Interest Rates (FRM Part 1 2025 – Book 4 – Chapter 10)

Автор: AnalystPrep

Загружено: 2021-04-19

Просмотров: 2118

Описание:

Learn how to calculate, interpret, and apply interest rates in FRM Part 1 Book 4 Valuation and Risk Models. This lesson explains spot rates, forward rates, and par rates, showing how they shape bond valuation and the yield curve. You will also understand compounding frequency, discount factors, and the concepts of flattening and steepening curves.

For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: https://analystprep.com/shop/unlimite...

AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams

After completing this reading, you should be able to:

Calculate and interpret the impact of different compounding frequencies on a bond’s value.

Calculate discount factors given interest rate swap rates.

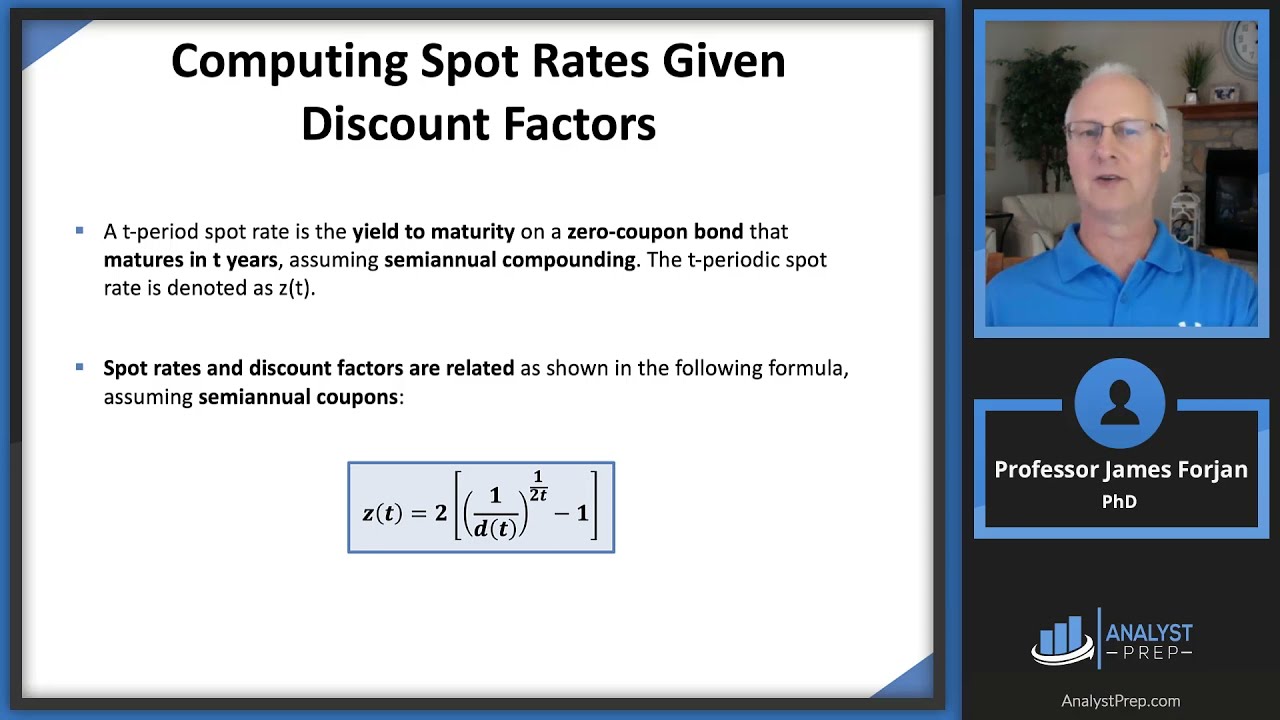

Compute spot rates given discount factors.

Interpret the forward rate, and compute forward rates given spot rates.

Define par rate and describe the equation for the par rate of a bond.

Interpret the relationship between spot, forward, and par rates.

Assess the impact of maturity on the price of a bond and the returns generated by bonds.

Define the “flattening” and “steepening” of rate curves and describe a trade to reflect expectations that a curve will flatten or steepen.

#FRM #FRMPart1 #InterestRates #FinancialRiskManager #GARP #BondValuation #YieldCurve #SpotRate #ForwardRate #AnalystPrep

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: