#investorrelations

Автор: Between Two Earnings Calls w Mr Investor Relations

Загружено: 2025-12-21

Просмотров: 100

Описание:

#investorrelations #capitalmarkets #corporatefinance #corporategovernance #corpgov #accountingandfinance #financialplanningandanalysis #financialprofessionals #investorrelationscareers #investorpresentation #earnings #earningscall #earningsreport #earningsannouncement #ceo #ceoadvisory #ceoadvice #ceoinsights #cfo #cfoadvisory #cfoadvice #cfoinsights #nyse #nasdaq #steverubis #mrinvestorrelations #betweentwoearningscalls #investmentbanking #venturecapital #privateequity #ipo #shareholders #boardofdirectors #shareholderengagement #equityresearch #equitymarkets #wallstreet #investorcalls #shareholdervalue #IRO #earningsprep #strategicfinance #BoardroomTrust #EquityStory #CaptialAllocation #ValuationPremium $LW

𝗕𝗲𝘁𝘄𝗲𝗲𝗻 𝗧𝘄𝗼 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹𝘀 𝘄/ 𝗠𝗿 𝗜𝗻𝘃𝗲𝘀𝘁𝗼𝗿 𝗥𝗲𝗹𝗮𝘁𝗶𝗼𝗻𝘀

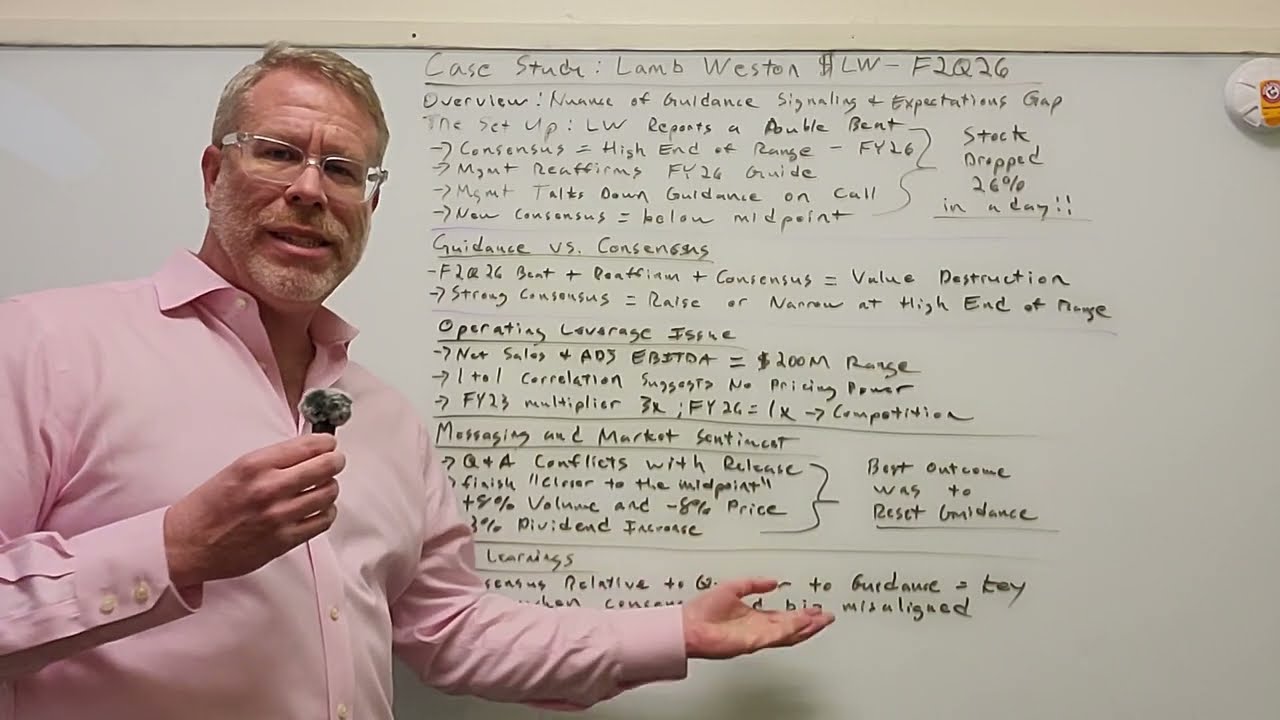

𝗖𝗮𝘀𝗲 𝗦𝘁𝘂𝗱𝘆: 𝗟𝗮𝗺𝗯 𝗪𝗲𝘀𝘁𝗼𝗻 ($𝗟𝗪) 𝗙𝟮𝗤𝟮𝟲 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹

On December 19, 2025, Lamb Weston experienced a 26% market valuation adjustment. This occurred despite the company delivering an earnings "double beat" and increasing its quarterly dividend. From an Investor Relations perspective, the event serves as a critical study in how the market interprets guidance ranges and management commentary and the importance of consistency of message.

𝗧𝗵𝗲 𝗘𝘅𝗽𝗲𝗰𝘁𝗮𝘁𝗶𝗼𝗻 𝗚𝗮𝗽: 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝘃𝘀. 𝗖𝗼𝗻𝘀𝗲𝗻𝘀𝘂𝘀

Strong consensus expectations + a quarterly beat + reaffirmation of guidance = value destruction.

The implied expectation when a company beats expectations is that the guidance range will be raised, or at a minimum narrow the range to the high end of the former guidance range

For example: $6.35B to $6.55B becomes $6.45B to $6.55B

The reaffirmation was inconsistent with consensus and inconsistent with management comments during the call.

𝗧𝗵𝗲 "𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗟𝗲𝘃𝗲𝗿𝗮𝗴𝗲" 𝗖𝗵𝗮𝗹𝗹𝗲𝗻𝗴𝗲

Both Net Sales and Adjusted EBITDA guidance called for an identical $200M size of range.

Such guidance implies to investors a 1-to-1 relationship between net sales and adj. EBITDA, which is atypical.

In FY23, $LW saw revenue up 27% and adj. EBITDA up 92%, a 3.4x multiplier.

Reaffirmed guidance suggests a 1.0x multiplier in FY26, vividly illustrating why the Q&A focused so much on competition and pricing pressure.

𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗠𝗲𝘀𝘀𝗮𝗴𝗶𝗻𝗴 𝗮𝗻𝗱 𝗠𝗮𝗿𝗸𝗲𝘁 𝗦𝗲𝗻𝘁𝗶𝗺𝗲𝗻𝘁

The problem was that management commentary did not align with the F2Q26 press release.

Management talked down consensus in prepared remarks and throughout Q&A.

The 8% volume growth offset by 8% price headwinds summed up the problem.

Investors saw through the 3% dividend increase because of the guidance inconsistencies

𝗧𝗵𝗲 𝗔𝗹𝘁𝗲𝗿𝗻𝗮𝘁𝗶𝘃𝗲: 𝗥𝗲𝘀𝗲𝘁 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝗖𝗼𝗺𝗽𝗹𝗲𝘁𝗲𝗹𝘆

In this case, $LW reaffirmed guidance and talked down consensus during the earnings call.

Consensus reset below the reaffirmed midpoint, but did not remove the possibility of another downside guidance revision at the F3Q26 earnings release.

Resetting the range, in this case $6.35B to $6.45B, becomes the new guidance range, allows the company to:

Reset valuation expectations on the fly,

Staunch the valuation destruction, and

Remove the likelihood of a negative guidance revision at the F3Q26 earnings print.

𝗞𝗲𝘆 𝗟𝗲𝗮𝗿𝗻𝗶𝗻𝗴𝘀

Consensus expectations relative to the quarter’s results and financial guidance drives valuation.

When consensus is stronger than visibility you must reset expectations.

The release, comments, and Q&A need to be aligned.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: