Скачать

VAR Models: Impulse-Responses and Structural VAR Models

Автор: Rasmus Pedersen

Загружено: 2021-03-02

Просмотров: 25654

Описание:

Video for Econometrics II course @ Dept. of Economics, Uni. of Copenhagen.

Original slides by Heino Bohn Nielsen and adapted by Rasmus Søndergaard Pedersen.

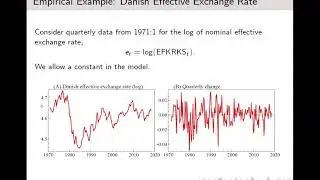

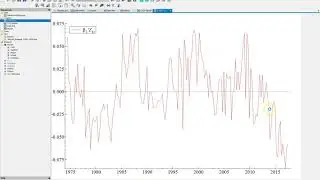

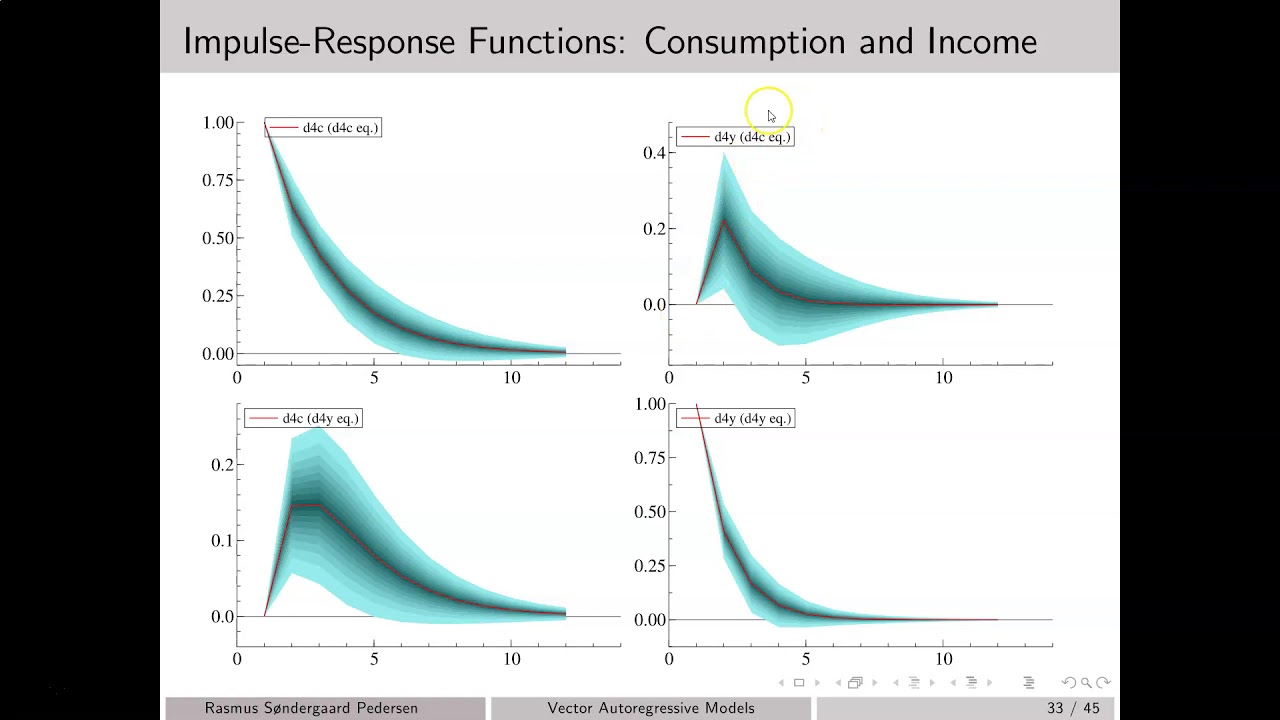

We consider impulse-response functions for vector autoregressive (VAR) models. Moreover, we introduce the notion of structural VAR (SVAR) models.

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![[TEORIA] Modelo VAR. VAR estrutural. Impulso-Resposta. Decomposição da Variância (Aula 2)](https://image.4k-video.ru/id-video/aRo0kknGPus)