1031 Exchange Explained

Автор: Real Estate Finance Academy with Trevor Calton

Загружено: 2021-07-14

Просмотров: 1959

Описание:

FREE COURSE: Financial Analysis Fundamentals - https://www.realestatefinanceacademy....

Free Commercial Loan Document Kit: https://www.realestatefinanceacademy....

For COMMERCIAL LOANS: https://www.evergreencapitaladvisors....

---

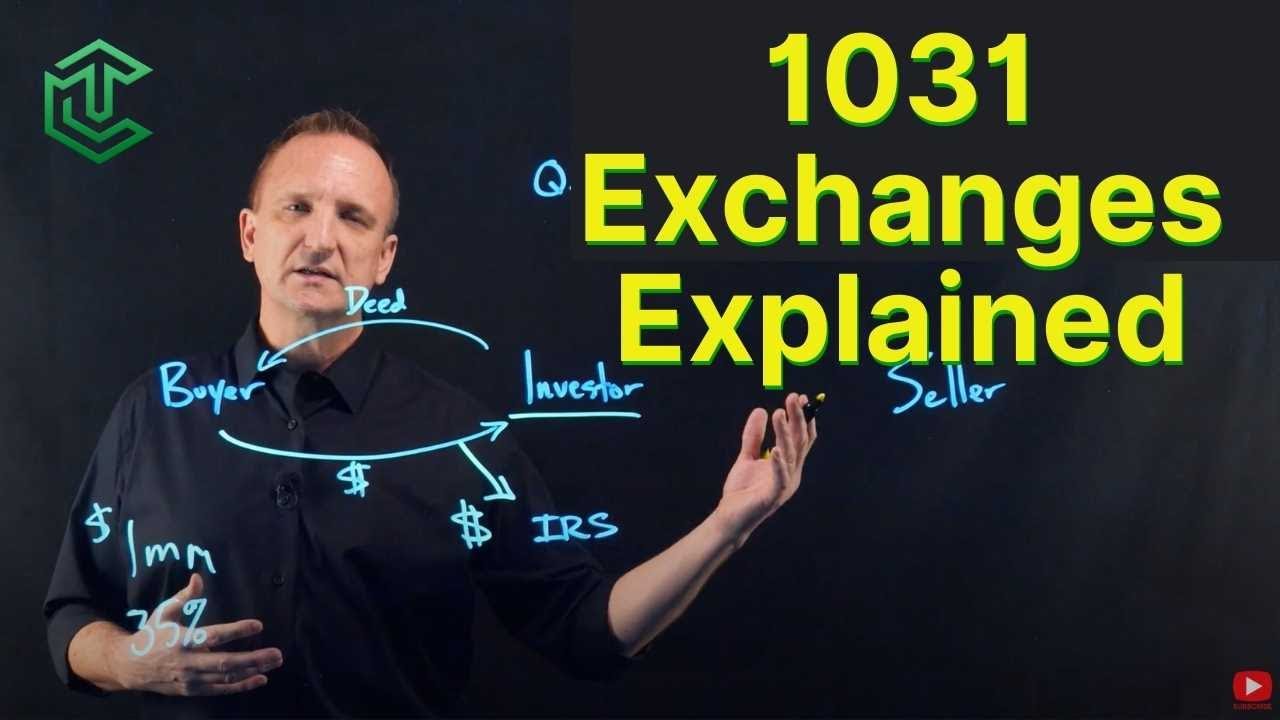

The 1031 exchange is a tax deferral strategy that allows an investor to relinquish a business or an investment asset and acquire another asset without having to pay capital gains taxes, or effectively deferring the capital gains taxes.

In a typical buy/sell transaction, the investor would receive cash from the buyer in exchange for the deed in the sale. At that point, a portion of that money would need to go to the IRS in the form of capital gains taxes, assuming that the seller or the investor made a profit.

If you had say a $1 million gain and were paying a 35% tax rate on capital gains between state and federal, then the taxpayer would be liable for approximately $350,000 to the IRS.

The 1031 exchange came about because an investor named Starker wanted to trade lands for other real estate, and he felt like because there wasn't a capital gain that was realized he shouldn't be liable for the taxes.

Normally what happens these days is what's called a delayed exchange. The delayed exchange gives the investor the opportunity to sell one property, and then within a certain timeframe, find another property from a different and invest in that without having to pay capital gains taxes.

In the 1031 exchange process, taking cash is called boot. As long as the investor does not receive any boot cash or debt relief, then they can avoid the capital gains taxes.

First, is that a 1031 is a tax deferral strategy, not a tax deduction. It simply allows the investor to defer realizing capital gains until a later date by rolling them into the next investment.

Next, is the 1031 exchange may only be used when buying and selling "like-kind" property. They can't sell real estate and then buy something like a yacht and still qualify for the 1031.

Next is they must use a qualified intermediary, often called an "accommodator".

Next, the 1031 exchange agreement must be in writing. The exchange agreement outlines the transfer of the relinquished property to the accommodator, the subsequent purchase of the replacement property by the accommodator, and the restrictions on the exchange proceeds during the exchange period.

The exchanger must inform the real estate agent about the 1031 exchange, and they need to make sure the process included in the purchase and sale agreement when listing the property for sale.

The property being sold is called the relinquished property, or the "downleg" property.

The property the exchanger buys is called the replacement property, or the "upleg".

The timelines on the 1031 are strict. The identification period allows for a maximum of 45 days from the date that the relinquished property closes in its sale to when they identify the potential replacement property. And then the exchange period is 180 days total.

When executing a 1031 exchange, the exchangers should begin searching for a replacement property before closing on the sale of the relinquished property. The countdown to identifying the replacement property begins the day of the sale of the relinquished property, and that 45 days goes by fast.

The exchanger cannot take what's called "constructive receipt" of the funds from the relinquished property, which are considered what's called "boot" and can be subject to capital gains tax.

"Cash boot" occurs when the exchanger takes any cash proceeds from the sale of the relinquished property, either by actual cash, or cash into a bank account that they control. Debt relief or "mortgage boot" is also a taxable event.

The Exchanger can identify up to three properties. By midnight, on the 45th day, they must identify the potential replacement properties and submit the names of those properties to the accommodator in writing.

They can potentially identify even more than three properties, as long as they close on 95% of those, or a total combined value of the identified properties is less than 200% of the value of the relinquished property.

#realestateinvesting #realestate #TrevorCalton #realestatefinance #investing #commercialrealestate #commercialloan #commercialloans #apartmentloan #multifamilyloan #apartmentinvesting #multifamilyinvesting #1031 #1031exchanges #stepbystep #stepbysteptutorial #diagram #example #download #freedownload #howto

commercial real estate analysis

CRE loan

investing in real estate

investment properties and commercial real estate

commercial real estate lending

commercial real estate loan

SBA commercial real estate loan

commercial real estate financing

commercial property loan

commercial building loan

real estate lending

best commercial real estate loans

commercial property lending

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: