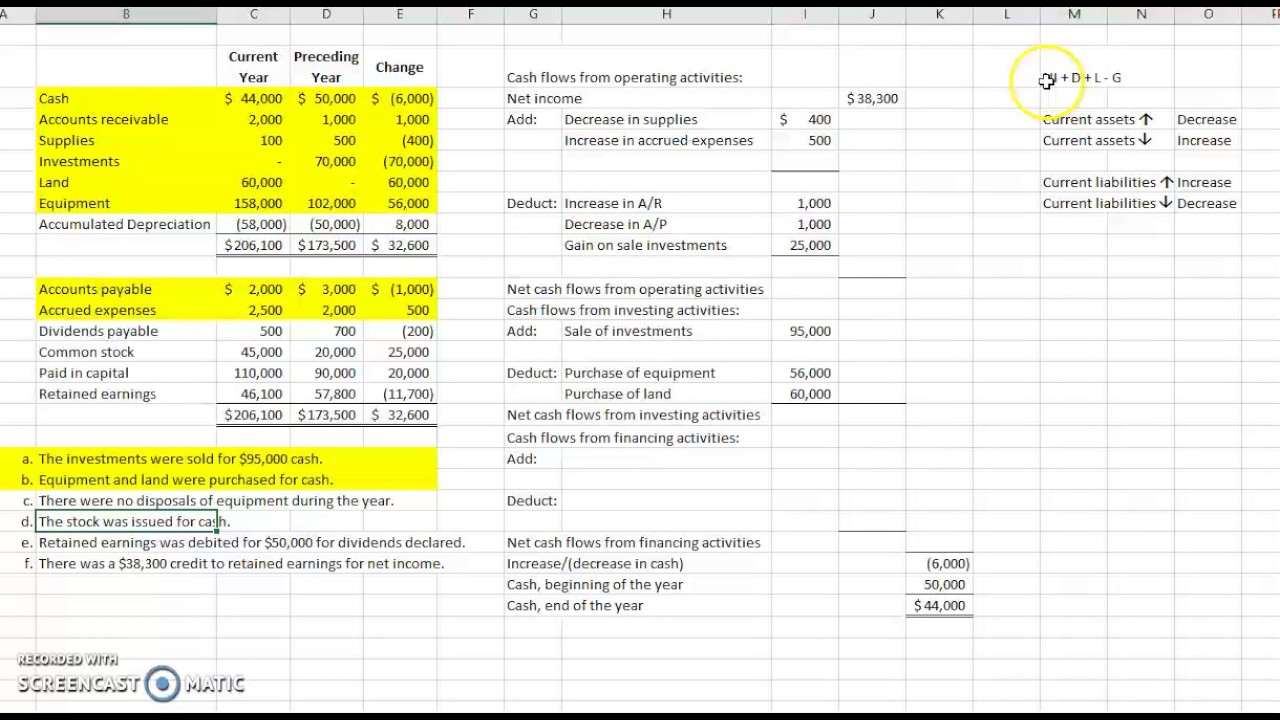

Statement of Cash Flows -Intro to Financial Accounting-Spring 2013(14)-Victoria Chiu

Автор: Rutgers Accounting Web

Загружено: 2013-05-30

Просмотров: 36582

Описание:

Principles of Auditing: Professor Liburd

Lecture 1

Overview

1/24/14

Please visit our website at http://raw.rutgers.edu

TIME STAMPS

0:19 In the Public Interest

1:58 Center for Audit Quality Website (& video)

6:44 Auditing vs. Accounting

11:35 Definition of Auditing

27:03 Purpose of Auditing

30:01 Information Risk

30:59 Assurance vs. Attestation

34:25 Sarbanes-Oxley Act

The purpose of this lecture is to provide the student with an overview of auditing and assurance services and the CPA profession as a while.

Auditing and accounting are technically two different fields, and thus should be distinguished. Accounting is the recording, classifying, and summarizing of economic events for the purpose of providing financial information used in decision making. Auditing is determining whether information that has already been recorded properly reflects the economic events that occurred during the accounting period.

More specifically, auditing is a systematic process of objectively obtaining and evaluating evidence regarding assertions (financial statements, including footnotes) about economic actions and events to ascertain the degree of correspondence between the assertions and established criteria (GAAP) and communicating the results (auditor's report and other reports) to interested users (persons who rely on the financial reports to make economic and financial decisions, such as creditors and investors).

An audit is performed by a competent, independent person (both independent in fact and independent in appearance). The auditor must be qualified to understand the criteria used and must be competent to know the types and amount of evidence to accumulate to reach the proper conclusion after the evidence has been examined. The competence of the individual performing the audit is of little value if he or she is biased in the accumulation and evaluation of evidence. Overall, auditors lend credibility to the financial statements presented by management.

There are numerous factors that have contributed towards the need of independent auditing today.

(1) Remoteness of information (i.e. lack of stockholder interaction with management, directors not being involved in daily operations and decision making, and dispersion of the business among numerous geographical locations and complex corporate structures).

(2) Biases and motives of the provider. Information will be biased in favor of the provider when his or her goals are inconsistent with the decision maker's goals.

(3) Voluminous data. Most business have to deal with millions of transactions processed daily via a sophisticated computerized system. There are also multiple product lines, and multiple transaction locations (probably for EACH of the aforementioned product lines). A fourth is

(4) Complex exchange transactions. New and changing business relationships lead to innovative accounting and reporting problems. The potential impact of transactions is not always quantifiable, which in turn leads to increased (and sometimes more complex) disclosures.

Auditing plays an important role in reducing information risk. Information risk reflects the possibility that the information upon which the business risk decision was made was inaccurate. Causes of information risk include the fact that it is nearly impossible for a decision maker to have much firsthand knowledge about the organization with which they do business (i.e. information from others must be relied upon). Furthermore, if information is provided by someone whose goals are inconsistent with those of the decision maker, the information may be biased in favor of the provider. The higher the volume of transactions, the greater the risk that improperly recorder information is included in the records. Exchange transactions between organizations have become increasingly complex and therefore more difficult to record properly.

There are four major elements of the broad definition of assurance services. (1) Independence-integrity and objectivity. (2) Professional services (which involves some element of judgment based on education and experience). (3) Improving the quality of information or its context (assuring users about the reliability and relevance of information). (4) For decision makers.

An attestation service is a type of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. To attest means to lend credibility or to vouch for the truth or accuracy of the statements that one party makes to another. It is primarily financial information. There are five categories: (1) audit of historical financial statements, (2) attestation of internal control over financial reporting, (3) review of historical financial statements, (4) attestation services on info technology, (5) other attestation services.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке:

![James Webb: How to Read a Financial Statement [Crowell School of Business]](https://imager.clipsaver.ru/Jkse-Wafe9U/max.jpg)