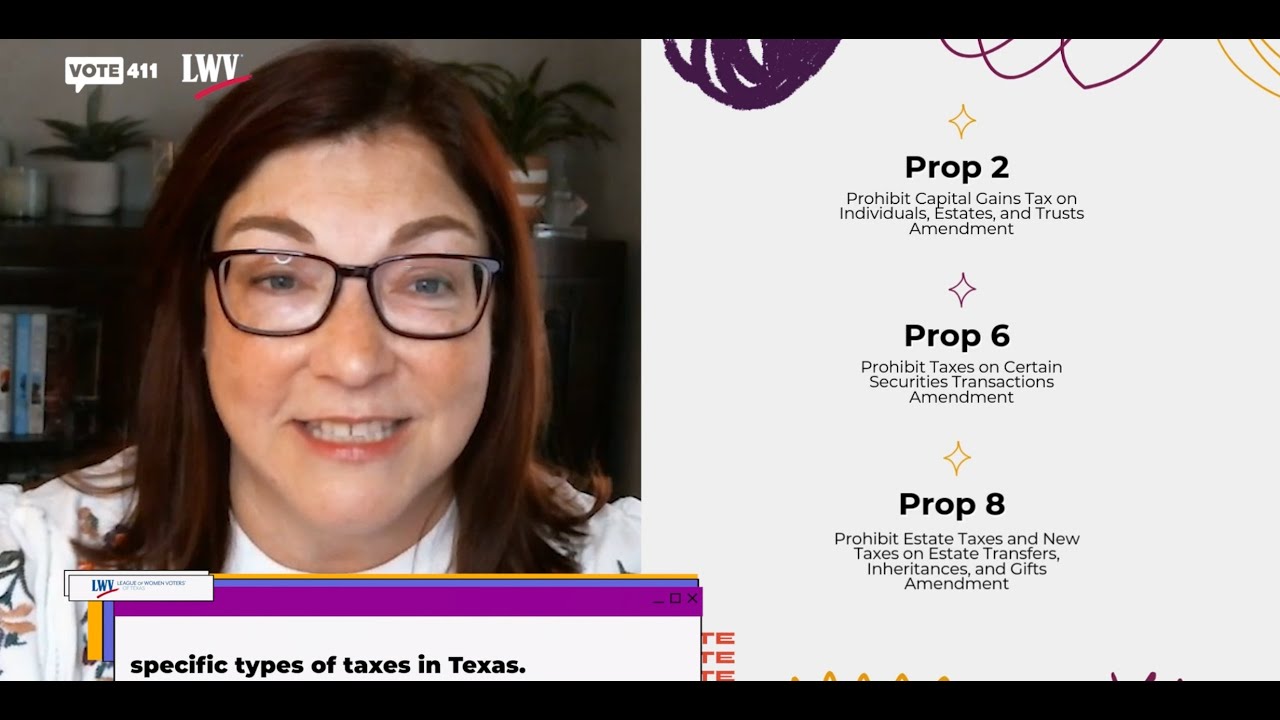

Propositions 5 & 9 - Animal Feed Taxes & Personal Property Tax Exemption

Автор: League of Women Voters of Texas

Загружено: 2025-09-22

Просмотров: 18263

Описание:

On November 4th, there will be an election covering several proposed changes to the Texas Constitution.

PROPOSITION 5 - Animal Feed Taxes

Proposition 5 is the constitutional amendment "authorizing the legislature to exempt from ad valorem taxation tangible personal property consisting of animal feed held by the owner of the property for sale at retail."

EXPLANATION

Under current law, animal feed is typically exempt from taxation at each location or transaction during its life cycle, from the field where it’s harvested to the purchase of the feed by a farmer or rancher, except for when the feed is sitting in a store as inventory. This proposed amendment seeks to address this inconsistency by amending the Texas Constitution to authorize the Texas State Legislature to exempt animal feed held by an owner for retail sale from personal property taxes.

ARGUMENTS FOR

• Removing this tax would help lower prices for farmers and ranchers, who are already dealing with rising operational expenses.

• Animal feed is part of our food chain, of which other parts are exempt from property taxes.

• Due to the seasonal needs of the agricultural business, warehouses are fully stocked when property taxes are calculated. Th is results in higher taxes on sellers that are passed onto the consumers.

ARGUMENTS AGAINST

• Inventory of other businesses is taxed as personal property since they are used to produce income. Th is proposition would treat those businesses unfairly.

• Exemptions for one group of taxpayers can unfairly shift the tax burden to other taxpayers.

• Inventory is constantly changing so the tax break cannot be easily measured.

PROPOSITION 9 - Personal Property Tax Exemption

Proposition 9 is the constitutional amendment "to authorize the legislature to exempt from ad valorem taxation a portion of the market value of tangible personal property a person owns that is held or used for the production of income."

EXPLANATION

Local taxing authorities, such as cities, counties, hospital districts, school districts and local college districts, tax personal property held or used for the production of income. This is a source of income used by these entities to pay for the services they provide to residents.

Business personal property that is held or used for the production of income includes inventory, computers, office furniture, manufacturing equipment, vehicles, machinery, and supplies. This does not include real estate. This tax is applied whether such personal property is owned or leased.

Currently $2,500 of business personal property is exempt from ad valorem taxation by local taxing entities. This proposed amendment would increase that exemption to $125,000 and would simplify the reporting requirements.

ARGUMENTS FOR

• Raising the exemption to $125,000 would ease the tax burden on small businesses, helping them keep more of their money to invest and grow.

• This would simplify tax reporting for small businesses with less than $125,000 of personal property.

• The Legislature could use part of the state’s general revenue to make up for any funding loss to school districts, ensuring they still receive adequate support.

ARGUMENTS AGAINST

• The Legislature did not provide additional monies to cities, counties, hospital districts, and college districts. To make up for the loss of revenue, these other local taxing entities may have to raise taxes or cut services.

• The Legislature may not be able to make up for the loss of funds to school districts should the economy slow and cause a budget deficit.

• This proposed amendment favors businesses at the expense of local residential taxpayers and taxing authorities.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: