Paytm s Turnaround Q2 FY26

Автор: STOCK AND SPICE

Загружено: 2026-02-02

Просмотров: 2

Описание:

Applying a Buffett-style investment model to One 97 Communications (Paytm) involves evaluating its economic moat, management quality, financial fortress, and valuation.

Based on the sources, while Paytm has built a powerful economic moat and demonstrated strong management agility, a strict Buffett disciple might be cautious regarding its high valuation metrics.

1. Economic Moat (Competitive Advantage)

Buffett looks for a "bridge with a toll." Paytm has established several "tolls" in the Indian digital economy:

• High Switching Costs: Paytm has 1.37 Cr subscription-paying merchants. These merchants pay monthly fees for Soundboxes and POS devices, creating sticky, recurring revenue that is difficult for competitors to displace.

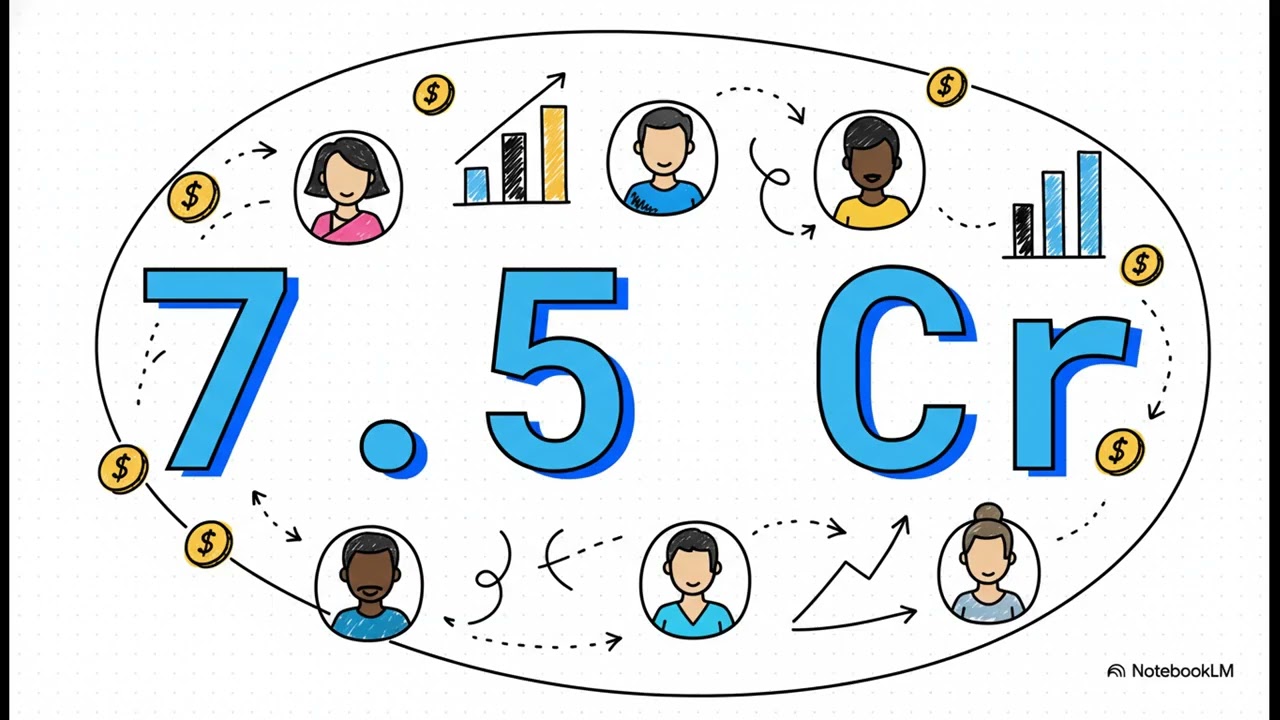

• Network Effect: With 4.7 Cr registered merchants and 7.5 Cr Monthly Transacting Users (MTUs), Paytm has a massive ecosystem that attracts more partners and users.

• Proprietary Technology: Its in-house AI platforms, like Paytm ARMS and Paytm Pi, create a "high-retention flywheel" by automating onboarding and fraud detection.

2. Management Integrity & Capability

Buffett prioritizes managers who act like owners. Recent management actions align with this:

• Shareholder Alignment: CEO Vijay Shekhar Sharma voluntarily forwent 2.1 Cr ESOPs to reduce company expenses and improve the bottom line.

• Transparency: Management has pivoted to "clean" GAAP reporting, discontinuing the use of "Adjusted EBITDA" to provide a clearer picture of profitability.

• Operational Pivot: Management successfully navigated a difficult regulatory period to reach an EBITDA and PAT profitability inflection point in FY 2026.

3. Financial Strength ("The Cash Fortress")

A key Buffett requirement is a strong balance sheet to survive downturns:

• Liquidity: Paytm maintains a massive cash balance of ₹13,068 Cr as of September 2025.

• Operating Leverage: Revenue grew 24% YoY in Q2 FY 2026, while indirect costs remained range-bound, showing that the business is becoming more efficient as it scales.

• Capital Light Growth: The company is focusing on refurbishing existing devices rather than just buying new ones, which has significantly lowered capital expenditure (Capex).

4. The Valuation Catch (Margin of Safety)

This is where a traditional Buffett model might flash a caution light:

• High P/E Ratio: Paytm’s stock P/E is 137, which is much higher than the industry average of 28.7.

• Price to Book (P/B): At 4.77, the stock is not "cheap" by traditional value-investing standards.

• Regulatory Risks: Buffett typically avoids companies with high regulatory uncertainty. Paytm still faces "overhangs" regarding its Payment Aggregator license and evolving RBI guidelines.

________________________________________

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: