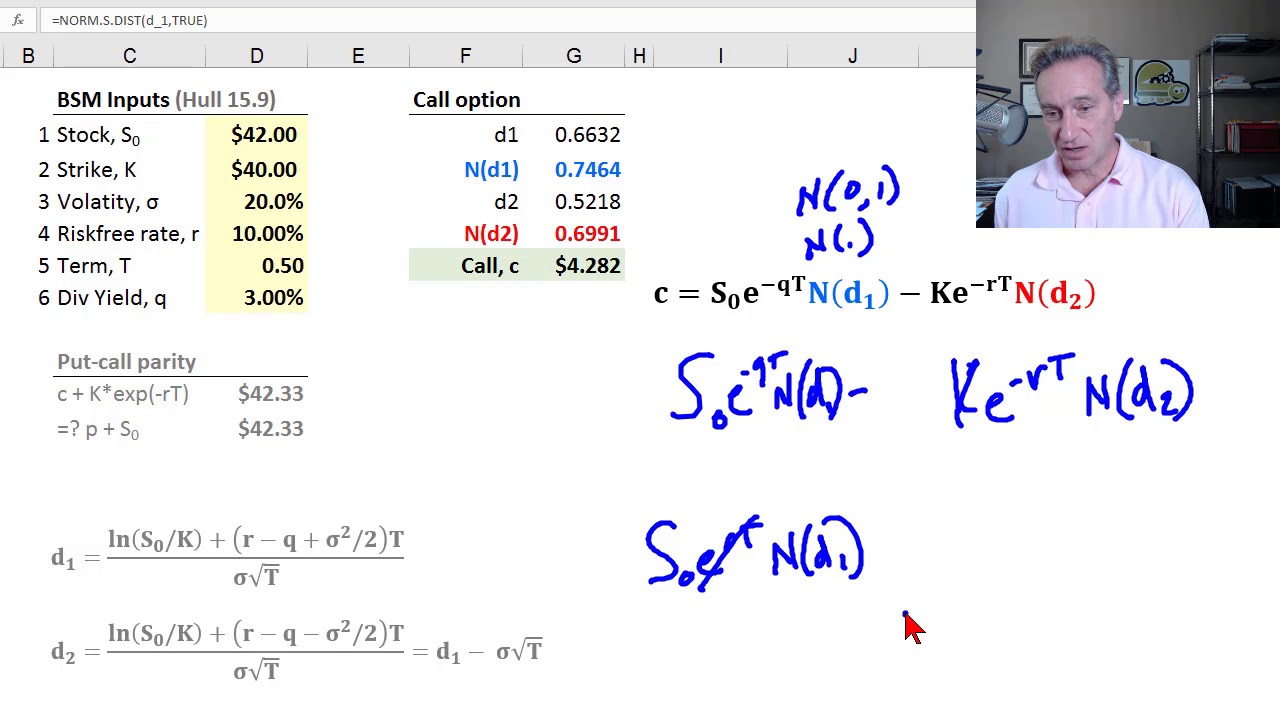

Описание: The value of a European call must be equal to a replicating portfolio that has two positions: long a fractional (delta) share of stock plus short a bond (where the bond = strike price). For more financial risk videos, visit our website! http://www.bionicturtle.com

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: