Mastering DCF Valuation Top 10 Mistakes!

Автор: The Bespoke Mortgage Experience

Загружено: 2024-08-19

Просмотров: 34

Описание:

When working with Discounted Cash Flow (DCF) models, even small mistakes can lead to significant mis-valuations. Let's explore some key areas where errors often occur, and how to avoid them.

First, it's essential to separate assumptions from calculations. Mixing them can create confusion and make your model difficult to audit.

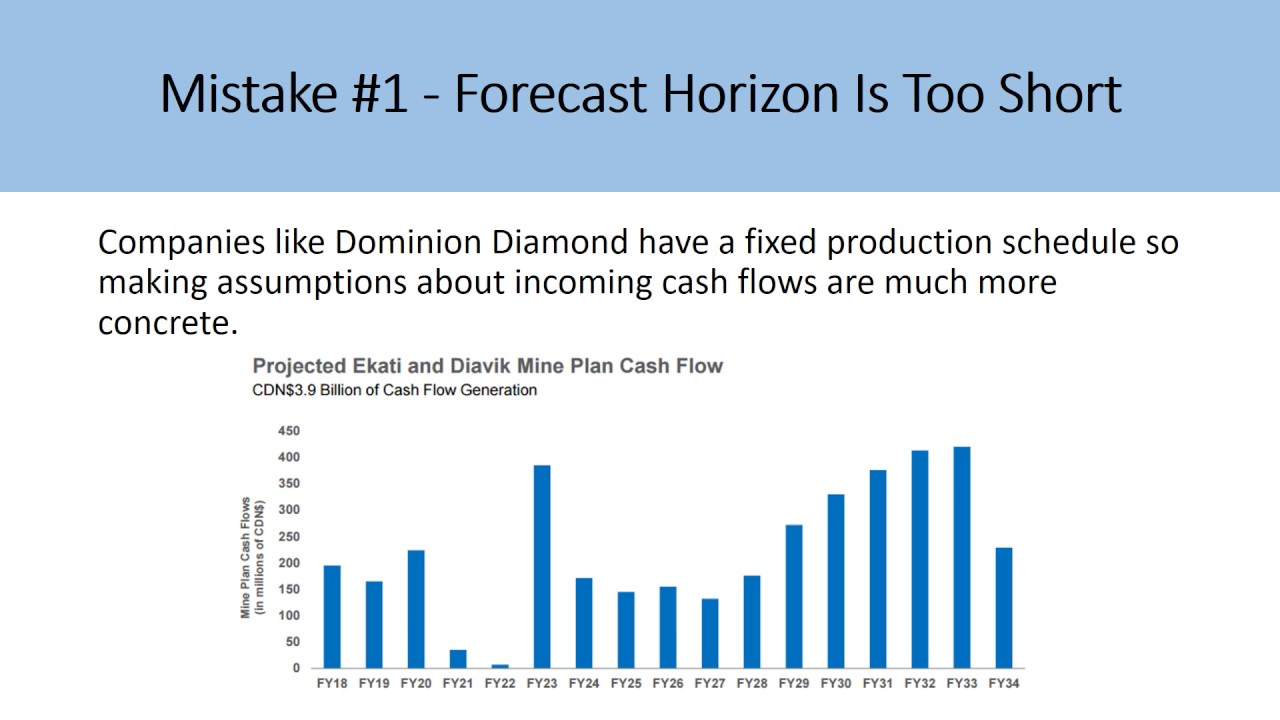

Next, be cautious with your forecasts. Overly optimistic projections, based on best-case scenarios rather than realistic data, can inflate valuations and lead to inaccurate results. It's always better to stay grounded in what the data tells you.

Understanding a company's competitive advantage, or economic moat, is another critical factor. Ignoring this can lead to overly simplistic and inaccurate long-term projections. Companies with strong moats are likely to sustain profits better over time, which should be reflected in your model.

One common error is miscalculating the Weighted Average Cost of Capital (WACC). Since WACC represents the risk and time value of money, getting this wrong can throw off your entire valuation. Ensure you’re using the correct inputs to accurately reflect the company’s risk profile.

Terminal value often constitutes a large portion of a DCF model, but relying too heavily on it can be risky. If your long-term assumptions aren’t well-founded, the terminal value might artificially inflate your valuation. Balance this with a detailed projection of cash flows.

Don’t overlook changes in working capital. These fluctuations can significantly impact cash flow, and neglecting them might lead to underestimating or overestimating a company’s financial health.

Always use the most up-to-date historical data available. The past informs the future in DCF models, and relying on outdated information can lead to projections that don’t align with the current market reality.

Sensitivity analysis is crucial but often overlooked. It allows you to see how changes in key assumptions, such as discount rates or growth rates, impact the valuation. This step helps gauge the robustness of your model and prepares you for different scenarios.

Cross-checking your DCF results with other valuation methods, like comparable company analysis, ensures your findings are not outliers. This validation step is vital for ensuring the credibility of your valuation.

Lastly, ensure your financial statements are consistent and accurate. Inconsistent data can lead to significant errors, compromising the integrity of your entire model.

By avoiding these common pitfalls, you'll enhance the reliability of your DCF valuations and make more informed financial decisions.

#Finance #Valuation #DCFModel #InvestmentAnalysis #CorporateFinance #BusinessStrategy #FinancialModeling #LinkedInLearning

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: