SECTION 194 - DIVIDENDS

Автор: edVihansh

Загружено: 2023-11-05

Просмотров: 3

Описание:

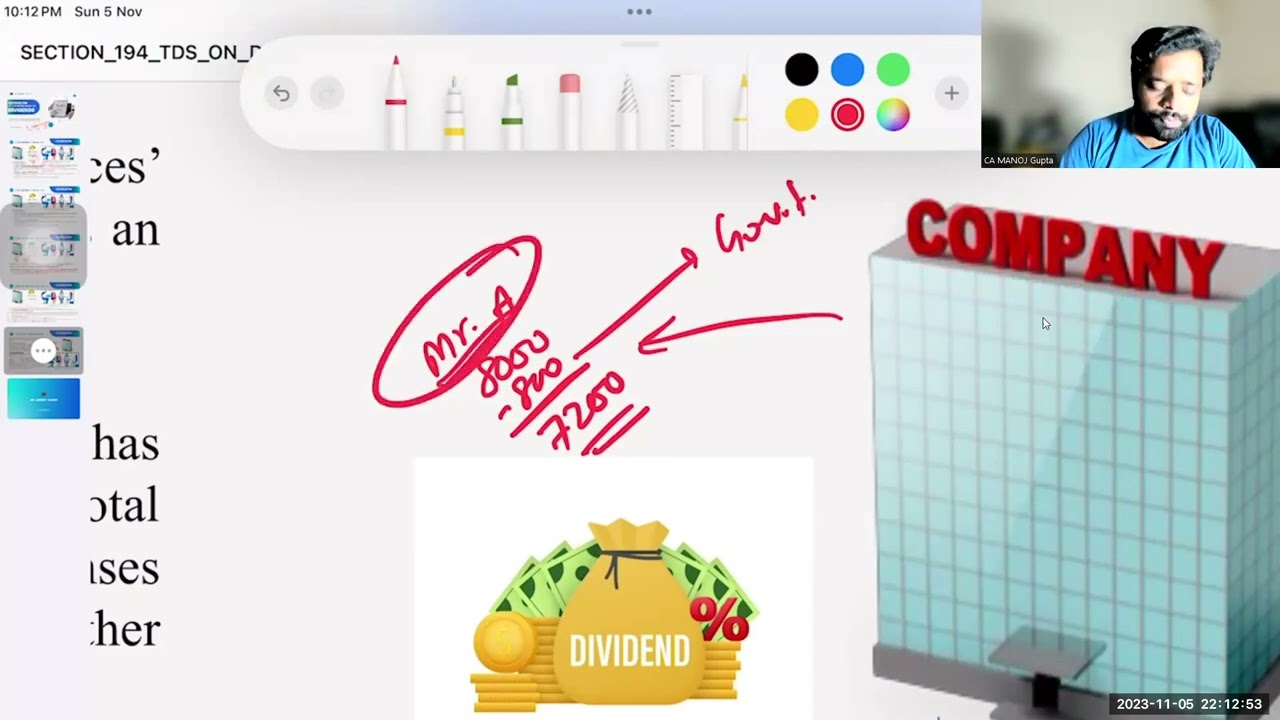

In this session we have discussed Provision related to tax deduction at source in case of dividends declared and paid by an India company or a company which has made the prescribed arrangements for the declaration and payment of dividends (including dividends on preference shares) within India.

In simple words, this provision is about how an Indian company must deduct a 10% tax from the dividends they pay to shareholders who are Indian residents. However, there are some exceptions:

If the dividend is not paid in cash and the total dividend paid in a financial year is less than Rs. 5,000, no tax is deducted for individual shareholders.

This rule doesn't apply to certain government insurance companies or other insurers in the case of dividends they receive.

It also doesn't apply to a "business trust" for dividends received from a special purpose vehicle as defined by law.

The government can add more exceptions by notifying them in the Official Gazette.

Повторяем попытку...

Доступные форматы для скачивания:

Скачать видео

-

Информация по загрузке: