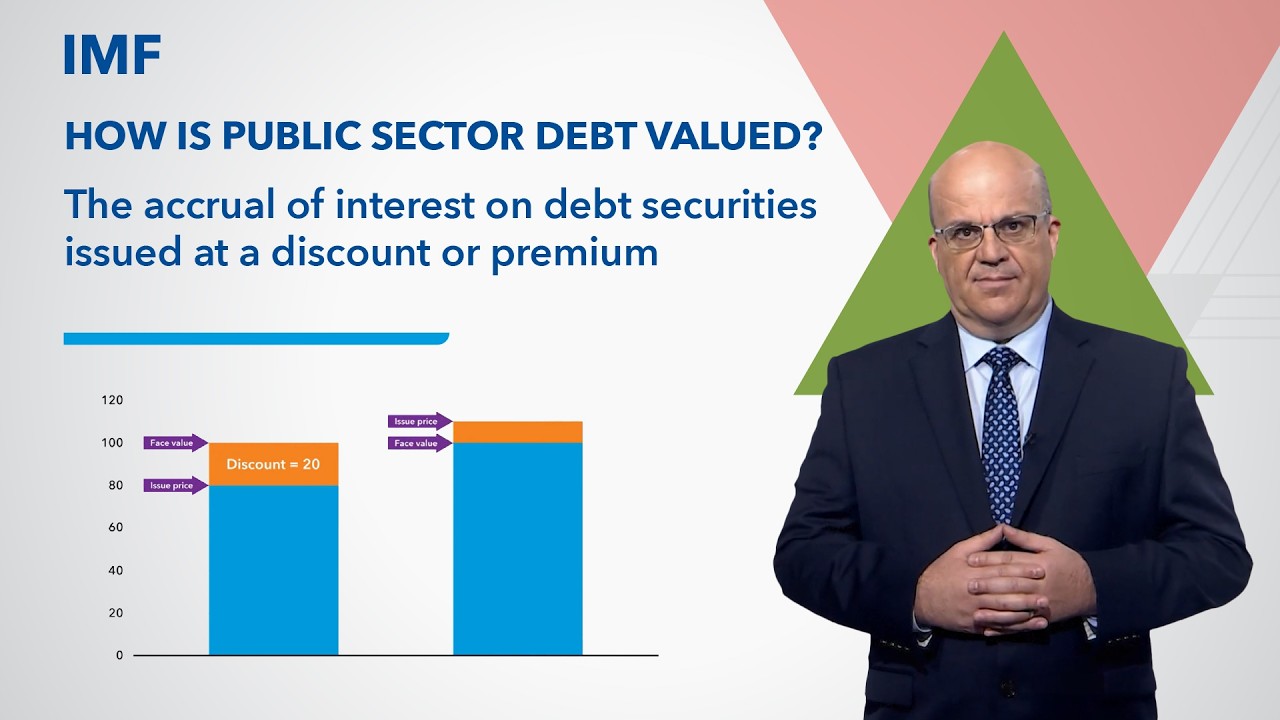

The accrual of interest on debt securities issued at a discount or premium

Автор: IMF Institute Learning Channel

Загружено: 2020-05-26

Просмотров: 1085

Описание:

A discount or a premium means that the issue price and par value (also called face value) of the debt security are different. A debt security is issued at a discount when the issue price is below the par or face value of the debt security. A debt security is issued at a premium when the issue price is above the par or face value of the debt security.

On an accrual basis of recording, interest on a debt security issued at a discount or premium may consist of one or two components: (1) Only interest that accrues is from the discount or premium, such as short-term bills of exchange and zero-coupon bonds; and (2) Interest accrues from the discount or premium and from the coupon, such as deep-discounted bonds, which require periodic coupon payments in addition to interest accruing from the discount/premium.

On a cash basis, interest is recorded only when the cash payment takes place: (1) For a debt security issued at a discount, the interest resulting from the discount is paid and recorded at maturity; and (2) For a debt security issued at a premium, the full amount of the premium is recognized as a negative interest expense at the time of issuance.

The accrual of interest in macroeconomic statistics is introduced here:

• The accrual of interest in government fina...

Link to the IMF online course on public sector debt statistics for government officials: https://www.imf.org/en/Capacity-Devel...

Link to the IMF online course on public sector debt statistics for members of the general public: https://www.edx.org/course/public-sec...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: