Скачать

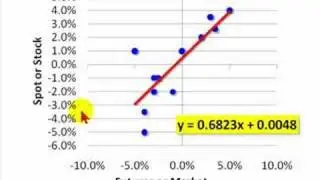

FRM: How to get portfolio variance/VaR from the covariance matrix

Автор: Bionic Turtle

Загружено: 2008-08-08

Просмотров: 63008

Описание: To get portfolio variance, we post-multiply the vector of positions (x) by the covariance matrix, then pre-multiply the transposed vector (x'). For more financial risk videos, visit our website! http://www.bionicturtle.com

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![[2026] Feeling Good Mix - English Deep House, Vocal House, Nu Disco | Emotional / Intimate Mood](https://image.4k-video.ru/id-video/cxLdtvzf2sI)