(EViews10)Interpret VAR, Forecast Error Variance Decomposition

Автор: CrunchEconometrix

Загружено: 2018-04-23

Просмотров: 36866

Описание:

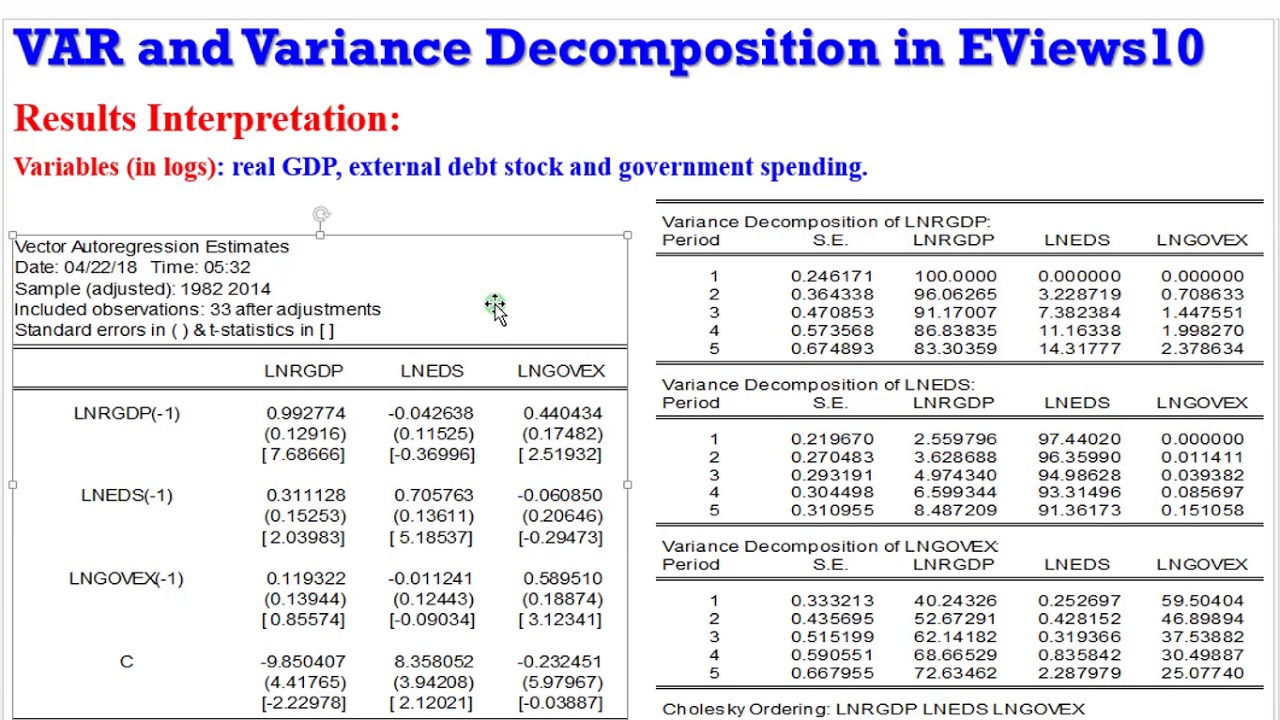

The variance decomposition indicates the amount of information each variable contributes to the other variables in the autoregression. It determines how much of the forecast error variance of each of the variables can be explained by exogenous shocks to the other variables. This video gives a step-by-step guide on how to estimate and interpret a VAR model and analyse the variance decomposed among the variables in the system.

Here is the link to the wanne.xlsx dataset used for this tutorial (endeavour to have a Google account for easy accessibility): https://drive.google.com/drive/u/1/fo...

Follow up with soft-notes and updates from CrunchEconometrix:

Website: http://cruncheconometrix.com.ng

Blog: https://cruncheconometrix.blogspot.co...

Forum: http://cruncheconometrix.com.ng/blog/...

Facebook: / cruncheconometrix

YouTube Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and Interpret Two-way A...

EViews Videos Playlist: • (EViews10):Interpret VECM, Forecast Error ...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: