Finance Theory — 14.6: Risk Parameter Estimation and Stationarity

Автор: Ludium

Загружено: 2026-02-16

Просмотров: 6

Описание:

How much historical data should you use to estimate portfolio risk parameters — and when should you override the math with judgment? This video walks through the covariance estimation formula with a concrete numerical example, explains the fundamental tradeoff between statistical precision and economic relevance, and builds a practical decision framework for choosing estimation windows.

Key concepts covered:

• Sample covariance formula: computing cross-products of return deviations and averaging across periods

• Numerical example: two-stock, four-period covariance calculation step by step

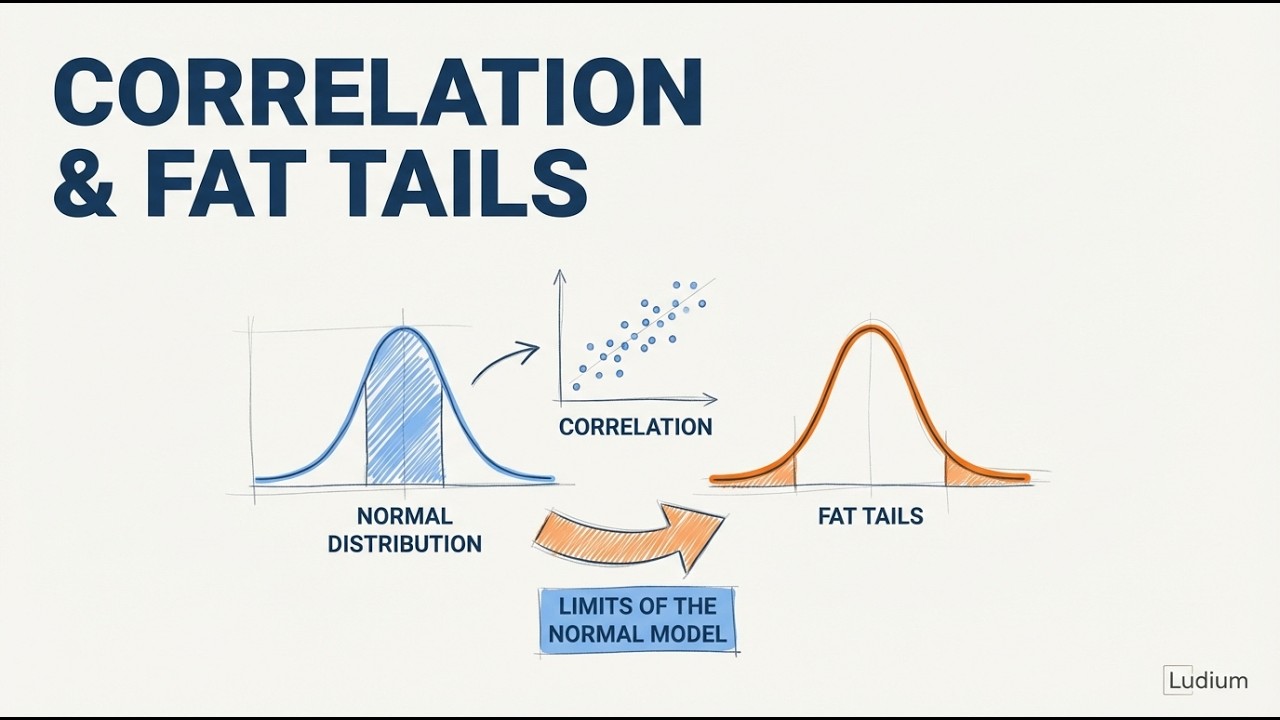

• Non-stationarity: why the statistical properties of financial returns change over time

• The estimation window tradeoff: more data reduces noise, but older data introduces systematic bias

• Annualizing volatility: converting monthly variance to annual variance using the square root of 12 rule

• Portfolio theory vs. stock picking: two fundamentally different investment philosophies and their assumptions

• Why crisis data (1987, 1998, 2000, 2008, 2020) should not be excluded from long-term estimates

• Rolling correlations: how S&P 500 vs. NASDAQ correlation shifts dramatically during crises

• Practitioner decision framework: structural breaks, regime dependence, and investment horizon

• The Venn diagram of effective risk estimation: mathematical framework, economic understanding, and contextual judgment

ORIGINAL SOURCE

This video is based on content from the following source:

• Ses 14: Portfolio Theory II

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: