05. Capital Asset Pricing Model

Автор: School of Investment

Загружено: 2025-11-05

Просмотров: 4

Описание:

The Capital Asset Pricing Model (CAPM) is a cornerstone of modern capital market theory, extending Markowitz's work and explaining how asset prices are determined when the market is in equilibrium. Key contributors to its development include Sharpe, Lintner, and Mossin. CAPM, in its broad sense, encompasses the Capital Market Line (CML) and the Security Market Line (SML).

CAPM is derived under several simplifying assumptions, such as all investors being risk-averse and seeking to maximize expected utility based on Markowitz’s average-variance model. Furthermore, investors are assumed to have homogeneous expectations regarding expected returns and variances. The model posits the existence of a risk-free asset, where investors can borrow or lend at the risk-free rate, and operates within a perfect capital market free of transaction costs and taxes.

The CML illustrates the relationship between expected return and total risk (standard deviation) for perfectly diversified, efficient portfolios. When including a risk-free asset, the optimal risky portfolio for all investors is the Market Portfolio (M), which is composed of all risky assets traded, weighted by their market value.

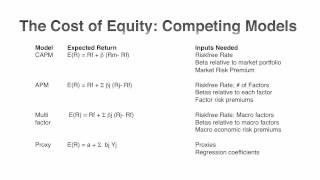

The SML defines the relationship between expected return and systematic risk, measured by Beta ($\beta$). Unlike the CML, the SML applies to both efficient and inefficient portfolios, as well as individual securities. Beta measures the sensitivity of an asset's return to fluctuations in market return. Assets with $\beta ) 1$ are considered aggressive stocks, while those with $\beta ( 1$ are defensive stocks. The SML formula is expressed as $E(R_i) = R_f + [E(R_m) - R_f] \times \beta_i$, where $[E(R_m) - R_f]$ is the market risk premium and the slope of the SML.

If an asset is mispriced (e.g., undervalued, lying above the SML), demand for it will increase, causing its price to rise and its expected return to fall until it reaches equilibrium on the SML.

CAPM’s simplifying assumptions have been tested and modified. The Zero-Beta Model addresses the non-existence of a truly risk-free asset by replacing $R_f$ with the expected return of a zero-beta portfolio, $E(R_Z)$. Incorporating real-world factors like different borrowing and lending rates, taxes, and transaction costs complicates the model, potentially resulting in CML/SML bands instead of a single line.

A major critique, notably from Roll, suggests that CAPM cannot truly be tested because the true Market Portfolio (M), which must include all capital assets (like bonds, real estate, and human capital), is unobservable. Therefore, practical tests using market index proxies only verify the efficiency of the proxy used, not the validity of the CAPM itself.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: