Session 4: Risk Free Rates

Автор: Aswath Damodaran

Загружено: 2019-02-13

Просмотров: 13437

Описание:

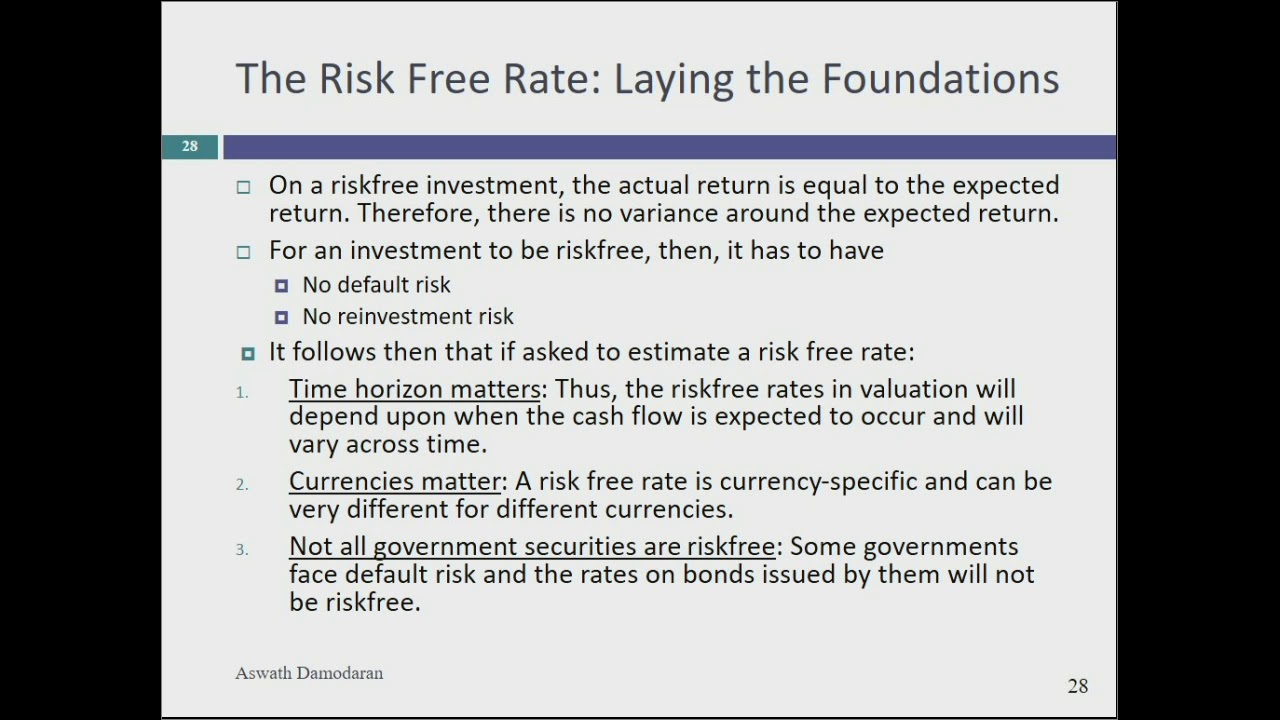

We started this session with a discussion of risk free rates, exploring why risk free rates vary across currencies and what to do about really low or negative risk free rates. The blog post below captures my thoughts on negative risk free rates:

http://aswathdamodaran.blogspot.com/2...

If you want to see my updated perspective on risk free rates, try my data post on the issue from earlier this year:

https://aswathdamodaran.blogspot.com/...

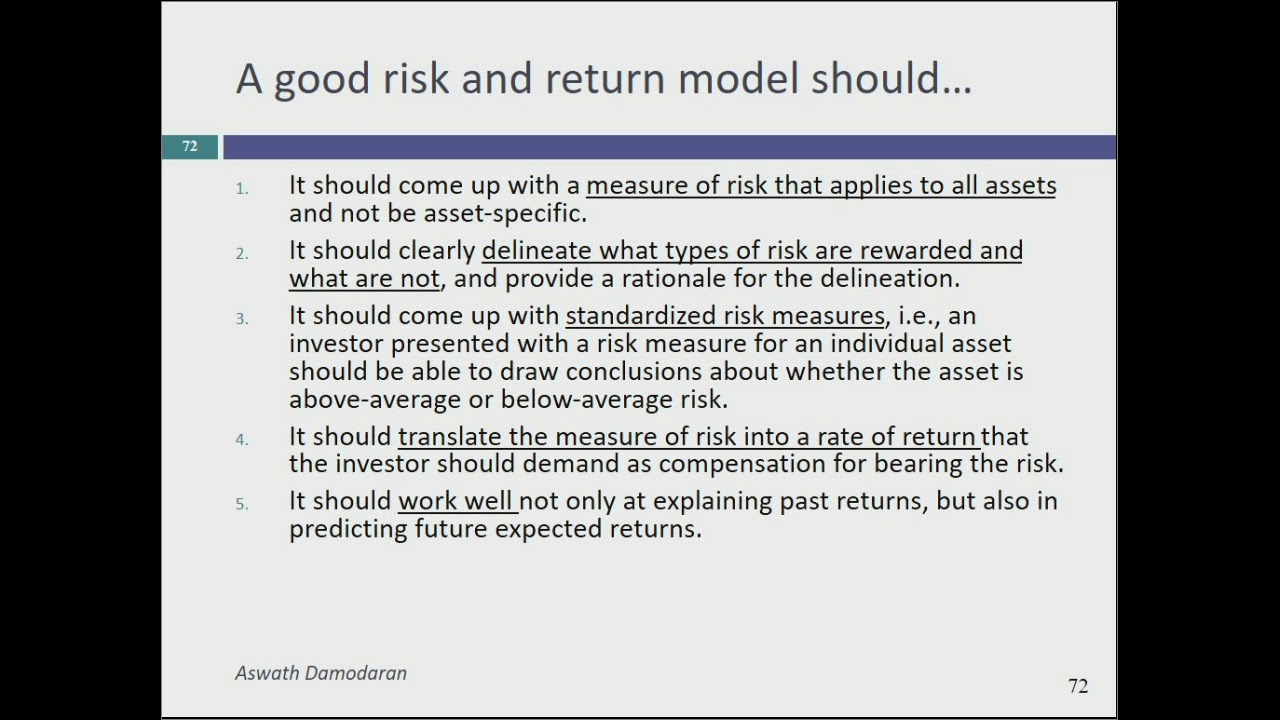

We just started on the discussion of equity risk premiums but the contours of the discussion should be clear. Historical equity risk premiums are not only backward looking but are noisy (have high standard errors). You can the historical return data for the US on my website by going to

http://www.stern.nyu.edu/~adamodar/Ne...

Click on current data, and look to the top of the table of downloadable data items.

Start of the class test: http://www.stern.nyu.edu/~adamodar/pd...

Slides: http://www.stern.nyu.edu/~adamodar/po...

Post Class Test: http://www.stern.nyu.edu/~adamodar/pd...

Post Class Test Solution: http://www.stern.nyu.edu/~adamodar/pd...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![CNN [#486] Dekalog szczęścia](https://imager.clipsaver.ru/yMkwYJ1_PQs/max.jpg)