Intro to Financial Accounting: Bonds Issued at Discount & Premium; Stockholder's Equity

Автор: Rutgers Accounting Web

Загружено: 2013-12-06

Просмотров: 4175

Описание:

Introduction to Financial Accounting

Professor Alexander Sannella

Lecture 21

00:12 Review on Recording Bonds issued at discounts (verbal)

06:03 Recording Bonds Issued at a discount

06:58 Example

08:05 Recording Discounted bonds

17:52 Straight line - Amortization Table (discount)

19:36 Example

23:20 Recording Bonds Issued at a Premium

24:15 Example (verbal)

31:22 Journal Entry

34:25 Amortization Table (premium) example

36:05 Journal Entry

Questions and Answers

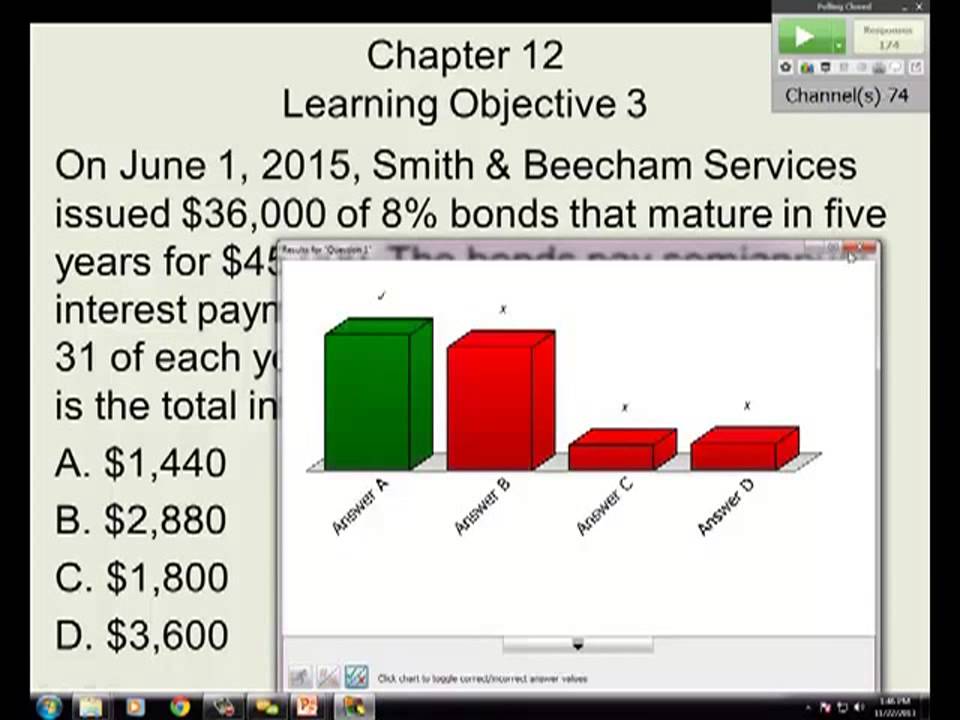

39:46 Question 1

46:10 Question 2

52:07 Question 3

Learning Objective 4

56:06 Retirement of Bonds at Maturity + Journal Entry

56:56 Retirement before Maturity

59:36 Reasons for retiring bonds early

1:02:05 Example of retirement before maturity + Journal Entry

Learning Objective 5

1:06:24 Balance Sheet Example

Learning Objective 6

1:06:45 Debt Equity Ratio

Chapter 13

Learning Objective 1

1:10:57 Stockholder's Equity

(Definitions of Stock Terms)

When the bond interest rate is greater than the market rate, the bonds are issued at a premium. The difference between the bonds payable and the cash received is recorded as a bond premium (an adjunct account). The premium is amoritzed over the life of the bond, reducing interest expense to the lower market rate.

When the bond interest rate is less than the market rate, the bonds are issued at a discount. The difference between the bonds payable and the cash received is recorded as a bond discount (contra-liability). The discount is amortized over the life of the bond, increasing interest expense to the higher market rate.

Bonds can be retired before maturity by an open market repurchase or a "call." Bonds can be called at par or a price above par (which is par plus a call premium). A company will retire bonds before maturity for a variety of reasons: (1) To refinance in order to take advantage of lower market interest rates, (2) the company has excess cash and would like to avoid future interest changes and create greater financial flexibility, (3) to improve the company's debt to equity ratio, and (4) to comply with other debt agreements.

When retiring before maturity, the full bonds payable will typically be retired. The remaining discount or premium will be removed. The cash paid will not equal the face value. The difference will be recorded as either a gain on retirement of bonds (cash paid to retire is less than the carrying value) or a loss on retirement of bonds (cash paid to retire is more than the carrying value).

A corporation is a separate entity created by law that is separate and distinct from its owners and its continued existence is dependent upon the corporate statutes of the state in which it is incorporated. Classification by ownership distinguishes between publicly held and privately held corporations.

The primary objectives for accounting for stock holder's equity are to: (1) separately disclose each source of equity (due to widespread ownership and the owner-manager separation), and (2) to disclose all rights or any restrictions of rights of each class of equity security.

The stockholders' equity section of the balance sheet includes several parenthetical disclosures: the terms are: authorized shares, issued shares, and outstanding shares. Authorized shares is the maximum number of shares of stock that a company can issue. It is specified in the company's charter. Issued shares are the total number of a company's shares that have been sold or distributed to shareholders over time. Outstanding shares are the number of shares of a corporation's stock that are in the hands of investors. Outstanding shares are issued shares less treasury shares. Treasury shares are the number of issued shares that have been previously issued and later reacquired by the corporation.

To receive additional updates regarding our library please subscribe to our mailing list using the following link:

http://rbx.business.rutgers.edu/subsc...

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![CCH Access Tax Software Demo: Tax Preparation Bootcamp Individual Return in 1 hour [2024]](https://imager.clipsaver.ru/LkaNyXMTbhA/max.jpg)