Nano Blog: ASU 2025 08

Автор: South Carolina Association of CPAs

Загружено: 2026-02-10

Просмотров: 4

Описание:

On November 12, 2025, the FASB issued ASU 2025-08 to improve the accounting for purchased loans. Since issuing the credit losses standard in 2016, the FASB has monitored and assisted stakeholders with implementation through the post-implementation review (PIR). Through that process, stakeholders highlighted concerns about the accounting for acquired financial assets. Many noted that the existing guidance for acquired financial assets—specifically the distinction between purchased credit-deteriorated (PCD) and non-PCD assets—created unnecessary complexity and reduced comparability.

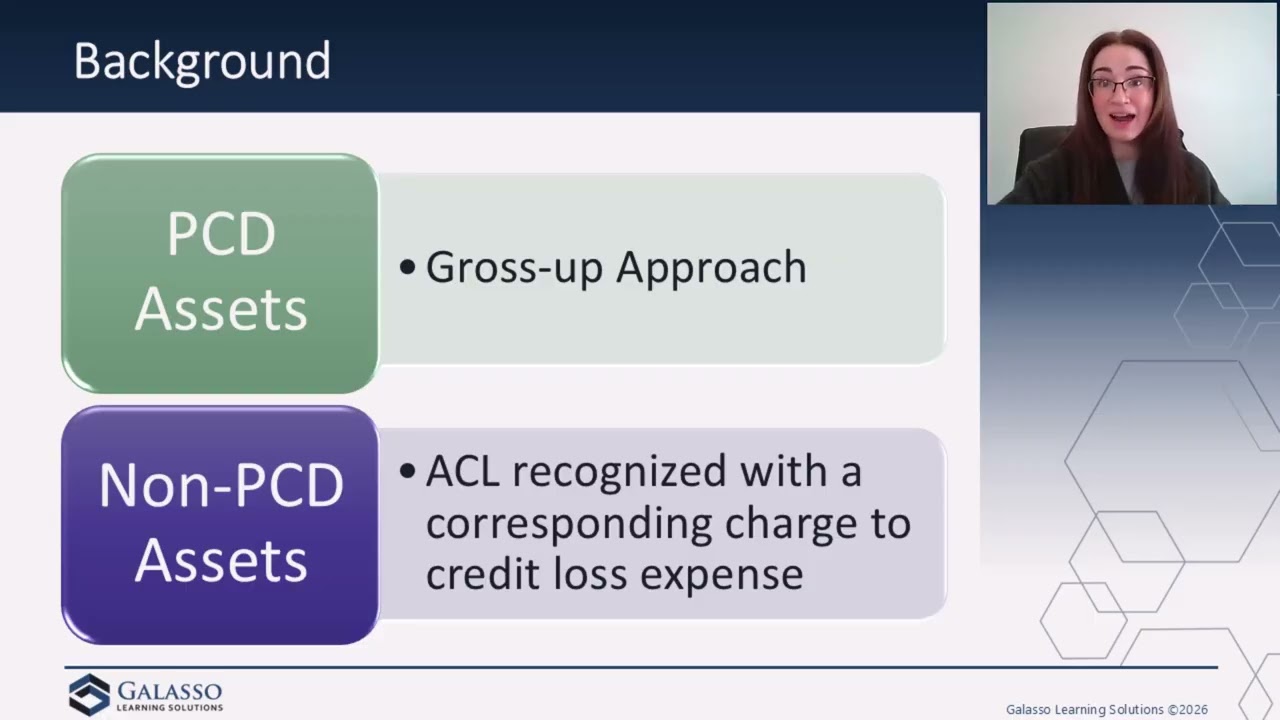

Under current GAAP, acquired financial assets are initially recorded at their amortized cost basis, with an allowance for expected credit losses (allowance) recognized separately. The process for PCD assets uses a “gross-up approach” to record the initial allowance through an adjustment to the initial amortized cost basis, while the initial allowance for non-PCD assets requires a direct charge to credit loss expense. This dual approach was seen as subjective, inconsistently applied, and resulted in double counting expected credit losses for non-PCD assets.

The new ASU addresses this by expanding the population of acquired financial assets accounted for using the gross-up approach. Acquired loans (excluding credit cards) are deemed purchased seasoned loans and accounted for using the gross-up approach upon acquisition if criteria established by the new guidance are met. This change aims to enhance comparability, consistency, and better reflect the economics of acquiring financial assets.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: